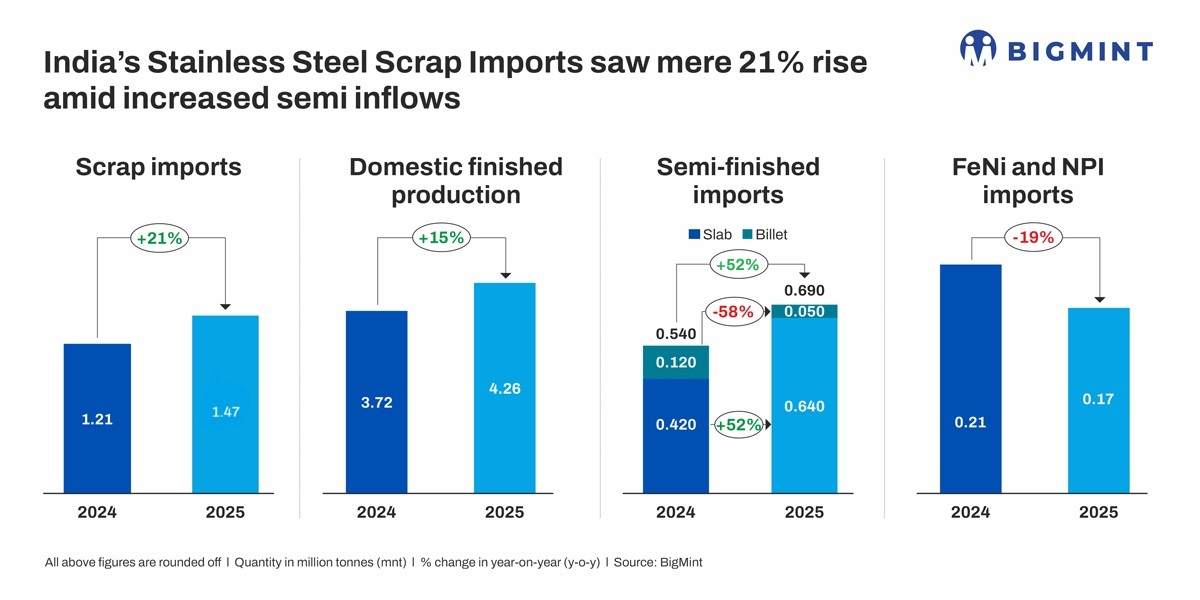

- SS scrap imports reach 1.47 mnt in CY’25

- Domestic stainless steel production rises 14% in CY’25

India’s imports of stainless steel scrap rose by 21% y-o-y in calendar year 2025 (January-December), with total shipments recorded at 1.47 million tonnes (mnt) as compared to 1.21 mnt in CY’24, as per BigMint data.

This rise in scrap imports coincided with a decline in arrivals of semi-finished products like slabs and billets, prompting greater use of scrap to support production. Notably, Indonesia, a key supplier, saw its exports of semi-finished products and ferro nickel to India decline during this period.

Series & grade-wise imports

Imports were led by 300-series, with total volumes rising by 28% y-o-y to 1.04 mnt, while imports of 200-series stainless steel scrap rose by 2% to 0.13 mnt. Imports of 400-series dropped slightly 1% to 0.18 mnt.

Among the mainstream grades, 304 scrap imports surged by 36% to 0.57 mnt, 316 grade increased by 27% to 0.14 mnt, and Zurik by 16% to 0.29 mnt. 430 grade imports were dropped by 7% to 0.12 mnt in the year, and other grades were dropped by 57%, reflecting broad-based demand.

Country-wise imports

The US remained the top supplier with 0.20 mnt up by 4% y-o-y from 0.19 mnt, while Vietnam shipments increased to 0.11 mnt by 10%. Thailand imports slightly dropped to 0.11 mnt by 1% y-o-y. Meanwhile Turkiye’s scrap imports recorded at 81,000 t in 2025 up 189% from 28,000 t, followed by UAE shipments were reported at 51,000 t up from 127% from 28,000 t in the year 2025. Significant volumes also came from Malaysia, Saudi Arabia, Germany, and the UK, as buyers diversified sourcing.

Factors driving imports

Increased domestic production: India’s finished stainless steel flat output rose 14% y-o-y to 2.95 mnt in CY’25 from 2.59 mnt. Higher capacity utilisation, expanding cold-rolling facilities, and better cost control enabled Indian mills to replace imported material, particularly in the 300-series.

Rupee weakens: The Indian rupee depreciated by around 4.7% in 2025, adding to imported cost pressures across the stainless steel value chain. The weaker currency raised the landed cost of key raw materials such as nickel, ferro alloys, and stainless steel flats, reducing the price advantage of imports. This also made overseas purchases riskier amid volatile freight and metal prices, further encouraging mills and traders to rely more on domestic supply.

Semi’s imports: Stainless steel billet imports into India were recorded at 46,000 t in CY’25, down 64% y-o-y compared to 129,000 t in CY’24. Indonesia remained the largest supplier, however, shipments from the country dropped significantly to 60,000 t compared to 128,000 t in 2024.

Ferro nickel & NPI imports: Ferro nickel imports were dropped to 0.17 mnt down by 16% from last year’s 0.20 mnt in 2024, with Indonesia remained the top supplier at 0.11 mnt, drop by 45% from 0.20 mnt last year. NPI shipments to India were recorded at 0.13 mnt in 2025.

Competitive domestic prices: From May 2025 onwards imported scrap prices were remained more higher than domestic prices, so mills were more inclined towards domestic scrap. During the end year Nov-Dec India’s stainless steel scrap market remained subdued with limited buying activity with mills were holded sufficient inventories and refraining from fresh bookings.

During September, 300-series scrap prices firmed up, supported by rising alloy prices, particularly ferro molybdenum, which traded at elevated levels during the period. Prices also gained strength in line with a broader uptrend in global markets, led by China. Additionally, an increase in oxide prices further lifted cost-side pressure, contributing to the upward movement in scrap values.

Outlook

India’s stainless steel scrap imports are expected to rise in the near term, driven by robust domestic production growth and continued broad-based demand across grades. With Indian mills expanding capacity and seeking cost efficiencies, the momentum in the scrap import market is set to persist in the months ahead.

Leave a Reply