- Tier-1 mills raise rebar list prices by up to INR 2,500/t

- HRC prices show mixed trends amid festive trade lull

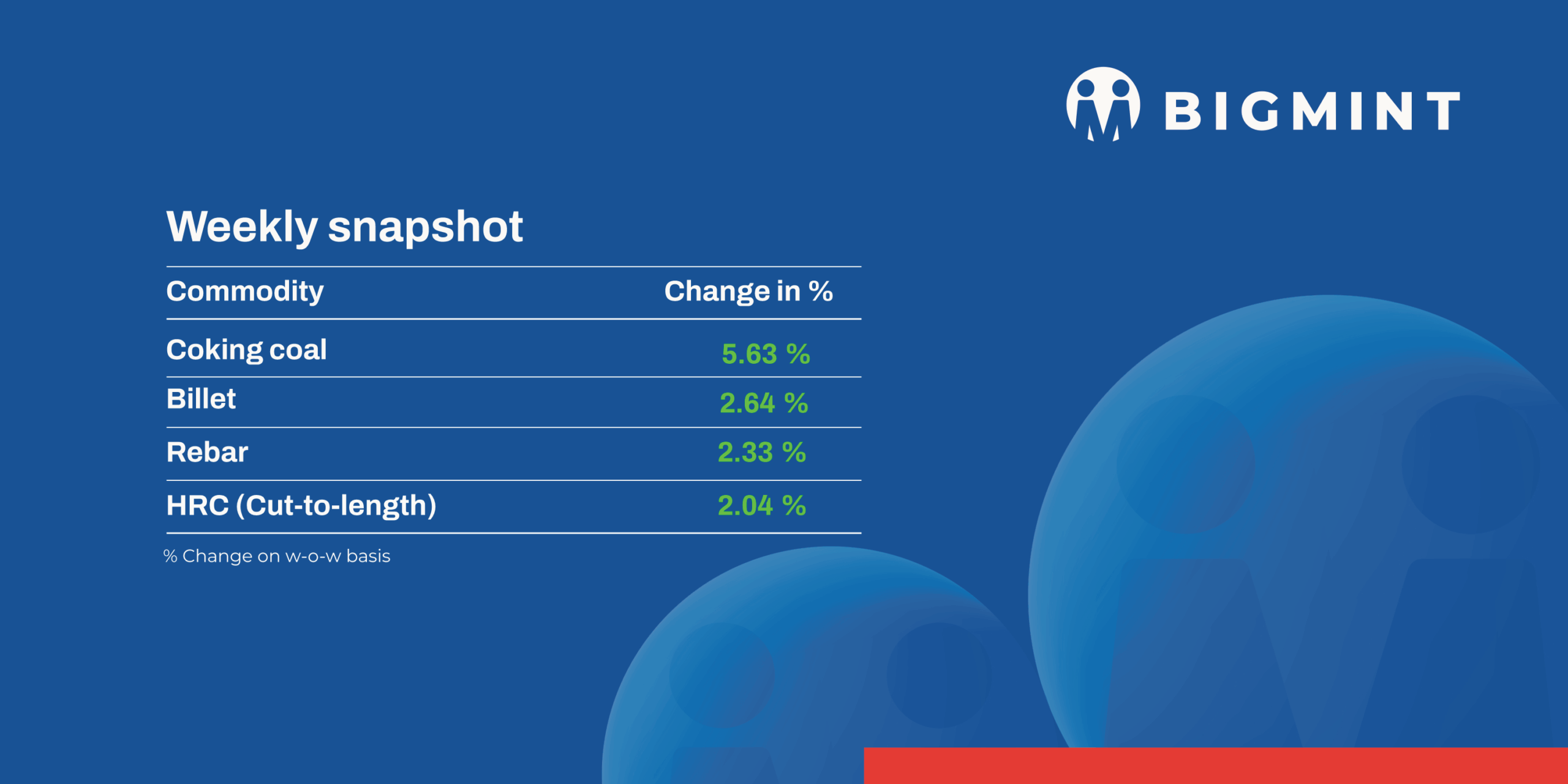

Domestic steel prices saw a positive trend during week 3 of CY’26 (12-16 January 2026) as demand picked up in key segments. Semi-finished steel prices increased by INR 500-2,200/tonne (t), while in the finished steel segment, IF-rebar prices increased by INR 700-2,700/t, and Indian tier-1 mills also increased rebar prices by up to INR 2,500/t. However, hot-rolled coil (HRC) prices showed mixed momentum as demand remained patchy.

