- Lumps bids stable, fines rise INR 425/t m-o-m at OMC auction

- Portside South African thermal coal prices rise to 1-year high

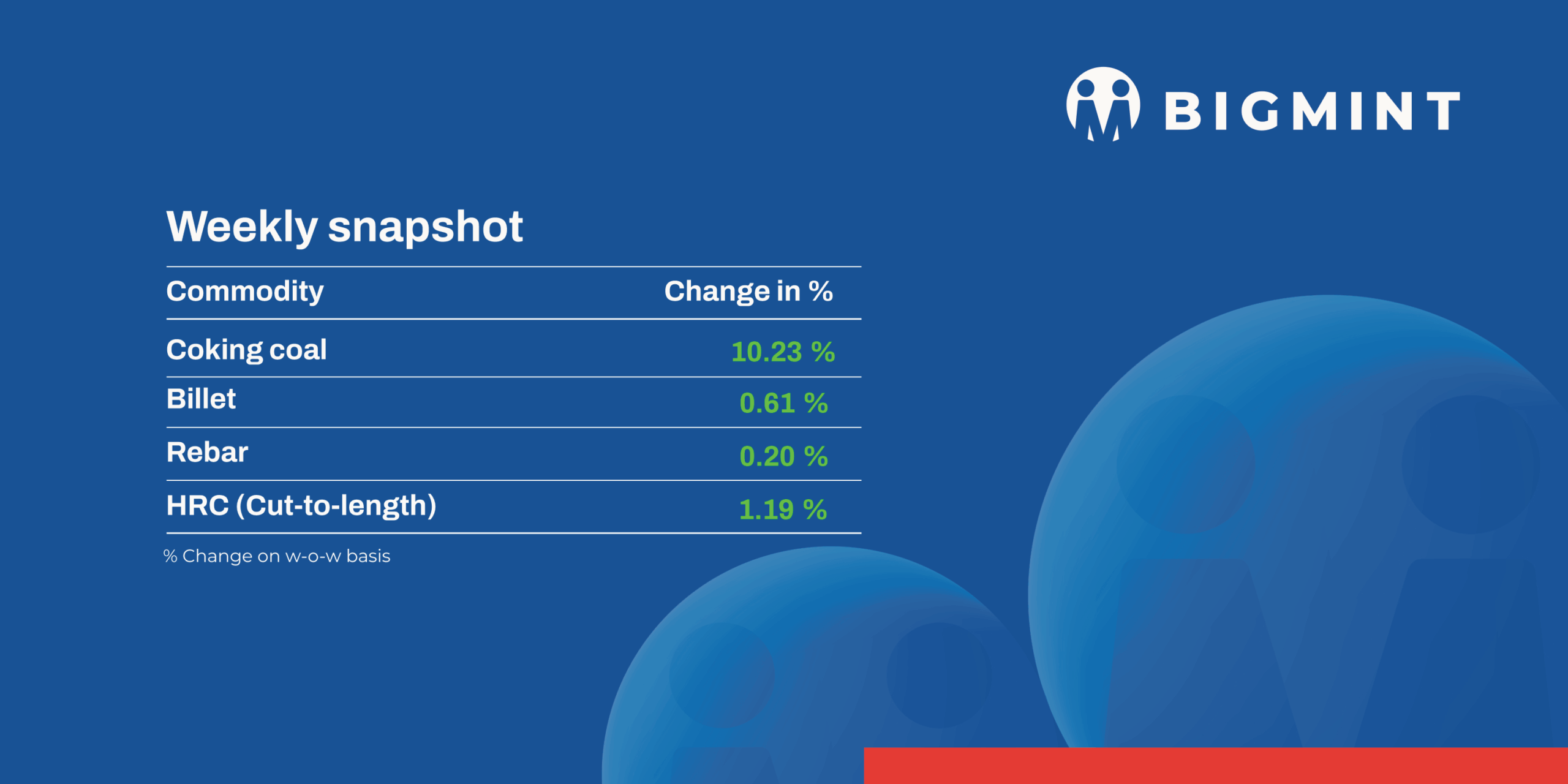

The domestic steel and raw materials markets saw mixed price trends during week 4 (19-23 January 2026). Semi-finished steel prices varied in the range of INR 50-1,300/tonne (t), while flat steel and rebar prices climbed higher. Firm raw material prices supported steel prices despite cautious trade activity.

