- Safeguard duty curbs HRC imports, tightens domestic supply

- Rising coking coal costs, stable iron ore lift production expenses

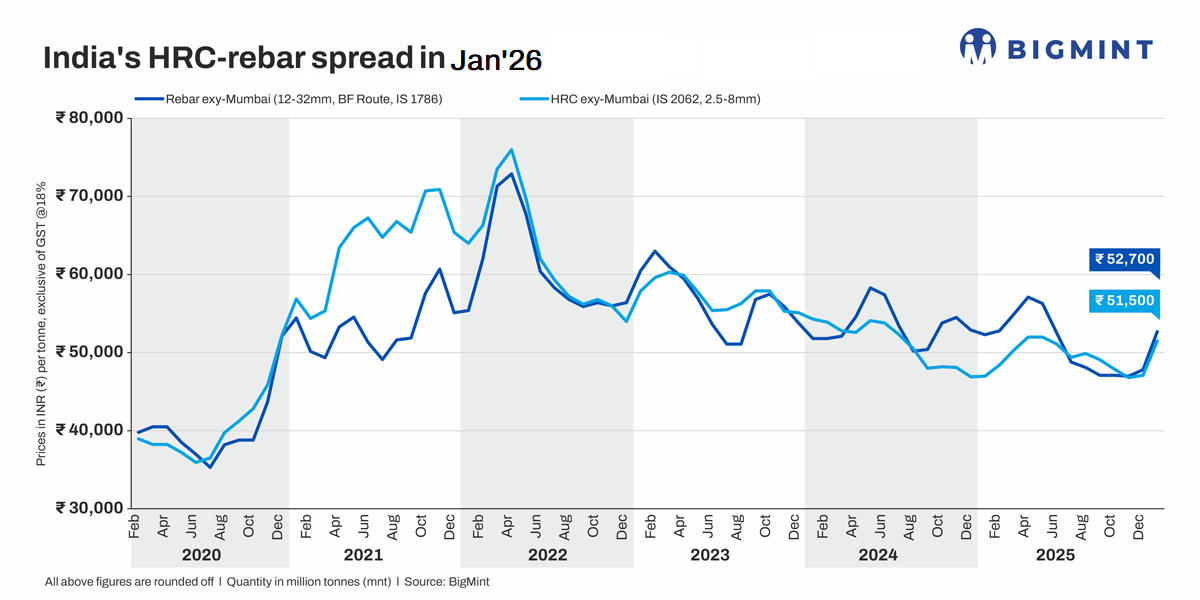

Indian steel prices traced a pronounced U-shaped trajectory between January 2025 and January 2026, sliding to five-year lows in October-November before rebounding sharply from December as cost pressures, particularly higher coking coal prices, policy support, and tighter market discipline reasserted themselves. The late-2025 trough marked a critical inflection point in the current steel cycle.

Domestic hot-rolled coil (HRC) and rebar prices weakened steadily through most of CY’25, bottoming out in October and November when prices slipped to the INR 47,000-48,000/tonne (t) range. HRC traded near INR 47,150/t, while rebar (TMT) hovered around INR 46,500-47,000/t, levels last seen in 2020 during the pandemic-led slowdown. The downturn was driven by weak export demand, aggressive global supply, especially from China, and steady inflows of imported finished steel, which capped any seasonal price recovery despite only moderate domestic demand softness.

Imports retreat as policy support kicks in

The imposition of safeguard duty on HRCs emerged as a key turning point in Q4CY’25, curbing low-priced imports and tightening domestic availability. India saw steel imports of around 9.56 mnt in CY’25, declining 13% from 10.99 mnt in CY’24, while exports stood at 8.59 mnt, keeping the country a net importer. With the safeguard duty discouraging opportunistic HRC inflows, import pressure increasingly translated into firmer domestic pricing discipline rather than outright volume stress.

Costs tighten even at the trough

Crucially, the price collapse was not matched by a meaningful easing in raw material costs. Iron ore prices (lumps, Odisha Index, India, 10-30mm, Fe 63%, BF grade) remained relatively stable at INR 6,200-7,450/t in CY’25, while premium hard coking coal, after touching near-term lows around $205/t CFR in October, firmed from November and rose further into December and January. This lagged pass-through of higher replacement costs compressed mill margins in Q4, limiting further downside and setting the stage for a sharp correction once mills regained pricing leverage.

BigMint’s coking coal (PHCC) index surged from $215/t CFR India in January 2025 to $247/t CFR India last week, marking a steep late‑year escalation after a largely range‑bound first half in CY’25. Weather-related disruptions in Australia, owing to heavy rainfall from Cyclone Koji, have prompted a few miners to go for force majeure, which have resulted in limited offers in the market in early-January 2026. The Indian rupee’s depreciation against the US dollar further boosted the landed costs of coking coal in India.

Rebound gathers pace in Dec-Jan

The recovery accelerated decisively from December 2025, with mills announcing repeated price hikes through January 2026. Cumulative increases during January ranged from about INR 2,500/t to over INR 6,000/t across producers and regions, pushing HRC (2.5-8mm/CTL, IS2062, Gr E250 Br.) prices to INR 52,000-52,500/t exy-Mumbai and rebar prices (12-32mm, BF Route, IS 1786 Fe 550D) to INR 55,000-55,500/t exy-Mumbai. Project-linked transactions were concluded at even higher levels, around INR 54,000-56,000/t. Market participants said the frequency and magnitude of the hikes reflected mills’ urgency to restore margins amid rising coking coal costs and improved order visibility after the year-end slowdown.

Outlook

Steel prices are expected to maintain a firm to positive bias in early 2026, at least through February 2026, supported by safeguard duty-led import moderation, elevated coking coal costs, disciplined supply management, and stronger pricing resolve from mills. Improved order visibility and front-loaded buying activity, as consumers accelerate procurement to complete projects ahead of the end of FY’26, are also likely to lend near-term support to prices.

Leave a Reply