Iron ore, pellet

- OMC will auction 3.6 mnt of iron ore (1.414-mnt lumps and 2.2-mnt fines) on 19 January. The miner has increased the base prices of lumps by around INR 800/t, while those of fines rose by INR 150-350/t m-o-m. The recent increase in pellet, sponge iron, and steel prices prompted an increase in base prices.

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, rose by INR 100/t w-o-w to INR 9,800/t ($108/t) DAP. Raipur-based pellet producers raised offers for Fe 62.5-63% (+/-0.5) grade pellets by INR 100-200/t ($1-2/t) to INR 9,600-9,700/t ($106-107/t) exw. The upward revision follows NMDC’s price increase for January iron ore sales. Deals were moderate as buyers booked material for immediate needs only.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices decreased by $2/tonne (t) w-o-w to $67/t FOB east coast on Thursday. Meanwhile, the index stood at $77/t CFR China. A few lower-grade cargoes were heard concluded this week, but deals are yet to be confirmed by the parties concerned. BigMint recorded around 80,000 t of iron ore export deals in this publishing window.

Coal

- Indian portside South African thermal coal prices touched a one-year high, supported by low port inventories, constrained export availability and firmer global benchmarks, although trading remained thin amid holidays and cautious buying. Exw Paradip 5,500 NAR rose INR 100/t w-o-w to INR 9,150/t, while Vizag increased INR 50/t to INR 9,000/t. For 4,800 NAR, Paradip climbed up by INR 200/t to INR 7,800/t and Vizag edged up to INR 7,600/t. Offers at Mangalore stayed elevated at INR 9,200-9,300/t for 5,500 NAR, with no trades reported.

- Domestic non-coking coal prices stayed unchanged w-o-w, with 5,000 GCV assessed at INR 5,750/t and 4,500 GCV at INR 4,800/t. Recent SECL auctions saw largely flat bidding, with most volumes clearing near floor prices, pointing to comfortable supply conditions.

- BigMint’s premium hard coking coal (PHCC) index increased $9/t w-o-w to $247/t CNF Paradip on 16 January 2026, reflecting tighter global supply, though confirmed bookings were absent. Australian PHCC prices rose by nearly $15/t since early January to $230-235/t FOB, driven by mining disruptions and force majeure declarations following heavy rainfall from Cyclone Koji. Higher coking coal costs also fuelled expectations of met coke price hikes in China of RMB 50-55/t.

- India’s BF-grade metallurgical coke prices were mostly steady w-o-w in mid-January, with subdued market activity. In eastern India, prices edged up by INR 100/t to INR 32,300/t ex-Jajpur on firmer raw material sentiment, while western India prices remained flat at INR 30,100/t ex-Gandhidham.

Ferrous scrap

- India’s imported ferrous scrap market remained subdued through the week, as a marginal improvement in steel demand failed to trigger fresh buying amid largely unworkable offer levels. Buyers stayed cautious and highly price-sensitive, supported by ample availability of cheaper domestic sponge iron and sufficient HMS and super scrap inventories.

- UK/EU-origin shredded was offered at $355-358/t CFR, while HMS 80:20 hovered near $330/t CFR with limited interest. Australian HMS at $325-330/t CFR and shredded at $345-350/t CFR also drew muted buying.

- Overall, around 3,000-3,500 t of imported scrap arrivals were heard, dominated by HMS 80:20, along with limited NTP, as buyers restricted purchases to strictly workable levels.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices edged up by INR 200/t ($2/t) w-o-w to INR 70,700-71,700/t ($784-791/t) across Durgapur, Raipur, Vizag, and Raigarh. Prices were supported by rising imported manganese ore costs, limited availability as key smelters are booked till mid-March, and the absence of discounted offers.

- Ferro manganese: Indian high-carbon ferro manganese (70%) prices remained largely range-bound w-o-w. Prices in Durgapur rose by INR 200/t ($2/t) to INR 71,900/t exw, while Raipur prices slipped by INR 100/t ($1/t) to INR 71,900/t. Market stability was driven by a lack of bulk export inquiries, offset by rising manganese ore costs.

