- USGC prices softened under freight and weak Asian demand

- USWC prices surged on strong Chinese low-sulfur demand

Global pet coke markets showed clear regional divergence through the week. Prices along the U.S. Gulf Coast (USGC) softened marginally, while the U.S. West Coast (USWC) extended a multi-week rally. Delivered markets-Turkey and India-remained firm, though buying appetite diverged sharply.

USGC FOB prices for high- and mid-sulfur pet coke slipped by $0.50/mt across grades, reflecting pressure from rising freight and limited Asian buying interest. By contrast, USWC prices strengthened further. FOB 4.5% sulfur pet coke rose to $87.00/st, while low-sulfur 2.0% material surged to $145.00/st, a nine-month high, driven by sustained Chinese demand and tight availability.

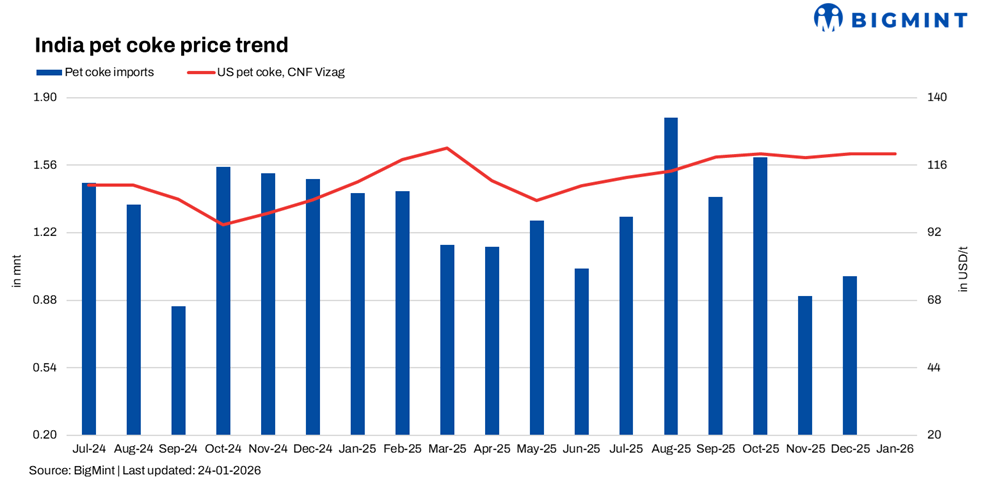

In delivered markets, CIF Turkey prices edged higher to $106.00/mt as cement demand remained strong. Indian domestic market intelligence showed CNF offers holding firm at $118-120/mt. Buyers continued to cap bids at $114-115/mt, maintaining a consistent bid-offer spread. Venezuelan pet coke was discussed as an alternative around $117/mt, though volumes were limited.

Market Drivers: Freight, Sulfur Segmentation, and Fuel Economics

The softening at USGC was freight-led rather than demand-led. Freight rates from the USGC to India rose by roughly $2.75/mt, forcing suppliers to adjust FOB prices to defend delivered competitiveness. At the same time, muted Chinese interest in high-sulfur material reduced an important outlet for USGC barrels.

USWC strength reflects a structurally different dynamic. Chinese demand for low- and mid-sulfur pet coke-particularly from glass and specialty industrial sectors-remains firm, while supply of low-sulfur material is inherently constrained. This sulfur-driven segmentation continues to widen the USWC premium over USGC.

Turkey’s firmness was supported by rising construction activity and seasonal tightness in alternative fuels. Weather-related disruptions to Russian thermal coal flows improved pet coke’s relative economics despite higher freight.

India remained the most price-sensitive market. Sellers kept offers elevated, supported by global tightness and stronger pull from Turkey and Brazil. Buyers resisted amid rupee weakness and high landed costs, increasingly evaluating thermal coal substitution where technically feasible. Import volumes remained subdued, reinforcing the stalemate.

Near-Term Outlook: Rangebound, Grade-Selective

In the near term, USWC prices are likely to stay firm as long as Chinese demand persists, though upside may be limited by already high absolute levels. USGC prices may remain under pressure if freight stays elevated and thermal coal continues to compete aggressively.

In India, a breakout in trade activity is unlikely without either currency relief or a narrowing of the pet coke-coal spread. Structurally, pet coke is increasingly treated as a premium, tactical fuel rather than a baseload option, with buying decisions tightly anchored to relative fuel economics rather than outright demand growth.

Leave a Reply