- Scrap prices stable in Chennai, steel firms up

- Billet prices increase by INR 500/t w-o-w

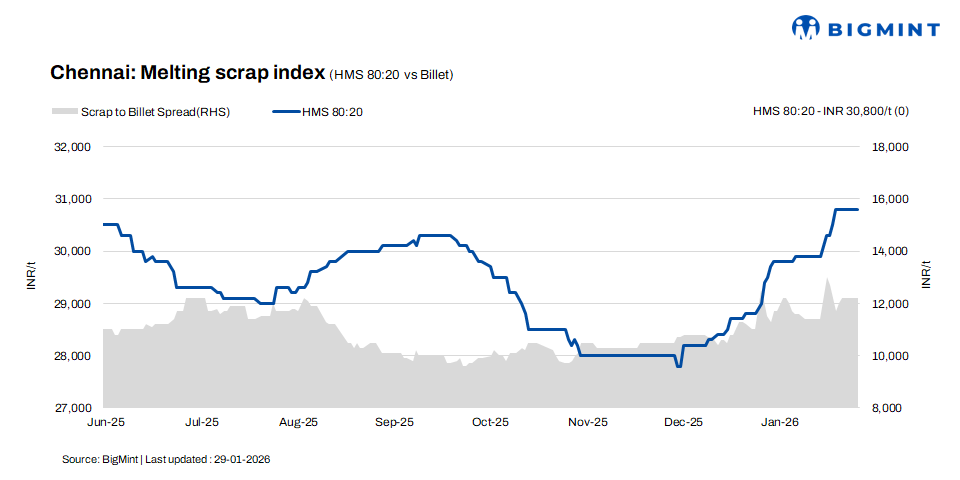

HMS (80:20) scrap prices in Chennai remained stable at INR 30,800/t, with no changes recorded on either a d-o-d or w-o-w basis, according to BigMint’s latest assessment. In contrast, billet and rebar prices strengthened by INR 500/t w-o-w to INR 43,000/t and INR 47,500/t, respectively, while remaining unchanged d-o-d. Overall, the market reflected a mixed sentiment, marked by stable trading activity and limited price fluctuations.

Imported, domestic market trends

Market participants reported that imported shredded scrap was offered at $355-360/t CFR Chennai, while HMS (80:20) scrap was quoted at $335-340/t. Buyers were bidding $5-10/t lower. Buying interest remained subdued as the strengthening US dollar increased landed costs. Additionally, the availability of relatively cheaper domestic scrap encouraged buyers to adopt a cautious approach toward fresh imported scrap bookings..

HMS (80:20) scrap prices in the domestic market were quoted at INR 30,500-31,000/t for spot deals with immediate payment. Transactions involving extended payment terms were concluded at higher levels of INR 31,000-31,500/t. Market activity remained largely concentrated within the INR 30,500-31,500/t range, with the majority of trades executed at these levels.

Imported arrivals slow, supply tight

According to market sources, an uptick in iron ore and pellet prices has prompted local sponge iron manufacturers to prioritise captive consumption rather than selling material in the merchant market. Meanwhile, mills are increasingly converting billets into rebar, as realisations from conversion are better than selling billets directly in the merchant market. Rebar demand is currently at a moderate level, while mill inventory levels are reported to be around 10-12 days.

A scrap supplier indicated that HMS (80:20) scrap prices are currently hovering in the range of INR 30,500-31,500/t, with variations driven by payment terms and mill-specific volume requirements. Improved rebar demand has eased liquidity conditions, with timely payment clearances supporting positive market sentiment. Additionally, scrap availability remains slightly tight, as imported scrap arrivals have slowed over the past couple of months due to higher import offer levels compared with domestic prices.

Regional comparison

In the Jalna market in western India, billet prices edged up by INR 100/t to INR 43,500/t, while rebar prices declined by INR 200/t to INR 49,100/t. HMS (80:20) scrap prices remained stable at INR 31,600/t. Finished steel trade activity slowed, as buyers are yet to lift previously booked material. Scrap availability remains comfortable, despite slight interruptions in movement due to increased vehicle checks at state borders.

Outlook

The domestic steel and scrap market is expected to remain range-bound. Moderate rebar demand and improved liquidity are supporting sentiment. Scrap prices are likely to stay firm due to limited imported scrap arrivals and captive consumption of sponge iron. However, cautious mill procurement and comfortable inventory levels may cap further upside. Overall price movement is expected within the INR +/- 200-500/t range.

Leave a Reply