- HRC offers to EU, Middle East remain stable w-o-w

- Weak EU domestic demand offset by firm sentiment

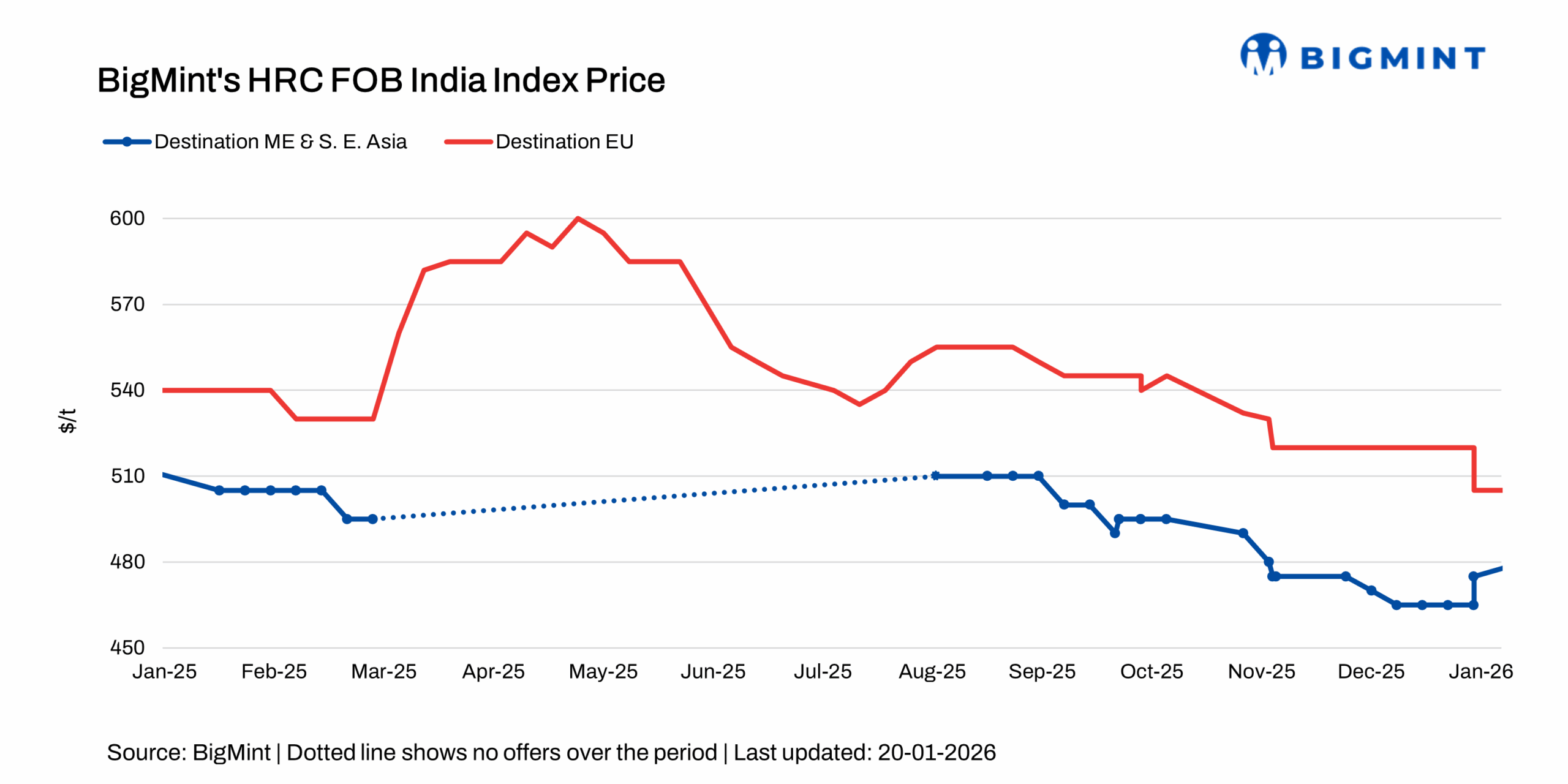

BigMint’s Indian HRC (S275) export index for the European Union (EU) remained unchanged w-o-w at $505/t FOB main port. Meanwhile, Indian HRC (SAE 1006) export index for the Middle East and South East Asia rose by $5/t w-o-w to $480/t FOB main port from $475/t a week earlier, following a recently concluded deal.

1. HRC offers to the EU: Indian HRC export offers to the EU remained stable w-o-w at $555/t CFR Antwerp, unchanged from the previous week. A BigMint source indicated that “cautious market sentiment continues to weigh on trading activity, keeping the market slow.”

However, the European flat steel market sentiment remained slightly positive in mid-January, supported by strong order books at domestic mills and reduced import availability following the implementation of CBAM. Buyers are increasingly preferring domestic material due to uncertainty surrounding carbon-related costs and safeguard measures, while mills remain comfortably booked for the first quarter. Despite seasonally weak post-holiday demand, expectations remained firm on anticipated trade shifts and limited import risk.

2. HRC offers to the Middle East: Indian HRC export offers to the Middle East remained stable w-o-w at $500/t CFR UAE, moreover, a deal of around 25,000 t has been heard concluded at similar levels for February shipments. However, demand in the region remained moderate.

China’s HRC export offers to the Middle East stood at $500/t CFR UAE, up by around $10/t w-o-w as compared to $490/t last week. A BigMint source noted, “Market sentiment has turned firmer, with mills pushing offers higher, a trend typically observed in China ahead of the Lunar New Year holidays.” May 2026 HRC contracts on the Shanghai Futures Exchange (SHFE) declined by RMB 21/t ($3/t) w-ow to RMB 3,288/t ($472/t) on 20 January from 3,309/t ($475/t) on 13 January 2026.

Outlook

The Indian HRC export market is expected to remain volatile in the coming week, with clearer price direction likely to emerge as demand trends become more visible. Sentiment in the EU may remain supported by firm domestic mill order books and subdued import appetite amid CBAM implementation. Meanwhile, demand in the Middle East remains moderate, limiting any meaningful price upside despite firmer Chinese offers.

Leave a Reply