- Low-alumina pellets witness selective demand

- Chinese mills seek to save steel margins

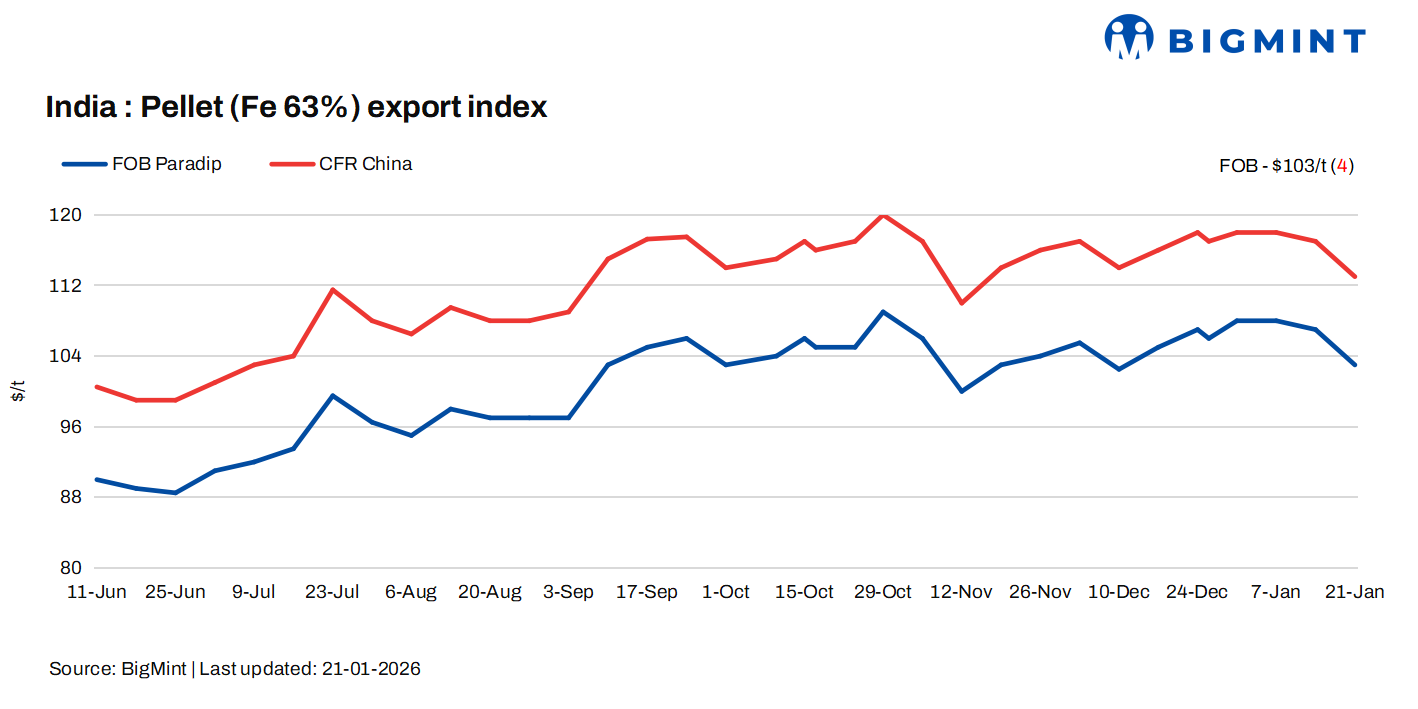

Pellet export prices for East Coast India-origin material declined by around $3-4/t this week, prices assessed on 21 January 2026, tracking the fall in global iron ore prices and subdued demand in the seaborne market.

Price update

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index fell by $4/t w-o-w to $103/t FOB east coast on Wednesday. No deals of pellet exports were heard from east coast amid better domestic realisation and lower bids in the seaborne market. The sellers are holding their export offers and waiting for a recovery in the global prices.

The suppliers are actively offering their pellet cargo for Fe 63-64% material. A deal of 60,000 t of pellet export (Fe 64%) was heard at $130-132/t CFR China concluded by a producer last weekend.

Market movement

Sources highlighted that the decline was largely driven by the presence of multiple unsold Indian pellet cargoes at Chinese ports, coupled with weak spot demand from Chinese buyers. A trader said, “The market is facing an oversupply situation in China, especially for standard-grade material, which is putting pressure on prices.”

Buyers have shown limited interest in Fe 63% pellet cargoes, particularly when sellers’ offers remained above prevailing bid levels. Market participants noted that Chinese mills are becoming increasingly price-sensitive and are avoiding higher-priced deals amid margin pressures. An international market player said, “There is a clear mismatch between bids and offers, which is restricting deal flow.”

However, higher-grade low-alumina pellets continue to see selective demand, supported by efficiency-driven procurement strategies at some mills. One shipment deal for premium-grade material was reportedly concluded last week, indicating that niche demand still exists in the market.

International traders pointed out that persistent weakness in iron ore swaps has led to instability in seaborne prices. Additionally, demand has softened further as Chinese mills remain reluctant to book pre-holiday delivery cargoes, preferring to delay procurement. Another source mentioned, “Mills are focusing on cost optimisation to protect steel margins and are largely avoiding average-grade pellet cargoes.”

On the supply side, sellers have kept their cargoes in the market but are exercising caution in concluding deals at lower price levels. Many exporters are waiting for improved price realisation before committing volumes.

Market participants expect the pellet export market to remain volatile in the near term. Better clarity on price direction may emerge once active export deals for Fe 63% pellet cargoes are concluded, which could help establish a more stable benchmark for the market.

Domestic vs export market

Domestic prices exceeded export realisations by around INR 800/t ($3/t), with the gap widening w-o-w. Pellet (Fe63%) prices in Odisha’s Barbil were recorded at INR 8,500/t ($94/t) exw, rising by INR 250/t ($2/t) last weekend. Hike in OMC’s recent iron ore fines auction have supported pellet offers. Meanwhile, the ex-plant realisation in exports from Barbil fell w-o-w to INR 7,700/t ($88/t) exw.

Rationale

- No confirmed deal from India’s east coast was recorded in this publishing window for T1 trade. Thus, this category was allotted 0% weightage for today’s price calculations. Click here for the detailed methodology.

- Eleven (11) indicative prices were received, and seven (7) were considered for the calculation of the index and given a balance 100% weightage.

Factors impacting pellet exports

- Chinese iron ore fines prices down w-o-w: The benchmark iron ore fines Fe 61% index fell by $4/t w-o-w to $104/t CFR China on 20 January. Prices fell amid weak downstream steel fundamentals, which continued to weigh on sentiment. Despite the decline, market offers remained competitive to protect margins amid steady pre-Lunar New Year liquidity. Meanwhile, Brazilian cargoes underperformed due to quality and logistics issues, while Australian material was preferred.

- DCE iron ore futures fall w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2026 contract closed at RMB 784/t ($114/t) on 21 January, dropping by RMB 37/t ($6/t) w-o-w.

Outlook

Leave a Reply