- Japan aluminium premiums surge 127%

- Near-term outlook remains firm amid tight supply

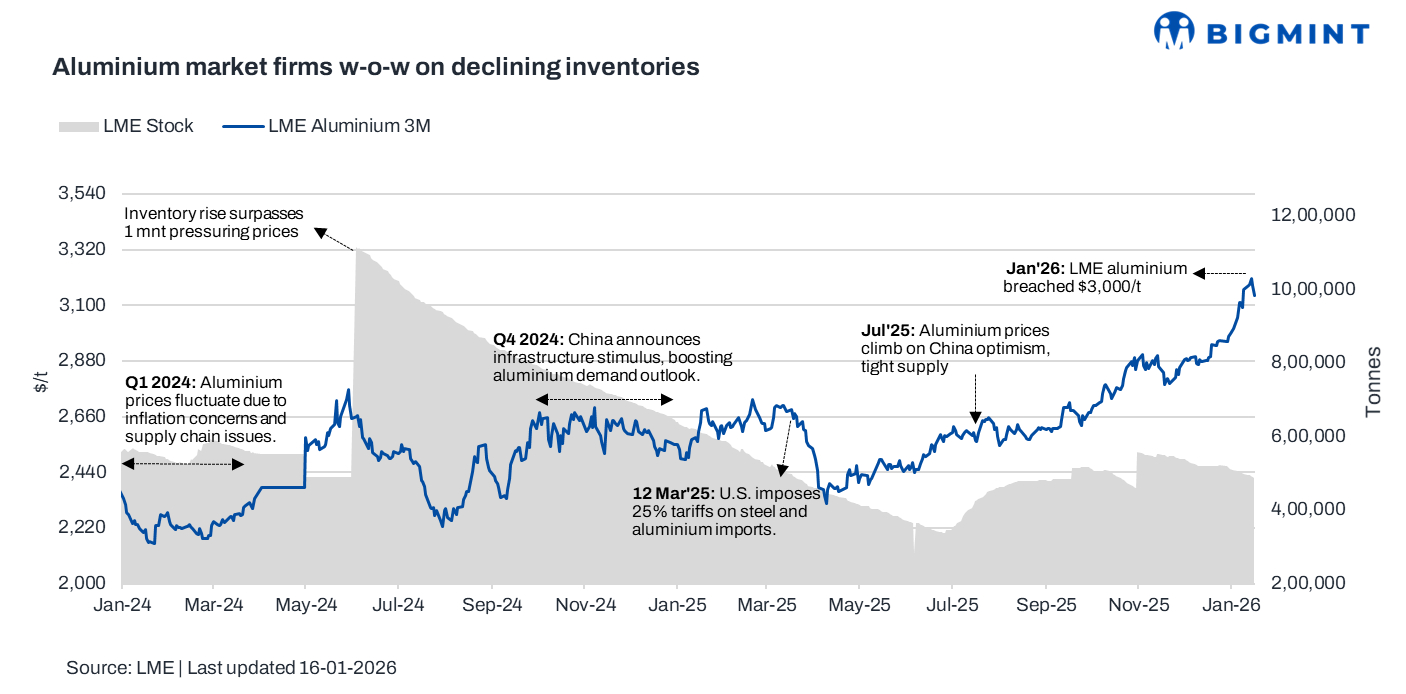

Benchmark aluminium prices on the London Metal Exchange (LME) rose by 2.3% over the week ended 16 January 2026, supported by tightening supply dynamics, China’s capacity curbs and reduced exports, along with indications of regional inventory tightness that lifted market sentiment.

Pricing, inventory trends

LME aluminium prices averaged $3,176/t in the week ended 16 January, up $70/t or 2.3% w-o-w. Prices opened the week at around $3,177/t and strengthened mid-week, reaching $3,205/t, and closed the week at $3,138/t.

Meanwhile, LME aluminium inventories dropped 2%, settling at 491,965 t w-o-w from 502,065 t in week 2.

Factors impacting prices

Aluminium prices rose w-o-w as supply-side tightness outweighed mixed demand signals. Market sentiment was underpinned by China’s strict enforcement of its 45-mnt smelting capacity cap, which constrained incremental supply even as domestic consumption showed signs of improvement. A sharp y-o-y decline in Chinese exports further tightened global availability, while delays and rising costs in overseas capacity additions–particularly in Indonesia–added to supply-side concerns.

Reflecting these conditions, the premium for aluminium shipments to Japan for January-March 2026 was set at $195/t, up 127% q-o-q and marking the first quarterly increase in a year. The sharp rise reflects tight global supply, production disruptions, and higher overseas premiums, according to market participants involved in the negotiations. Aluminium premiums in Japan are expected to remain elevated in Q2CY’26, supported by ongoing smelter outages, tight global inventories, and firm LME prices. While domestic demand remains moderate, sustained overseas market pressures are likely to keep premiums supported, with upcoming negotiations closely watched by both buyers and producers.

Outlook

Aluminium prices are expected to remain firm in the near term, supported by tight global supply, China’s capacity restrictions, and low inventories. While demand signals remain mixed, elevated regional premiums and limited supply additions could sustain price strength, with volatility driven by inventory movements and macroeconomic developments.

Leave a Reply