Iron ore, pellet

- OMC’s auctions on 19 January 2026 witnessed strong demand across lumps and fines. The entire 1.414 mnt of lumps (Fe 60-65%) offered were booked at INR 5,500-7,700/t, with weighted average bids largely stable m-o-m despite an INR 800/t hike in base prices. Meanwhile, 2.03 mnt (91%) of the 2.24 mnt fines (Fe 51-62%) on offer were booked, with the weighted average price rising by INR 425/t m-o-m, supported by firm steel and sponge CDRI prices and positive demand expectations.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index fell by $3/t w-o-w to $64/t FOB east coast, while the CFR China index stood at $73.5/t. Despite weak sentiment and lower realisations, around 450,000 t of Fe 55-57% fines were traded in the seaborne market last week. Discounts widened to about 23-25% for Fe 57% and nearly 29-30% for Fe 55% material versus the global fines index.

- In NMDC’s Chhattisgarh auction on 22 January 2026, 21,500 t of DR CLO (Fe 67%) were booked at a 13.5% premium over the base price of INR 5,190/t, while 45,500 t of ROM (Fe 65.5%) were sold at INR 4,540/t. Meanwhile, 68,100 t of Fe 60% fines remained unsold at a base price of INR 3,150/t, whereas 21,500 t of Fe 64% fines were booked at INR 3,930/t from the Kirandul mines.

Coal

- South African thermal coal prices at Indian ports strengthened further, reaching a one-year high as tight portside stocks, firmer global indices and higher freight costs pushed offers up. As per BigMint’s assessment, exw-Paradip 5,500 NAR rose by INR 250/t w-o-w to INR 9,400/t, while 4,800 NAR increased by INR 300/t to INR 8,100/t. At Vizag, 5,500 NAR climbed by INR 250/t to INR 9,250/t and 4,800 NAR jumped by INR 350/t to INR 7,950/t. Despite higher prices, trades remained selective, with limited deals around INR 9,000-9,100/t.

- Domestic non-coking coal prices remained unchanged w-o-w, with 5,000 GCV assessed at INR 5,750/t and 4,500 GCV at INR 4,800/t.

- BigMint’s premium hard coking coal index surged by $17/t w-o-w to $264/t CNF Paradip on 23 January 2026, supported by a reported 75,000-t cargo sale at $250/t FOB Australia. Australian coking coal prices rose further as heavy rainfall from Cyclone Koji disrupted mining and port operations, with vessels awaiting berthing.

- Indian BF-grade metallurgical coke prices rose w-o-w, supported by a sharp rally in coking coal prices, though spot trade activity remained subdued. In eastern India, BF-grade met coke prices increased by INR 1,200/t to INR 33,500/t ex-Jajpur, driven by higher raw material costs and firmer upstream sentiment. In contrast, western India prices stayed unchanged at INR 30,100/t ex-Gandhidham due to comfortable supply and weak buying interest.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices inched up by INR 875/t ($10/t) w-o-w to INR 71,900-72,700/t ($785-794/t) across Durgapur, Raipur, Vizag, and Raigarh. Strong domestic demand, limited supply, and rising imported manganese ore costs supported prices. Although steel mills remained cautious, improving buying interest reflected a positive market outlook.

- Ferro manganese: Indian ferro manganese (70%) prices rose by INR 600/t ($7/t) w-o-w to INR 72,500/t ($791/t) in Durgapur and Raipur. The increase was supported by firmer seller offers and improved buyer acceptance of higher quotations, reflecting steady demand and a stable to positive market sentiment.

- Ferro chrome: Domestic high-carbon ferro chrome (60%, Si: 4%) prices increased by INR 6,100/t ($67/t) w-o-w to INR 112,600/t ($1,229/t) exw-Jajpur. Limited material supply and strong export realisations due to firm demand from China encouraged sellers to increase their offers. Additionally, OMC is set to auction 3,000 t high carbon ferro chrome on 27 January, with the 1,500 t lot priced at INR 104,500/t exw.

