- Singapore and Japan dominate bulk scrap sourcing

- Rebar prices stable, post-election optimism improves sentiment

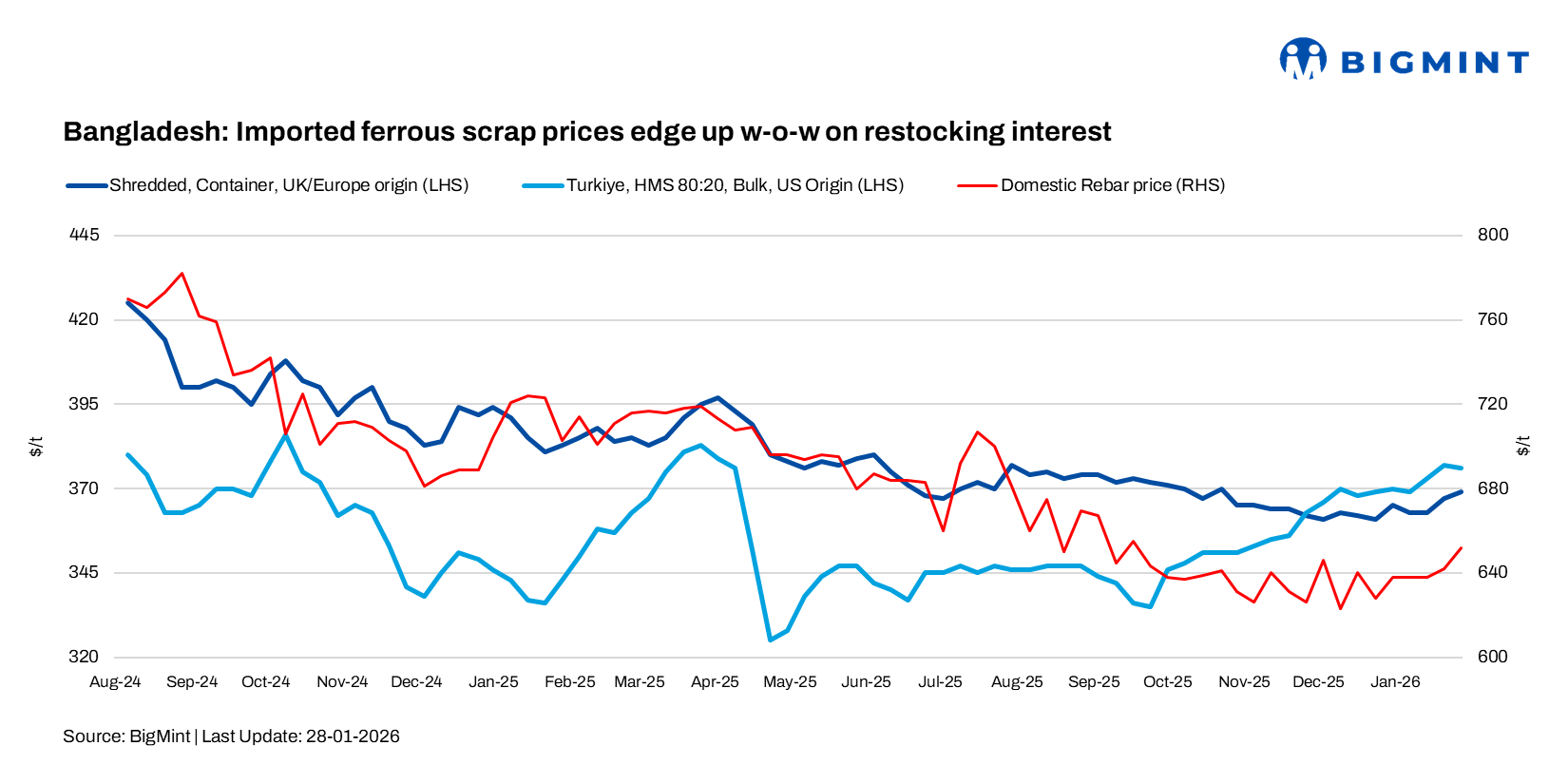

Imported ferrous scrap prices into Bangladesh improved week-on-week in the week ended 28 January, supported by firmer containerised cargo values amid a tightening global supply environment. Market participants noted a pickup in buying interest as mills returned to the market for restocking, with a clear preference for bulk scrap from Singapore and Japan. Improving scrap demand, combined with constrained availability from key origins, continued to lend upward support to prices despite cautious procurement strategies.

BigMint’s weekly assessments

- European-origin HMS (80:20) assessed at $348/t, up by $4/t w-o-w.

- European-origin containerised shredded increases by $2/t w-o-w to $369/t.

- Japanese-origin H2 bulk improved by $5/t w-o-w to $350/t.

- US-origin HMS (80:20) bulk stable w-o-w at $367/t.

A Chattogram-based scrap trader said imported ferrous scrap prices into Bangladesh firmed, supported by tighter global supply. “For bulk cargoes from East Asia, Japanese H2 is being quoted around $355-357/t CFR Chattogram, while HS scrap is heard at higher levels of $362-367/t. Premium grades remain scarce, with busheling from Hong Kong and Singapore offered at around $385/t CFR,” the trader noted, adding that mills are selectively booking based on grade availability and immediate requirements.

An Australia-based scrap trader said containerised scrap prices from Oceania have firmed amid renewed buying interest from Bangladesh. “HMS 80:20 is currently quoted at $345-350/t CFR Chattogram, while HMS 1 is offered at $355-360/t. Shredded scrap is being heard at $365-370/t, with PNS trading slightly higher at $370-375/t CFR,” he said. The trader added that Bangladeshi mills are focusing on selective containerised cargoes due to quicker delivery timelines, while tight availability from key origins continues to limit near-term downside risk.

Recent bulk deals (CFR Chattogram)

- Last week, two Singapore-origin bulk cargoes of HMS 80:20, each of 10,000 t, were concluded at $358/t and $362/t.

- A 25,000-t mixed bulk cargo from Japan, comprising H1/H2, HS, busheling, and shredded scrap, was traded at an average of $370/t CFR. H1/H2 was priced at $350-355/t, while HS and busheling were concluded at $380-385/t.

- Earlier, a 20,000-t Japan-origin cargo was sold, including 10,000 t of H2 at $345/t and 10,000 t of HS at $375/t CFR Chattogram.

Rebar market

A Chattogram-based trader said most mainstream rebar brands were trading in the range of BDT 75,000-80,000/t ($614-655/t), with market sentiment gradually improving. Industry participants expect larger mills to step up production after the elections, as improved liquidity and expectations of policy continuity in infrastructure and construction could support higher cargo bookings in the near term.

Ship recycling: Bangladesh slipped sharply in South Asia’s ship recycling rankings this week, with bidding activity remaining minimal and offers lagging India and Pakistan. Weak steel prices near $487/t, a stronger taka around BDT 122, and subdued resale demand continued to pressure recyclers, while political uncertainty and security concerns kept Chattogram largely inactive, with vessel deliveries limited in the near term.

Outlook

Imported scrap prices in Bangladesh are likely to remain firm in the near term, supported by tightening global supply and restocking demand. Containerised scrap from nearshore origins is expected to stay preferred due to quicker delivery timelines. Post-election clarity could gradually improve mill confidence and liquidity, though upside may remain capped by cautious procurement, still-fragile steel margins.

Leave a Reply