- Heavy rainfall, logistics disruptions prompt 18% drop in Australian exports

- Weak demand from India, China contributes to sharp Indonesian pullback

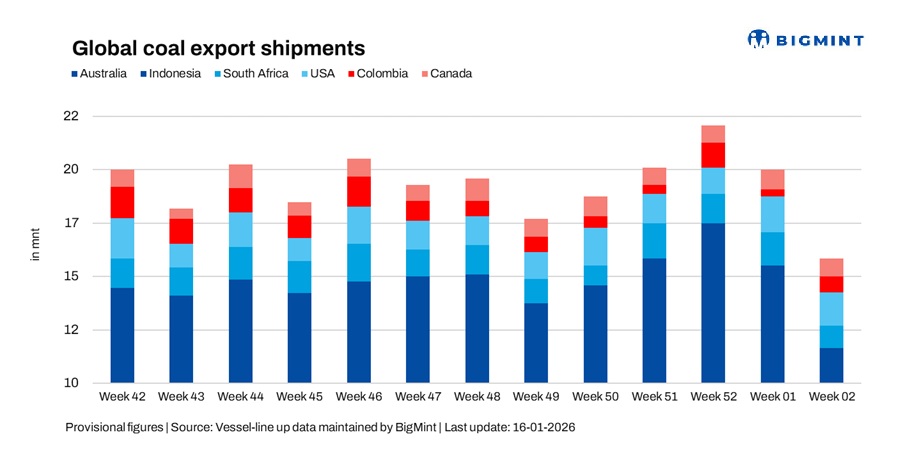

Global seaborne coal exports declined sharply by 20.8% w-o-w to 15.51 million tonnes (mnt) in week 02 of 2026 (03-09 January) from 19.59 mnt in week 01 (27 December-02 January), according to BigMint’s vessel line-up data. The decline reflected a deepening post-holiday slowdown, with steep reductions in shipments from Australia, Indonesia, and South Africa outweighing a rebound from Colombia. Volumes stood at their lowest since BigMint began tracking weekly coal export shipments in June 2025.

The week 02 performance marked a continuation of the soft start to CY’26, as early-January demand remained subdued and freight market conditions offered little incentive for exporters to accelerate loadings. With fresh cargo enquiries limited, chartering activity cautious, and freight sentiment weak, exporters prioritised controlled shipment programmes over volume expansion. While port operations across major origins remained largely stable, the absence of demand-side urgency reinforced the sharp weekly decline in global coal exports.

Country-wise trends

Australian coal shipments plunge

Australia’s coal exports declined 17.5% w-o-w to 6.4 mnt in week 02 from 7.7 mnt in week 01, extending the post-year-end correction. The decline reflected reduced cargo stem issuance and limited buying interest from key Asian markets, as comfortable inventories and weak downstream margins continued to curb procurement appetite.

Export momentum was further weighed by logistical headwinds, as heavy rainfall and climate-driven volatility intermittently disrupted rail and port operations across key Queensland corridors, constraining coal movements despite broadly stable terminal capacity. Shipment activity was led by Newcastle (2.78 mnt), followed by Gladstone (1.54 mnt) and Abbot Point (0.65 mnt). Glencore led shipments at 0.72 mnt, followed by BHP at 0.51 mnt, underscoring the supply-managed export environment.

On the demand front, Japan remained the largest destination at 2.18 mnt, followed by China at 0.97 mnt and South Korea at 0.88 mnt. Overall, the week 02 slowdown underscored the unwinding of aggressive December dispatches, keeping Australian coal exports firmly demand-led, while rising climate-related logistics risks continue to pose a structural challenge to export reliability.

Indonesian shipments see sharp pullback

Indonesia’s coal exports declined 31.8% w-o-w to 5.2 mnt in week 02, from 7.6 mnt in the previous week, marking one of the sharpest weekly pullbacks among major exporters. The decline followed the clearance of deferred December cargoes, with shipment flows normalising sharply as spot demand from India and China remained weak. The slowdown also comes against the backdrop of Indonesia signalling a coal output cut in 2026, as authorities seek to rebalance the market amid softer exports and easing prices, adding a layer of policy-driven caution to current export strategies.

Export activity was concentrated at key loading hubs, led by Taboneo at 1.23 mnt, followed by Balikpapan at 0.62 mnt and Samarinda at 0.40 mnt, reflecting moderated but steady operational throughput. On the demand side, China emerged as the largest destination at 1.29 mnt, followed by India at 0.73 mnt and Vietnam at 0.55 mnt, though overall buying interest remained selective.

Despite stable operations, exporters had limited incentive to push volumes amid weak freight economics and cautious buying. Logistical constraints and policy uncertainty around future production and exports further weighed on shipment momentum.

