- Indonesian coal stays stable w-o-w on muted post-holiday buying

- Buyers remain cautious, limiting purchases to immediate needs

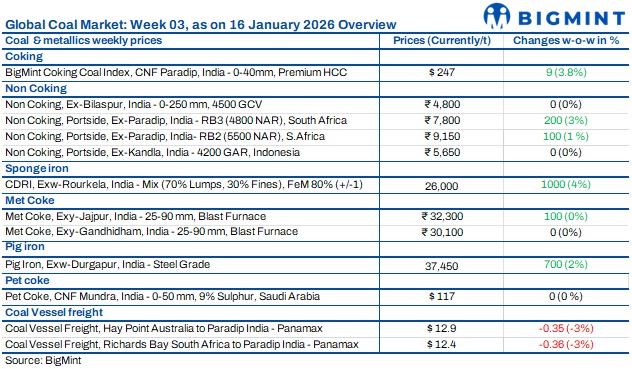

Indian coal market sentiment remained cautious and selective during the week ended 17 January 2026. Divergent price trends emerged: Portside South African non-coking coal prices firmed up on tightening export availability and global arbitrage signals, while Indonesian coal stayed stable due to muted domestic buying and holiday disruptions. Trade activity remained thin, with most buyers restricting procurement to immediate needs. Overall sentiment reflected availability-driven firmness rather than demand-led momentum, keeping negotiations active but deal closures limited across origins.

Indonesian thermal coal stays remains stable

Indonesian thermal coal prices at Indian ports remained largely stable through mid-January 2026, capped by weak buying interest and holiday disruptions. West coast 3,400 GAR softened slightly in early January before settling around INR 4,400-4,500/t on 16 January, with offers at INR 4,275-4,475/t. Buying remained strictly need-based amid subdued industrial activity. Meanwhile, 4,200 GAR prices eased and then found a floor, holding near INR 5,500-5,750/t, with offers around INR 5,500-5,650/t. Lower freight costs and comfortable availability limited downside but also prevented any meaningful upside, keeping Indonesian material stable. Indonesia’s ESDM revised HBA coal prices for late January 2026, with high- and low-CV grades firming on improving Asian demand, while mid-CV eased slightly amid cautious supply.

South African non-coking coal prices hit 1-year high

Indian portside South African thermal coal prices rose to a one-year high, supported by lower port stocks, tight export availability, and higher global indices, though trade activity remained thin due to holidays and cautious buying. In late December, 5,500 NAR traded around INR 8,700-9,000/t with limited activity. Prices stabilised near INR 8,900-9,100/t in early January, though trades stayed thin. On 16 January, offers firmed to INR 9,100-9,200/t, supported by FOB RBCT levels of $79-80/t and CFR India ideas near $94/t amid cargo diversion to South America. 4,800 NAR tightened faster, rising from around INR 7,500-7,900/t in late December to INR 7,600-7,900/t, driven by limited portside availability rather than demand.

Domestic non-coking coal prices remain flat as auctions reflect cautious buying

Domestic non-coking coal prices remained stable w-o-w, with 5,000 GCV at INR 5,750/t and 4,500 GCV at INR 4,800/t. Recent SECL auctions witnessed largely flat bidding, with most volumes clearing close to floor prices, indicating adequate supply. Only select parcels, including Sonepur Bazari, attracted modest premiums, while overall participation stayed subdued as buyers continued need-based procurement amid comfortable availability.

Coking coal index jumps, further hike likely

BigMint’s premium hard coking coal (PHCC) index rose by $9/t w-o-w to $247/t CNF Paradip on 16 January 2026, reflecting tightening global supply, though no firm bookings were concluded. Australian PHCC prices climbed up by nearly $15/t since early January to $230-235/t FOB, driven by mining disruptions and force majeure declarations after heavy rainfall from Cyclone Koji. Rising coking coal costs prompted expectations of met coke offer hikes in China by RMB 50-55/t. In India, BF-grade met coke prices stayed supported, with eastern India prices edging up by INR 100/t to INR 32,300/t ex-Jajpur. Indian steel sentiment also firmed as primary mills raised rebar list prices by up to INR 2,500/t for mid-January deliveries, lending indirect support to the coking coal and met coke markets.

Met coke prices steady

India’s BF-grade metallurgical coke prices largely held steady w-o-w in mid-January, with market activity remaining muted amid cautious buying. In eastern India, prices edged up by INR 100/t to INR 32,300/t ex-Jajpur, supported by firmer raw material sentiment, while western India prices stayed unchanged at INR 30,100/t ex-Gandhidham. Trade volumes remained thin as buyers relied on existing inventories and deferred fresh commitments, partly due to Sankranti-related disruptions.

Australian premium hard coking coal prices surged by $10/t w-o-w to $228/t FOB following weather-related supply disruptions, lending cost support to coke prices, though the impact was expected to materialise only from late-February shipments. Chinese met coke prices remained stable, while Indian pig iron prices rose by INR 200/t to INR 36,700/t, supporting overall sentiment.

Indian steelmakers increasingly booked Indonesian met coke despite anti-dumping duties, as higher coking coal prices and tight availability of high-CSR domestic coke improved import viability. Landed Indonesian met coke costs remained competitive against rising domestic prices, encouraging imports amid Australian coking coal supply disruptions.

US coal prices jump

Indian portside prices of US-origin thermal coal rose sharply w-o-w, increasing by INR 500/t to INR 11,100/t, driven by supply tightness and steady demand from cement producers. Buyers turned to US coal as imported pet coke remained relatively expensive, improving coal’s cost competitiveness. Market participants indicated that limited domestic availability further tightened prompt supply, supporting the sharp price increase.

Sentiment was also influenced by geopolitical concerns, with expectations of potentially higher US tariffs creating uncertainty around future availability and trade flows. The combination of supply shortages, substitution demand from cement plants, and rising geopolitical risk kept prices firm during the week, despite otherwise cautious procurement behaviour across the broader fuel market.

Pet coke prices stay firm

Global pet coke markets moved through mid-January 2026 in a quiet but resilient phase, as tight supply and high freight costs kept prices supported despite weak spot demand. High-sulphur material remained range-bound, with US export prices largely unchanged and Turkish prices holding in the low-$100s/t. In India, bids stayed near the low-$110s/t CFR, while offers hovered close to $120/t, limiting trades.

Mid-sulphur grades showed selective strength, with 5.5% sulphur material trading at a premium, while US West Coast 4.5% sulphur edged higher on tight availability. Low-sulphur pet coke from the US West Coast stayed structurally tight and highly priced, retaining a strong premium. Seasonal supply discipline, elevated landed costs, and fuel substitution risks kept the market muted but supported, preventing any sharp downside.

Coal freights stay weak

Dry bulk coal freights into India remained under pressure during the week as weak demand and ample vessel availability dominated market sentiment. Limited fixing activity across Australia-India, South Africa-India and Indonesia-India routes kept rates soft, while charterers adopted a cautious, wait-and-watch approach amid comfortable coal inventories and subdued steel sector demand.

Rising bunker prices lifted voyage costs but failed to support rates, squeezing shipowners’ margins further. Softer FFAs and a Baltic index at a six-month low reinforced bearish sentiment. Panamax freights from Australia to India declined by $0.35/dmt w-o-w to $12.9/dmt, while South Africa-India rates fell by $0.36/dmt to $12.4/dmt. Indonesia-India Supramax freights eased by $0.21/dmt to $10.8/dmt. Overall, freights stayed weak.

Leave a Reply