- Global iron ore supply growth to outpace demand in 2026

- Iron ore prices forecast to soften to $92-98/dmt range

Mysteel Global: Global iron ore supply is expected to grow at a faster pace this year, driven by increased production from major miners, while demand will see only modest growth in line with a slight increase in worldwide pig iron production, Mysteel predicts in its newly published annual report for the commodity. The widening supply surplus will continue to weigh on iron ore prices in the year ahead, it concludes.

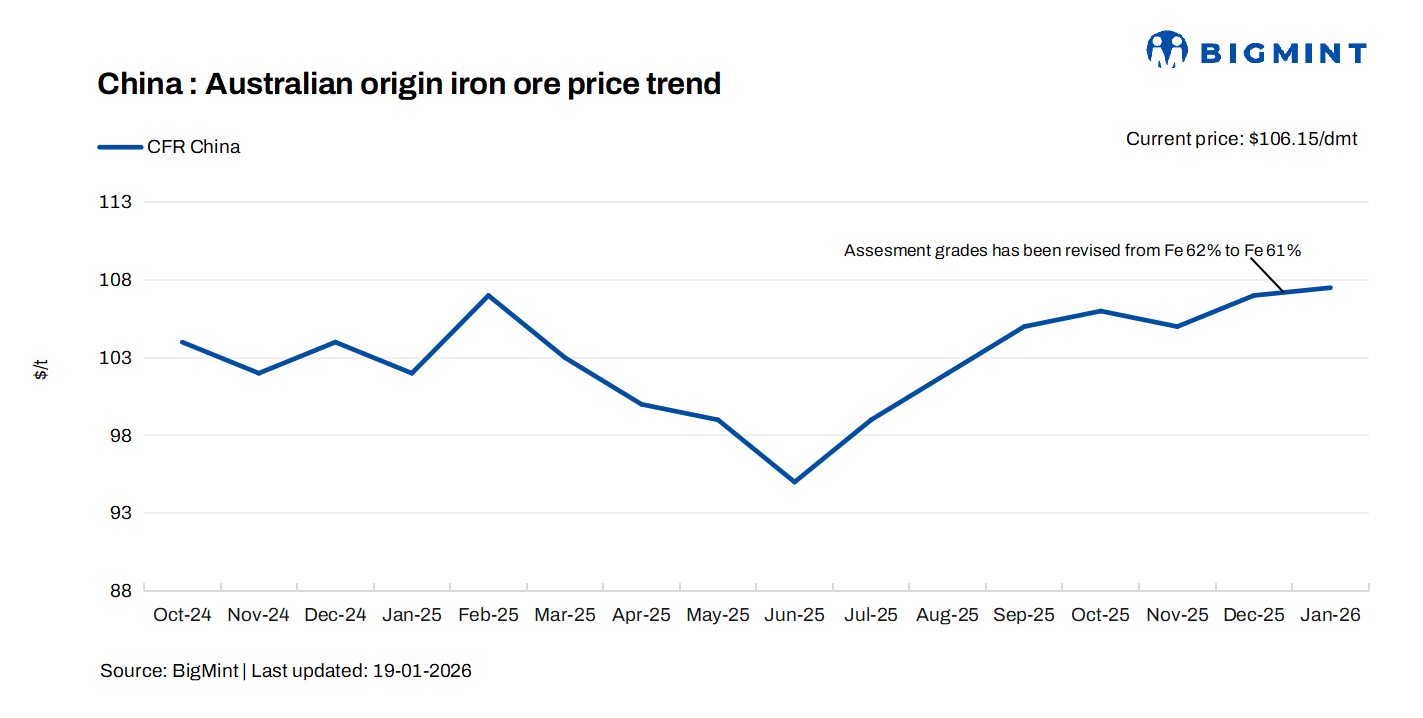

Last year, the average price of seaborne 62% Australian iron ore fines was assessed by Mysteel at $102/dmt, 6.8% lower than the $109/dmt in 2024. The decline mainly reflected a persistent oversupply of the steelmaking material in the global market, the report said.

On the supply side, global iron ore output is estimated to have reached 2.61 billion tonnes (bnt) in 2025, up by 40 million tonnes (mnt) on year, with global iron ore shipments in the same year also increasing by 45.6 mnt on year to 1.65 bnt, according to Mysteel’s tracking. Largely responsible for the growth were major miners such as Rio Tinto, BHP, and Vale, who continued to expand capacity and improve operational efficiency.

On the other hand, iron ore demand also increased last year, though at a slower pace. Global pig iron output is thought to have risen by 19.7 mnt on year to reach 1.29 bnt. As a result, the global iron ore surplus in 2025 is estimated to have surged by 11 mnt or 68% from 2024 to reach 26.3 mnt, according to the report.

Despite the softening of iron ore prices amid oversupply, prices actually outperformed expectations last year, with those for 62% Australian iron ore fines staying above $100/dmt for more than two-thirds of the year. Moreover, the on-year drop in iron ore prices was also smaller than that seen in steel prices.

The report attributed the relative resilience in iron ore prices last year mainly to steady demand from China, the world’s largest iron ore consumer. Mysteel’s tracking of the 247 Chinese blast-furnace steelmakers showed that their total hot metal output in 2025 increased by 2.7% y-o-y to 863.8 mnt. Consequently, these mills’ consumption of imported iron ore during the same year also rose by 3.6% on year to 1.07 bnt.

China’s strong appetite for iron ore last year was also evidenced by the country’s record-high imports of the raw material, where the total reached 1.26 bnt, up by 1.8% from the previous record set in 2024, as reported.

The report also notes that thin profit margins have led Chinese steelmakers to increasingly favour medium- and low-grade ores in recent years. For example, the average iron grade of sintered ore used by the surveyed Chinese steel mills last year fell by 0.09 percentage points y-o-y to 55.25%.

Looking ahead to this year, global pig iron output is anticipated to grow by 15 mnt y-o-y to 1.3 bnt in 2026, supported by robust steel production outside China. The central government in Beijing is aiming to control steel output, as reported.

However, the growth in iron ore demand will be overshadowed by the expansion of supply, as global iron ore miners will continue to ramp up capacity. Total iron ore output in 2026 is estimated at 2.68 bnt, up by 65 mnt on year. The increment will primarily come from traditional mining giants in Australia and Brazil, as well as Guinea’s Simandou project, which was commissioned late last year and is scheduled to gradually ramp up to its full capacity of 120 mnt/year by around 2030.

In summary, the global iron ore surplus this year is expected to expand by 12.2 mnt from 2025 to 38.45 mnt, leading to rising stocks at mines, ports, and in transit. Notably, total stockpiles of imported iron ore across China’s 45 major ports under Mysteel’s regular tracking had already hit a record high of 165.6 mnt as of 15 January.

Under persistent oversupply pressure, the average price for seaborne 62% Australian iron ore fines this year is expected to fall to $92-98/dmt, the report forecasts.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply