- Oil prices ease on Iran dialogue signals

- India factory output hits two-year high

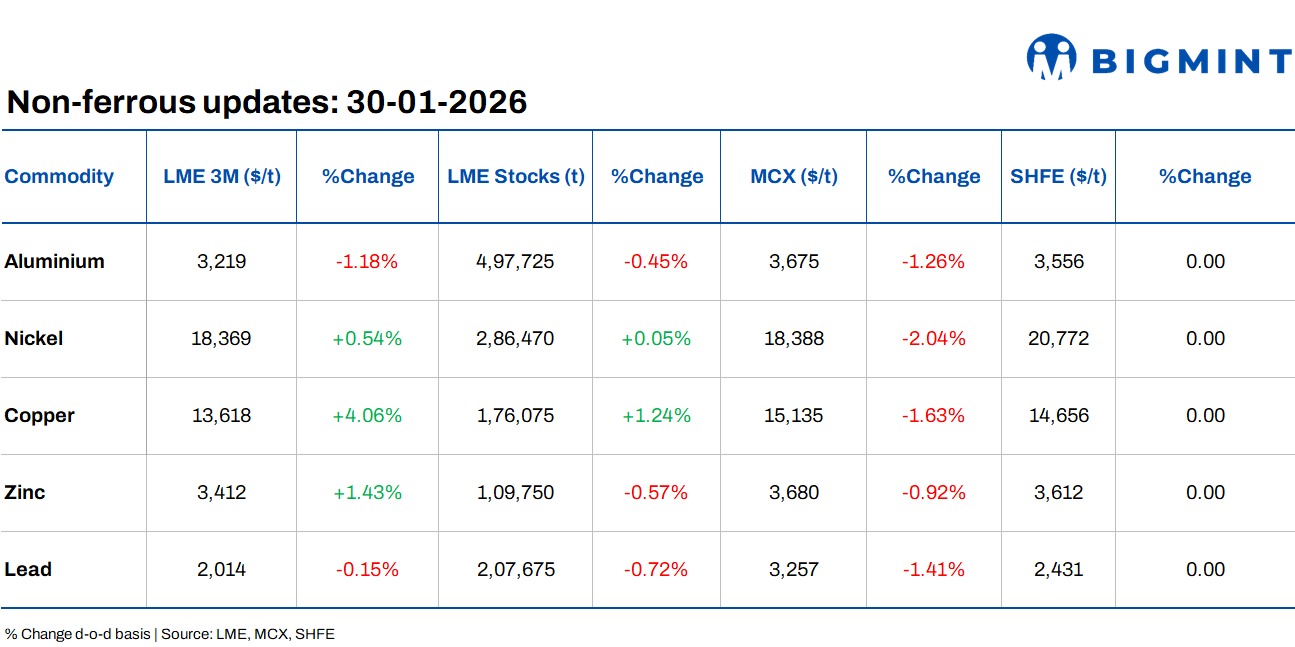

Base metals prices on the London Metal Exchange (LME) traded mixed, reflecting divergent price movements across the complex. Copper led the gains, surging 4.06% to $13,618/t, supported by strong buying momentum, while zinc advanced 1.43% to $3,412/t and nickel edged up 0.54% to $18,369/t. In contrast, aluminium prices declined 1.18% to $3,219/t, while lead slipped marginally by 0.15% to $2,014/t, capping overall market optimism.

LME warehouse inventories also showed uneven trends, indicating mixed supply conditions. Aluminium stocks fell 0.45% to 497,725 t, zinc inventories declined 0.57% to 109,750 t, and lead stocks dropped 0.72% to 207,675 t, pointing to slightly tighter availability. Meanwhile, copper inventories increased 1.24% to 176,075 t and nickel stocks inched up 0.05% to 286,470 t, suggesting modest inflows and relatively comfortable near-term supply on the exchange.

Domestic market overview

In India’s non-ferrous scrap market, aluminium Tense scrap prices edged up d-o-d across key regions. Ex-Delhi assessments rose by INR 1,000/t to INR 211,000/t, while ex-Chennai prices also increased by INR 1,000/t to INR 213,000/t, reflecting steady regional buying interest. Meanwhile, copper armature scrap prices, ex-Delhi, jumped sharply by INR 73,250/t (6.4%) to INR 1,213,250/t, indicating a strong uptick in demand among market participants.

Other updates

Oil prices ease on Iran dialogue signals

Oil prices slipped as markets reacted to signals that the US may pursue dialogue with Iran over its nuclear programme, easing fears of immediate supply disruptions from potential military action. Brent crude fell below $70/bbl, while WTI also retreated, pressured further by a firmer dollar. Despite the pullback, both benchmarks remain on track for strong monthly gains, supported by heightened Middle East tensions and recent supply disruptions across key producing regions.

Private sector activity rebounds to two-month high in January

India’s private sector activity strengthened in January, with the HSBC flash Composite PMI rising to 59.5 from 57.8 in December, signalling the fastest expansion in two months. The rebound was driven by a pickup in new orders, output and hiring across both manufacturing and services, reversing December’s slowdown. The flash Manufacturing PMI climbed to 56.8, while services activity also improved, reflecting firmer demand conditions, higher international orders and renewed job creation, despite rising input cost pressures.

India’s factory output hits two-year high in December

India’s industrial production surged 7.8% y-o-y in December 2025, marking its fastest growth in over two years, driven by strong performance across manufacturing, mining and power. Manufacturing output rose 8.1%, led by basic metals, automobiles and pharmaceuticals, while mining and power generation grew 6.8% and 6.3%, respectively. Despite the sharp December rebound, industrial growth during April-December FY26 moderated slightly to 3.9%, reflecting uneven momentum earlier in the fiscal year.

Leave a Reply