- Ferro silicon: Indian ferro silicon (70%) prices remained stable w-o-w, with minor regional variations, supported by steady trading at Bhutan’s January-announced levels. Prices were assessed at around INR 94,000/t ($1,042/t) exw-Guwahati, while Bhutan prices edged down by INR 100/t to INR 93,900/t ($1,040/t) exw. Around 2,500 t were traded across both regions within the INR 93,500-94,000/t ($1,036-1,042/t) exw range.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices rose by INR 900/t ($8/t) w-o-w to INR 106,500/t ($1,170/t) exw-Jajpur. Prices were supported by the limited availability of standard-grade material and a lack of prompt deliveries. Market participants also adopted a wait-and-watch approach ahead of OMC’s chrome ore auction.

Semi-finished steel

- India’s semi-finished steel market witnessed a sharp improvement during the week, as per BigMint’s assessment. Domestic billet prices across major markets increased by INR 500-2,200/t ($9-24/t) w-o-w, supported by stronger market sentiment. Improved demand for finished steel, price hikes by primary producers, and tighter raw material prices provided upward momentum. Trade activity remained moderate, while buying interest in the semi-finished segment stayed steady.

Metallics

- Meanwhile, the sponge iron market also witnessed firm support during the week. Prices across key producing regions rose by INR 800-1,100/t ($7-15/t) w-o-w, aided by a slight improvement in procurement activity across regions. Increased buyer enquiries further boosted market confidence. Overall, stronger demand fundamentals and supply-side constraints contributed to a positive weekly market sentiment.

Finished long steel

- IF-rebar: IF-route rebar trade prices increased w-o-w across major Indian markets, supported by moderately strong trading activity and improved mill order bookings. The price rise was further backed by higher raw material costs, particularly sponge iron and billets. However, trading activity slowed mid-week as markets in Gujarat, Tamil Nadu, and Hyderabad remained closed due to regional festivities, including Makar Sankranti and Pongal. As per the current scenario, prices are likely to remain supported in the near term.

- Rebar prices increased by INR 700-2,700/t w-o-w across regions, as per BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 44,400-44,800/t exw-Raipur and INR 49,400-50,000/t exw-Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 45,800-46,200/t exw-Raipur.

- Trade reference prices of wire rod stood at INR 44,200-45,000/t ex-Raipur.

- BF-rebar: Indian Tier-I mills have increased rebar prices by up to INR 2,500/tonne (t) ($28/t) for mid-January 2026 deliveries, sources informed BigMint. Post-revision, list prices stood at INR 54,000-55,000/t ($594-605/t) on landed basis. Following this, trade-level blast furnace (BF) rebar prices (distributor to dealer) rose w-o-w across major Indian markets. The distribution channel experienced limited material availability in some sizes, highlighted market participants.

- Trade-level BF-rebar (distributor to dealer) prices rose w-o-w by INR 1,300/t ($14/t) to INR 53,800/t ($592/t) exy-Mumbai as per BigMint’s assessment on 16 January 2026. Prices are excluding GST at 18%.

- In the projects segment, prices hovered at around INR 53,500-55,000/t ($589-605/t) FOR Mumbai basis.

Flat steel

-

- Trade-level prices of hot-rolled coils (HRCs) in India showed mixed trends w-o-w, ranging within INR 49,500-51,600/t ($549-572/t) in key regions. However, cold-rolled coil (CRC) prices increased w-o-w, ranging between INR 54,000-59,500 ($598-659/t).

- Domestic HRC prices firmed up in the west, while a decline was noted in the north this week due to mixed demand trends. In northern India, limited buying enquiries were received by distributors, who indicated that demand softness was partly attributable to festival holidays and an extended weekend, which dampened market activity. Sellers faced constrained liquidity and expressed increasing impatience regarding the slow offtake.

- India’s bulk imports of HRCs touched 68,901 t as of 12 January, based on vessel line-up data. Around 107,199 t of additional cargoes are expected by late-January. India’s bulk exports of HRCs touched 20,253 t as of 12 January.

- BigMint’s Indian HRC (S275) export index for the European Union (EU) declined by $15/t w-o-w to $505/t FOB main port from $520/t a week earlier. “Indian mills have fully exhausted their allocated quota for Q1CY’26. With the Carbon Border Adjustment Mechanism (CBAM) now in force, buyers are increasingly relying on mills’ declared emissions values, while the verification process has been initiated by most mills,” a BigMint source noted.

- However, the Indian HRC (SAE 1006) export index for the Middle East increased by $5-10/t to $470-475/t FOB main port from $465/t a week earlier. A BigMint source noted that “overall demand in the region remained steady, with market activity continuing at a moderate pace.

Leave a Reply