Semi-finished

- India’s semi-finished steel market witnessed mixed sentiment during the week, as per BigMint’s assessment. Billet prices increased by INR 50-1,600/t across most regions on a w-o-w basis; however, enquiry levels remained moderate, and trade activity was limited. In contrast, the western market saw prices decline by INR 300-1,000/t due to weak enquiries and low acceptance of higher offers. Muted finished steel demand kept prices largely stable, with buying largely need-based.

Metallics

- Meanwhile, the sponge iron market witnessed firm support during the week. Prices across key producing regions increased by INR 50-1,200/t on a w-o-w basis, supported by a marginal improvement in buyer enquiries. Rising raw material costs and supply-side constraints further underpinned prices. However, overall trade volumes remained limited, with transactions largely confined to need-based buying.

Finished long steel

- IF-rebar: IF-route rebar trade prices witnessed an upward trend on a w-o-w basis across major Indian markets, mainly due to sellers holding future booking orders. However, market activity remained subdued at elevated prices. Fresh bookings were limited despite higher offers, as many buyers had already procured material in the previous week. Weakness in semi-finished steel further weighed on sentiment, prompting buyers to adopt a wait-and-watch approach before making bulk purchases. Under the current scenario, prices are expected to remain range-bound in the next week.

- On a w-o-w basis, rebar prices increased by INR 100-1,000/t w-o-w across regions except in Ahmedabad, where prices fell by INR 400/t, as per BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 43,700-44,100/t exw Raipur and INR 49,300-49,900/t exw Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 46,000-46,400/t exw-Raipur.

- Trade reference prices of wire rod stood at INR 44,000-44,800/t ex-Raipur.

- BF-rebar: Indian Tier-I mills increased rebar prices by up to INR 1,250/tonne (t) ($14/t) this week, sources informed BigMint. Post-revision, list prices stood at INR 54,500-55,500/t ($593-604/t) on landed basis. Following this, trade-level blast furnace (BF) rebar prices (distributor to dealer) rose w-o-w across major Indian markets. Strong material lifting was observed in the trade channel this week, as per market participants.

- Trade-level BF-rebar (distributor to dealer) prices rose by INR 1,500/t ($16/t) w-o-w to INR 55,300/t ($601/t) exy-Mumbai as per BigMint’s assessment on 23 January 2026. Prices exclude GST at 18%.

- In the projects segment, prices hovered at around INR 54,500-56,000/t ($593-609/t) FOR Mumbai basis. Robust demand from the infrastructure and construction segments led to a material shortage at mills, supporting prices. Some offers were heard higher than these levels due to shortages.

Flat steel

-

- Trade-level prices of hot-rolled coils (HRC) in India increased w-o-w following the announcement of price hikes by mills, with HRC prices assessed in the range of INR 50,000-52,900/t ($550-581/t). In line with this trend, cold-rolled coil (CRC) prices also edged up w-o-w, with prices assessed at INR 54,500-60,500/t ($599-665/t).

- Last week, festive holidays kept demand and trading subdued. However, this week, mill-led price hikes sparked a rebound in trade-level prices as activity resumed post-festivities. While demand remained moderate, fewer working days from bank holidays on Saturday and Monday pushed participants to liquidate swiftly for payment management.

- India’s bulk imports of HRCs touched 151,637 t as of 16 January, based on vessel line-up data. Around 165,079 t of additional cargoes are expected by early-February.

- India’s bulk exports of HRCs touched 20,253 t as of 16 January, and around 155,800 t of additional cargo are being shipped.

- BigMint’s Indian HRC (S275) export index for the European Union (EU) remained unchanged w-o-w at $505/t FOB main port. Meanwhile, India’s HRC (SAE 1006) export index for the Middle East and South East Asia rose by $5/t w-o-w to $480/t FOB main port from $475/t a week earlier, following a recently concluded deal.

Leave a Reply