- Tight inventories continue to support prices

- TC/RCs signal upstream market tightness

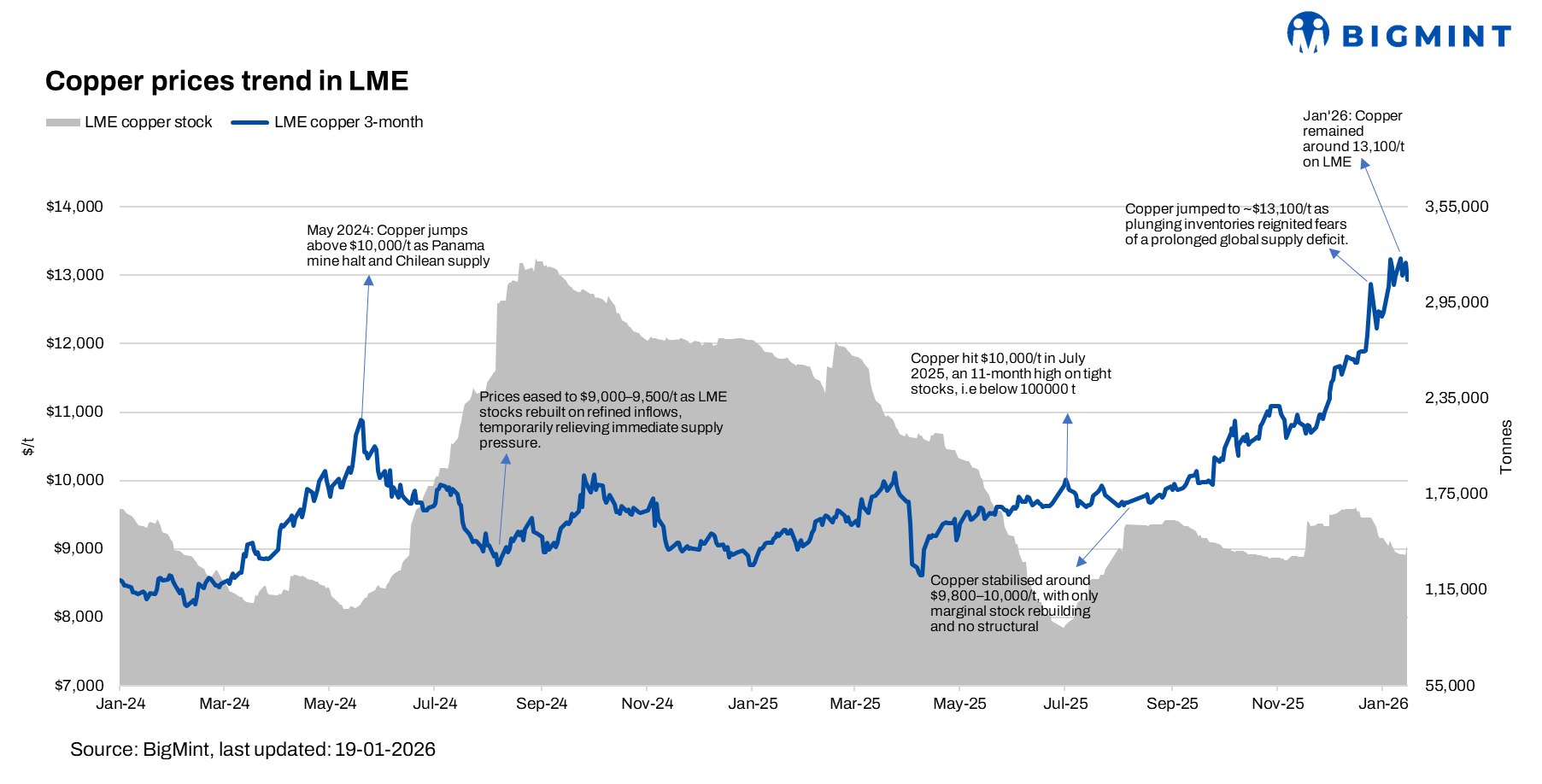

Copper prices continued to trade near record highs in January 2026, underlining the tightness in the global copper market. Prices touched $12,900 per tonne on 9 January 2026 and eased only marginally to around $12,800 per tonne on 16 January, showing limited downside correction despite daily volatility.

The key support for prices remains extremely low visible inventories. LME copper stocks are hovering around 140,000 tonnes, one of the lowest levels seen in recent years. This represents barely three days of global copper consumption, leaving the market with very little cushion. In such conditions, even small supply disruptions, shipment delays, or sudden buying interest can trigger sharp price movements.

Demand continues to be strong, driven mainly by electrification-related sectors. Global refined copper demand is expected to grow by around 3% in 2026, supported by investments in power transmission, renewable energy, electric vehicles, and data centres. These sectors consume copper steadily and are less sensitive to short-term price changes, keeping demand firm even at elevated price levels.

On the supply side, growth remains slow. Global mine output is projected to rise by less than 2% in 2026, as new projects take years to come online and several existing mines face operational challenges. Although additional smelting capacity has been added globally over the past two years, limited availability of copper concentrate continues to restrict refined copper production. This has kept treatment and refining charges (TC/RCs) near zero or in negative territory, a clear signal of upstream tightness.

The narrow price movement between 9 and 16 January suggests that the market is now accepting higher price levels as the new normal, rather than viewing them as temporary spikes. Financial participation has further amplified this trend, with copper increasingly seen as a strategic metal linked to the global energy transition.

Looking ahead, market participants are expected to plan for continued volatility. Staggered purchasing, selective hedging, diversified sourcing, and contractual price pass-throughs are likely to remain key strategies as copper prices stay sensitive to even minor changes in supply or sentiment.

Leave a Reply