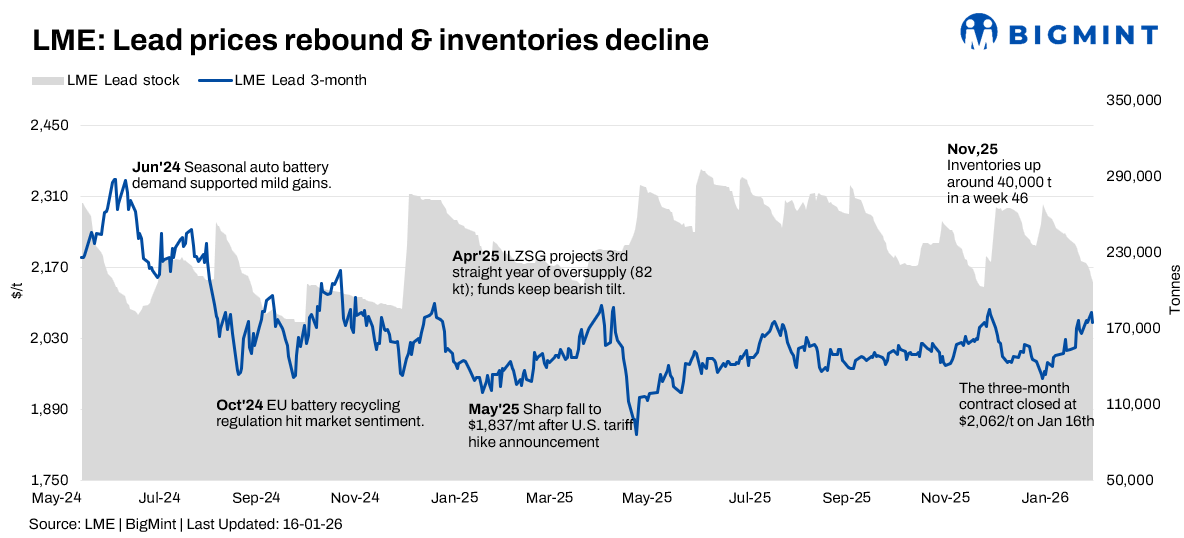

- LME lead inventories decline by 6.82% w-o-w

- Cash and 3-month contracts track similar weekly pattern

The London Metal Exchange (LME) lead market continued its recovery over 12–16 January 2026, building on early-year gains. Prices advanced steadily amid short-covering and improved sentiment, though high exchange inventories remained a persistent ceiling on the rally’s scope.

Price trends

LME lead cash prices opened at $2,020/t on 12 January and moved in a narrow range early in the week, dipping to $2,018.5/t on 13 January before strengthening to a weekly high of $2,040/t on 15 January. Prices later eased, closing at $2,017/t on 16 January, marginally lower by around 0.15% w-o-w. The three-month contract followed a similar trajectory, rising from $2,065/t on 12 January to a mid-week peak of $2,082/t, before settling at $2,062/t by 16 January, down slightly by about 0.15% w-o-w, but continuing to trade above the $2,050/t support level.

Inventory analysis

LME lead inventories declined sharply over the week, falling from 221,450 t on 12 January to 206,350 t by 16 January, marking a weekly drop of 6.82% (15,100 t). The consistent drawdown reflected steady warrant cancellations and improved physical offtake. However, despite the notable decline, total stocks remain elevated above historical norms, indicating that broader oversupply concerns persist. Market participants continue to monitor Chinese inventory movements closely, as smelter maintenance and seasonal factors keep regional availability relatively tight.

MCX lead trends (12-16 Jan)

On the MCX, near-month lead futures (31 January 2026) showed mixed movement but ended the week up around 1% w-o-w, settling at INR 191,400/t on 16 January compared with INR 193,150/t earlier in the week. Open interest remained broadly stable, suggesting sustained market participation, although marginal profit-booking was observed toward Friday.

Indian lead prices broadly tracked global cues but remained sensitive to local demand conditions and rupee movements, with physical buying staying cautious amid elevated cost structures.

SHFE lead trend

On the SHFE, the February 2026 contract (2602) traded at around CNY 17,400/t, up 0.8% w-o-w. Domestic battery restocking provided support, offsetting a largely neutral SHFE-LME arbitrage environment. Smelter maintenance continued to limit near-term supply, lending modest firmness to prices.

Ola Electric gets govt nod for India-made Shakti home battery

Ola Electric has secured government certification for its India-manufactured Shakti home battery, marking a key milestone in its energy storage ambitions. The approval validates compliance with domestic safety and performance standards, enabling wider commercial rollout. The Shakti battery is positioned to support residential energy needs, including rooftop solar integration and backup power. The development aligns with India’s push for local manufacturing and strengthens Ola Electric’s presence beyond electric vehicles into stationary energy solutions.

Spanish battery maker Endurance Motive wins 10 MW BESS orders

Endurance Motive SA has secured contracts worth 5.71 million Euro to supply and integrate 10 MW/50 MWh of battery energy storage systems in Spain. The projects, linked to solar plants, are scheduled for equipment delivery in May–June 2026, with commissioning expected in July.

Outlook

In the near term, LME lead prices are expected to trade range-bound, supported by inventory drawdowns, seasonal restocking and short-covering, but constrained by still-elevated exchange stocks and cautious downstream demand. The $2,050-2,100/t range is likely to remain critical for three-month contracts. Any sustained upside will depend on further visible inventory declines, firmer battery demand signals, and clarity on Chinese supply-side dynamics. On the domestic front, Indian prices may continue to follow global trends, with currency movements and physical demand conditions remaining key swing factors.

Leave a Reply