- LME prices rise 7% y-o-y in CY’25, stocks down 37%

- Structural aluminium deficit likely in 2026

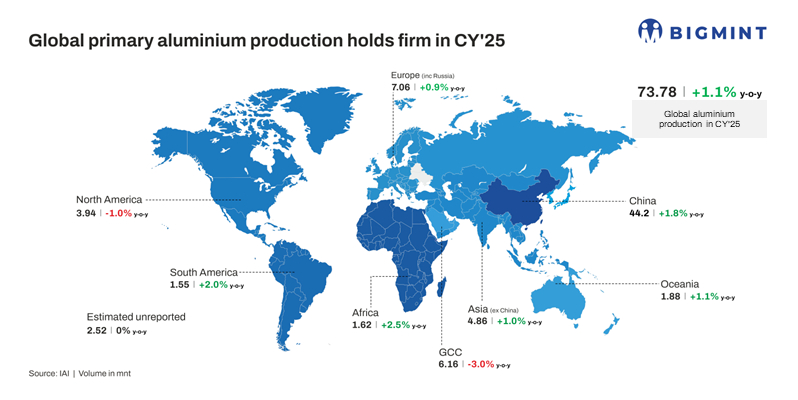

Global primary aluminium production stood at 73.78 million tonnes in calendar year (CY) 2025, marking a 1.1% y-o-y increase from 73.01 million tonnes in CY’24. The marginal rise reflects largely steady output across major producing regions, with stable smelter operations balancing periodic demand variations and region-specific supply realignments.

Country-wise breakdown

China, the world’s largest aluminium producer, reported output of 44.20 mnt in CY’25, up 1.8% y-o-y from 43.40 mnt in CY’24, reinforcing its dominance in global supply. Africa’s production increased 2.5% y-o-y to 1.62 mnt, while South America posted a 2.0% y-o-y rise to 1.55 mnt, reflecting steady capacity utilisation across both regions.

In contrast, North American output slipped 1.0% y-o-y to 3.94 mnt. Asia (excluding China) recorded a 1.0% y-o-y increase to 4.86 mnt, and Europe (including Russia) saw production edge up 0.9% y-o-y to 7.06 mnt. Oceania’s output grew 1.1% y-o-y to 1.88 mnt, while the GCC region registered a sharper 3.0% y-o-y decline to 6.16 mnt. Estimated unreported production remained flat at 2.52 mnt.

Overall, global aluminium production in CY’25 displayed mixed y-o-y trends, with growth in China, Africa and South America offset by contractions in North America and the GCC, underscoring regional divergences in smelter operations and cost dynamics.

Slow-paced expansion in primary supply

China continued to anchor global aluminium supply in CY’25, but output growth remained moderate as production operated close to the country’s policy-mandated capacity ceiling. As the dominant producer, accounting for nearly 60% of global output, China’s annualised production is approaching the 45 mnt cap aimed at curbing overcapacity and environmental impact. This has sharply limited headroom for fresh supply additions, slowing global growth despite steady demand from transport, construction and energy sectors. Incremental gains largely came from efficiency improvements and stable utilisation rather than new capacity.

Input-side dynamics also influenced production trends. Alumina operating rates in China softened during the year due to environmental restrictions, maintenance activity and operational adjustments, leading to a decline in metallurgical-grade alumina output. Seasonal maintenance and equipment upgrade further tightened feedstock availability at times, directly constraining smelter throughput even though overall alumina capacity remained ample.

Production in Africa and South America improved on the back of consistent smelter operations, access to bauxite and alumina feedstock, and comparatively lower operating costs. These regions benefited from stable capacity utilisation and gradual downstream demand support, allowing output to rise steadily without major disruptions.

In contrast, North American aluminium output edged lower, reflecting persistent structural challenges such as high energy costs, limited investment in new primary smelting capacity and an increasing shift toward recycled aluminium. Trade policies and cost pressures continued to undermine smelter competitiveness, restricting any meaningful recovery in production.

Asia outside China and Europe recorded only marginal growth, pointing to a cautious operating environment. While industrial demand provided some support, elevated power prices, regulatory constraints and lingering cost pressures-especially in Europe-capped stronger gains. Many producers focused on optimising existing assets rather than expanding capacity.

Oceania’s output rose slightly, supported by stable smelter operations and export-oriented demand, though producers remained sensitive to energy pricing and input cost volatility. The increase largely reflected operational stability rather than expansion.

The GCC region, however, saw a notable decline in production, driven by shifting production strategies, maintenance schedules and adjustments to global demand and trade flows. Some producers also prioritised downstream or value-added segments over maximising primary metal output.

Overall, global aluminium supply in CY’25 showed mixed regional trends, shaped by policy-driven capacity constraints, input material dynamics, energy economics and strategic operational choices, resulting in only modest net growth despite divergent regional performances.

Impact of pricing

Aluminium prices on the LME increased by $178/t y-o-y in CY’25 reaching $ 2,635/t from $2,457/t. Meanwhile, stocks on LME saw a 37% drop in CY’25 settling at 0.48 mnt as against 0.76 mnt.

Aluminium prices have strengthened sharply y‑o‑y, driven by tightening supply conditions and supportive macro sentiment. China, the world’s largest producer, remains close to its 45 mnt capacity caps, limiting incremental supply despite firm demand. Additional supply pressures have arisen from smelter disruptions and uncertain power contracts in regions like Iceland and Mozambique.

Higher US import tariffs have tightened trade flows, lifted regional premiums, and constrained physical availability, particularly in Western markets. LME aluminium prices have already breached the $3,000/t mark, trading around $3,100-$3,150/t in mid-January 2026, while inventories remain tight. Against this backdrop, market participants expect the aluminium market to enter a structural deficit in 2026, supporting the likelihood of sustained high prices.

Outlook

Global aluminium supply is expected to remain moderately constrained in the near term, as China operates near its 45 mnt capacity ceiling and new additions in other regions remain limited. Seasonal maintenance, feedstock availability, and energy cost pressures in key producing regions are likely to continue affecting output, keeping overall production growth modest. Meanwhile, robust demand from transport, construction, renewable energy, and electrification trends is expected to persist, supporting strong pricing momentum. With LME prices having already surpassed $3,000/t and inventories remaining tight, the market is likely to face a structural deficit through 2026, suggesting continued upward pressure on aluminium prices and a firm outlook for global supply-demand dynamics.

Leave a Reply