- Speculative buying triggers price rise

- China and global investors fueled the rally

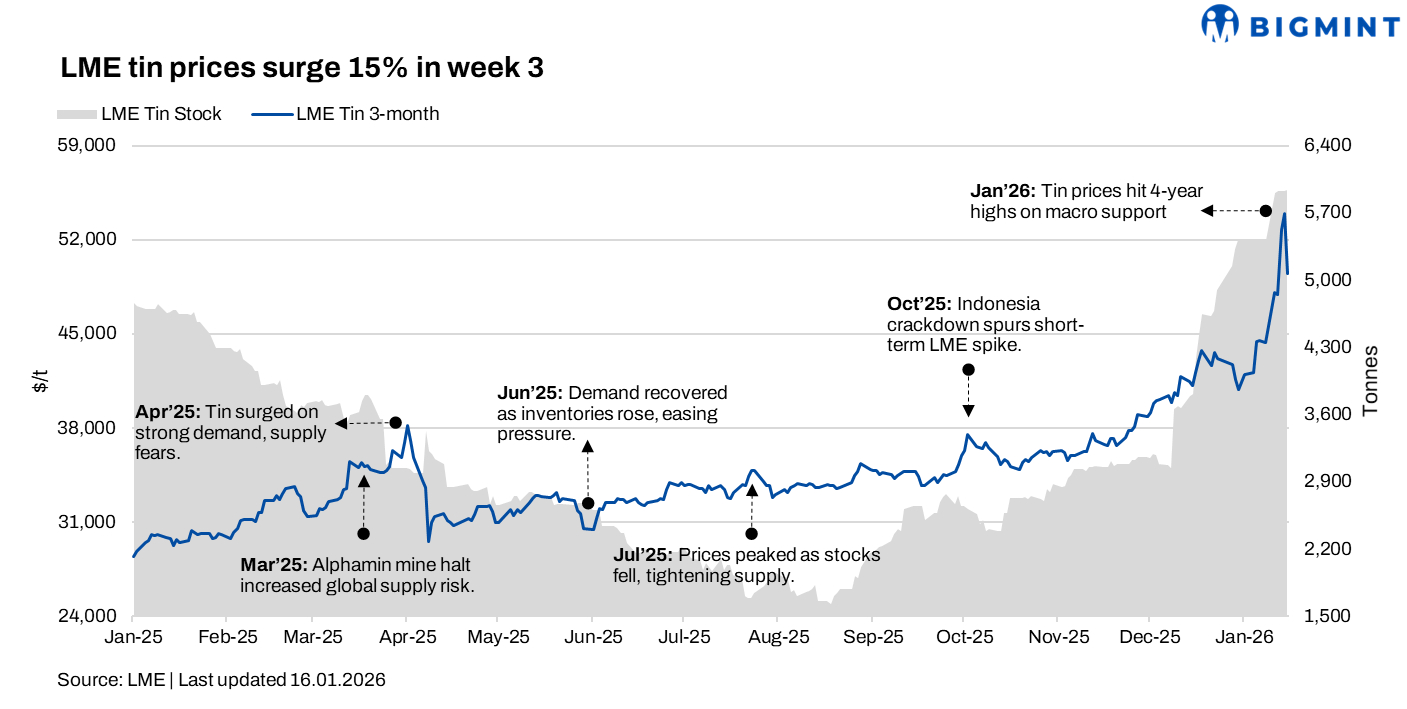

Tin prices on the London Metal Exchange (LME) surged in the week ended 16 January 2026 (week 3), driven by strong speculative buying from Chinese and global investors. Despite improving physical supply and rising inventories, market sentiment was fuelled by perceived supply tightness and tin’s strategic role in electronics, pushing prices to record highs.

Pricing, inventory trends

LME tin prices averaged $50,454/tonne (t) in the week ended 16 January, marking an $6,470/t or 15% rise w-o-w from the previous week. The week began with prices at $48,100/t, which inched up to around $53,970/t mid-week and then closed at $49,500/t.

Meanwhile, tin inventories at LME-registered warehouses rose 9% to 5,925 t from 5,412 t in the previous week.

Factors impacting prices

LME tin prices rose sharply w-o-w, driven primarily by an influx of speculative buying rather than a sudden deterioration in physical fundamentals. Strong investor interest, particularly from China, spilled over into the London market as prices surged to record nominal highs on both the LME and the Shanghai Futures Exchange (SHFE). Elevated trading volumes in Shanghai–far exceeding global physical consumption–highlighted the scale of speculative participation and reinforced bullish momentum across exchanges.

Market sentiment has been anchored to a long-standing narrative of structural supply constraints, given tin’s concentrated mine production base and reliance on geopolitically sensitive regions such as Myanmar and the Democratic Republic of Congo. This perception, coupled with tin’s growing strategic importance in electronics and semiconductor soldering, attracted fund flows seeking exposure to critical industrial metals.

However, the price rally has unfolded despite signs of improving supply conditions. Production risks in Congo have eased, Myanmar exports have rebounded, and Indonesia is expected to raise official output quotas in 2026. Refined tin availability has also improved, with combined LME and SHFE inventories rising notably in recent months.

Nevertheless, the relatively small size of the tin market amplified the price impact of speculative inflows. Rising fund long positions on the LME added liquidity but also heightened volatility, allowing momentum-driven buying to overpower near-term supply-demand realities and push prices higher w-o-w.

Outlook

Tin prices are likely to remain volatile in the near term, supported by ongoing speculative interest and tin’s strategic demand in electronics. While physical supply is improving and inventories are rising, small market size and elevated fund positions could sustain price swings, keeping both upside and downside risks significant.

Leave a Reply