- Buyer resistance capped spot activity despite firm global pet coke prices

- Supply discipline and freight costs underpinned prices across grades

Global petroleum coke markets moved through mid-January 2026 in a quiet but resilient phase. While buyers across key importing regions showed increasing resistance to high landed costs, prices across most sulfur grades and geographies remained firm. Tight supply, seasonal availability constraints, and elevated freight costs continued to underpin values, preventing any meaningful downside correction despite low spot activity.

Price Snapshot: Sulfur Grade-Wise and Geography-Wise

All prices in US$/t; early-mid January 2026

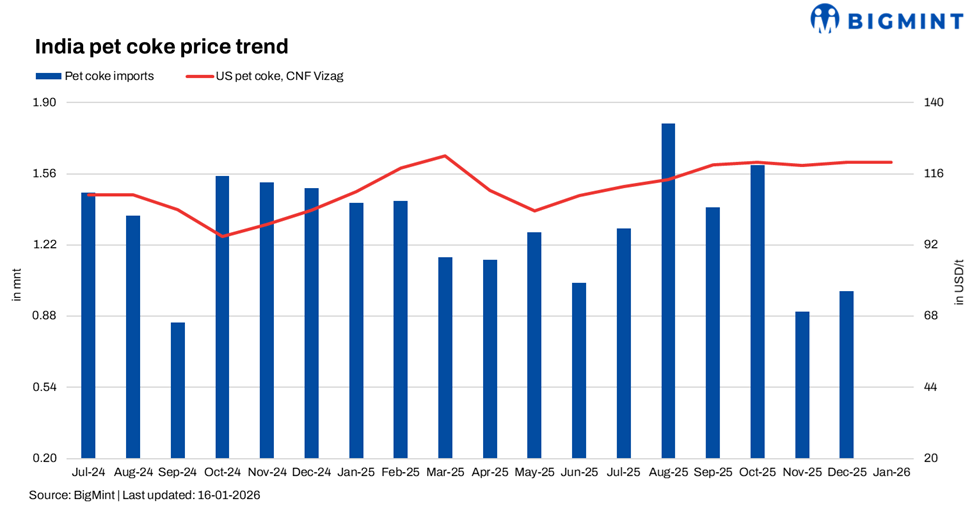

India range reflects buyer bids, indicative levels, and seller offers; practical buying interest is concentrated in the $112-116/mt CFR band.

Market Performance Across Sulfur Grades

High-Sulfur (6.5% Sulfur): Rangebound and Cautious

High-sulfur pet coke remained firm but capped across markets. US export prices were largely unchanged, reflecting muted spot demand balanced by limited prompt availability. In Turkey, delivered prices held in the low-$100s/mt, with both bids and offers visible, indicating a relatively balanced but thin market.

In India, buyer resistance was more pronounced. Bid ideas clustered near the low-$110s CFR, while offers remained closer to $120/mt, resulting in a wide bid-offer spread and few spot transactions. Buyers largely adopted a wait-and-watch approach, covering only immediate requirements.

Mid-Sulfur (5.5-4.5% Sulfur): Selective Strength

Mid-sulfur grades displayed slightly firmer undertones. Turkey continued to show a preference for 5.5% sulfur material, which consistently traded at a premium to high-sulfur grades due to cement sector requirements. US Gulf Coast mid-sulfur prices were stable, while US West Coast

4.5% sulfur values edged higher, supported by tighter regional supply and limited spot cargo availability.

Low-Sulfur (≤2% Sulfur): Structurally Tight

Low-sulfur pet coke from the US West Coast remained structurally tight and highly priced. Limited production volumes and niche industrial demand insulated this segment from broader market weakness, allowing prices to retain a significant premium over higher-sulfur grades.

Structural Forces Shaping the Market

Seasonal Supply Discipline

Producers entered the year with reduced spot exposure following year-end inventory drawdowns. This seasonal tightening limited availability across sulfur grades, particularly for low- and mid-sulfur material, restricting sellers’ ability to chase volumes through discounts.

Landed Cost Pressure and Buyer Pushback

Elevated freight rates continued to inflate delivered prices into India and Turkey, magnifying buyer resistance even where FOB prices remained stable. In India, buyers consistently indicated workable economics in the mid-$110s CFR, with limited willingness to transact above that level.

Fuel Substitution Risk

High-sulfur pet coke faced growing competition from thermal coal, especially in price-sensitive cement markets. This substitution risk capped upside potential for 6.5% sulfur material, reinforcing the current rangebound structure.

Near-Term Market Direction

High-sulfur pet coke is expected to remain sideways, supported by supply discipline but constrained by buyer resistance. Mid-sulfur grades are likely to retain a modest premium, particularly in markets with tighter availability. Low-sulfur pet coke should continue to trade firmly, underpinned by structural scarcity.

Overall, the pet coke market is set to remain muted but but with a floor under prices, characterised by cautious buyers, low spot volumes, and supply discipline rather than demand-led price momentum.

Leave a Reply