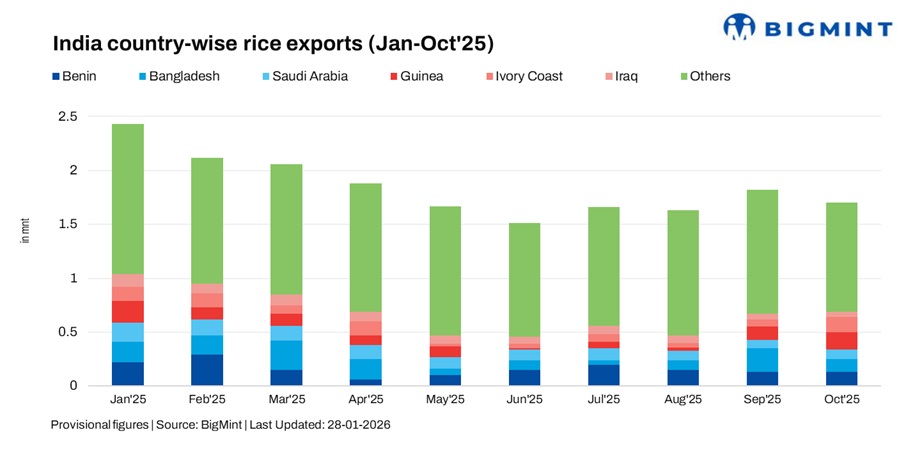

- West Africa supports flows, but demand remains cautious

- Freight sentiment mixed amid soft market conditions

India’s rice export vessel freight sentiment remained mixed this week, with bulk freights from the East Coast easing further on Africa-bound routes, while containerised movements from the west coast showed selective strength on a few Middle Eastern and East African lanes. Although Africa continued to dominate India’s rice export basket, weak fresh enquiries, elevated domestic prices and abundant vessel availability weighed on overall freight momentum.

Bulk shipments from the East Coast, particularly Kakinada, to West Africa remained operationally active; however, spot sentiment weakened as charterers delayed fresh cover amid subdued buying interest. Ample supramax availability and a lack of urgency among receivers limited owners’ pricing power, resulting in softer bulk freight indications despite steady export flows.

On the container side, shipments from the West Coast, mainly Mundra and JNPT, to the Middle East and East Africa remained largely rangebound. While some Middle East-facing routes firmed modestly, supported by liner capacity discipline and demand for faster deliveries, other lanes continued to face pressure due to cautious booking activity and destination-side risks.

Efforts to diversify export destinations amid reduced demand from traditional markets and ongoing payment risks are shaping a more selective shipment pattern, with exporters focusing on regular buyers and smaller parcels, which continues to influence freight sentiment. At the same time, India’s longer-term push to expand overall goods exports through policy reforms, port upgrades and logistics efficiency improvements is expected to provide structural support to agricultural export volumes, including rice, helping underpin vessel deployment and freight demand over time.

“Global rice prices remain under pressure due to abundant supplies and strong export volumes, particularly from India, which has pushed Asian prices to multi-year lows,” a market participant told BigMint.

Another source noted, “While global rice trade remains robust, weak price growth and ample supply are benefiting importers but squeezing exporter margins, as buyers increasingly benchmark prices against more competitive origins such as Thailand, Vietnam and Pakistan.”

“Container freight sentiment from the West Coast, particularly JNPT and Mundra, remains bearish due to low demand and limited fresh bookings,” a source mentioned.

Route wise updates

Meanwhile, according to few market participants, freight rates may move up or down by around 5-10%, subject to bunker (BAF) and currency (CAF) adjustments.

On the other hand, some market participants reported lower freight levels on the West Coast, particularly on the Mundra-Umm Qasr and Mundra-Jebel Ali routes, at around $19.2/t and $10.5/t, respectively. Sources attributed the decline to a generally weak market and softer sentiment in the Mediterranean sector, adding that freight rates may improve once European demand picks up.

Market highlights

- West Africa anchors exports: Steady buying interest from West Africa continues to underpin India’s rice export flows despite weaker bulk sentiment.

- Global oversupply pressures prices: Abundant supply and strong export volumes have pushed Asian rice prices to multi-year lows, squeezing exporter margins.

- East Coast bulk freights under pressure: Limited fresh cargoes and ample vessel availability continue to weigh on East Coast freight sentiment.

- Selective West Coast container firmness: Liner capacity discipline is supporting select Middle East and East Africa routes.

- Red Sea risk eases: Red Sea-related risks have eased slightly, with some carriers gradually restoring Suez routings, potentially shortening voyage distances.

- Bunker prices remain soft: Bunker prices have stayed largely stable to soft, easing cost pressure on freight rates.

Outlook

Looking ahead, India’s rice export vessel freights are expected to remain largely stable with a softer bias in the near term. While West Africa-led demand should continue to provide a base level of support, upside is likely to remain capped by high domestic prices, weak global price momentum, abundant supply and rising competition from other exporting origins.

Market participants expect shipment activity to stay subdued into mid-February, with only a gradual improvement possible if domestic prices ease and buying interest improves. Continued global oversupply, destination-side risks and geopolitical uncertainty across the Middle East and parts of Africa are expected to keep overall freight sentiment cautious rather than bullish.

Leave a Reply