South African exports retreat after brief recovery

South Africa’s coal exports declined 32.4% w-o-w to 1.01 mnt in week 02 from 1.5 mnt in week 01, reversing the previous week’s modest recovery. The pullback reflected selective execution of scheduled cargoes rather than buying interest during the week.

Export activity remained concentrated at Richards Bay, which handled the complete 1.01 mnt of coal. On the demand side, India emerged as the leading destination with imports of 0.29 mnt, followed by Pakistan at 0.11 mnt, highlighting continued dependence on South Asian demand despite overall muted buying interest.

While terminal operations remained stable, demand stayed measured amid soft freight sentiment and subdued power sector import appetite. Limited follow-through demand continued to constrain export volumes, keeping South African coal shipments below potential despite available supply and operational readiness.

Colombia coal shipments jump on cargo execution

Colombia’s coal exports rose sharply by 120% w-o-w to 0.7 mnt in week 02 from 0.32 mnt in week 01, supported by the execution of previously scheduled cargoes following last week’s lull. The rebound was largely logistical in nature, reflecting shipment timing rather than an improvement in underlying demand conditions.

Export activity remained concentrated at a narrow set of terminals, led by Puerto Bolivar at 0.44 mnt and Puerto Nuevo at 0.22 mnt. On the supply side, Cerrejon Mines emerged as the leading shipper with 0.44 mnt, followed by Prodeco Group at 0.22 mnt, underscoring the shipment-specific nature of the week’s increase.

On the demand front, Turkiye was the largest destination at 0.16 mnt, followed closely by Mexico at 0.15 mnt. Despite the sharp w-o-w rebound, weak European demand and limited cargo redirection flexibility continued to cap a sustained recovery, indicating that the uptick did not signal a broader turnaround in Colombia’s export outlook.

US coal exports inch down

US coal exports edged lower by 7.4% w-o-w to 1.5 mnt in week 02 from 1.6 mnt in week 01. The week witnessed steady execution of planned cargoes rather than a broad-based decline in demand. Terminal operations remained consistent during the week, supported by stable logistics and scheduled loadings.

Export activity was led by Norfolk at 0.76 mnt, followed by New Orleans at 0.30 mnt and Baltimore at 0.25 mnt, indicating stable throughput across major US load ports. On the demand side, India remained the leading destination, with imports of 0.22 mnt, followed by Brazil at 0.14 mnt, though overall buying interest stayed selective.

While US exports showed relative resilience compared with other Atlantic suppliers, muted global import demand and ongoing trade headwinds continued to limit upside momentum. As a result, exporters maintained a broadly cautious outlook for US coal for CY’26.

Canadian shipments soften after recent highs

Canada’s coal exports declined 8.8% w-o-w to 0.8 mnt in week 02 from 0.9 mnt in the previous week, as shipments eased following recent multi-week highs. The pullback reflected slower cargo execution amid muted demand visibility from northeast Asia, even as west coast terminals maintained steady operations.

Export activity remained concentrated across key west coast ports, led by Roberts Bank at 0.43 mnt, followed by Vancouver at 0.24 mnt and Prince Rupert at 0.16 mnt. On the supply side, Elk Valley Resources emerged as the leading shipper with 0.24 mnt, underscoring the supply-led nature of exports during the week.

On the demand front, Japan remained the largest destination at 0.36 mnt, followed by South Korea at 0.16 mnt. Despite the weekly decline, exports continued to be supported by planned shipments; however, volumes still trailed available capacity, reinforcing the cautious export environment at the start of CY’26.

Coal freights remain weak, slowing shipments

Coal freight markets across major India-bound routes remained mixed during the week, as ongoing enquiries and selective fixing offered limited support but were insufficient to offset the impact of ample vessel availability and cautious early-year buying. Cargo urgency stayed low, with Indian importers largely covering near-term requirements rather than advancing shipment programmes. Comfortable tonnage supply across Australia, South Africa, and Indonesia continued to cap owners’ pricing power, keeping freights largely stable to weaker.

While Panamax segments saw selective, route-specific support, Supramax markets remained under pressure amid muted cargo volumes and an oversupply of prompt vessels. Falling bunker prices and softer FFAs further reinforced the bearish undertone, reducing owners’ resistance to rate concessions. As a result, subdued freight economics discouraged exporters from pushing additional long-haul shipments, reinforcing a demand-led and controlled shipment environment during the week.

Outlook

Global coal exports are expected to remain soft in the near term, with shipment momentum dependent on the pace of post-holiday demand recovery and the direction of freight markets. Australian and Indonesian volumes may stabilise if buying interest from India and China improves, while South African and US exports are likely to remain stable amid selective import demand. Atlantic suppliers remain vulnerable to weak European interest.

Freight markets are expected to stay under pressure in early January due to ample vessel availability and muted cargo enquiries. In the absence of a clear pick-up in downstream demand, any recovery in coal exports is expected to be gradual, keeping global coal trade cautious as CY’26 unfolds.

Leave a Reply