- Stocks at many mills decline by over 10% m-o-m

- Tight supply intensifies competition among mills

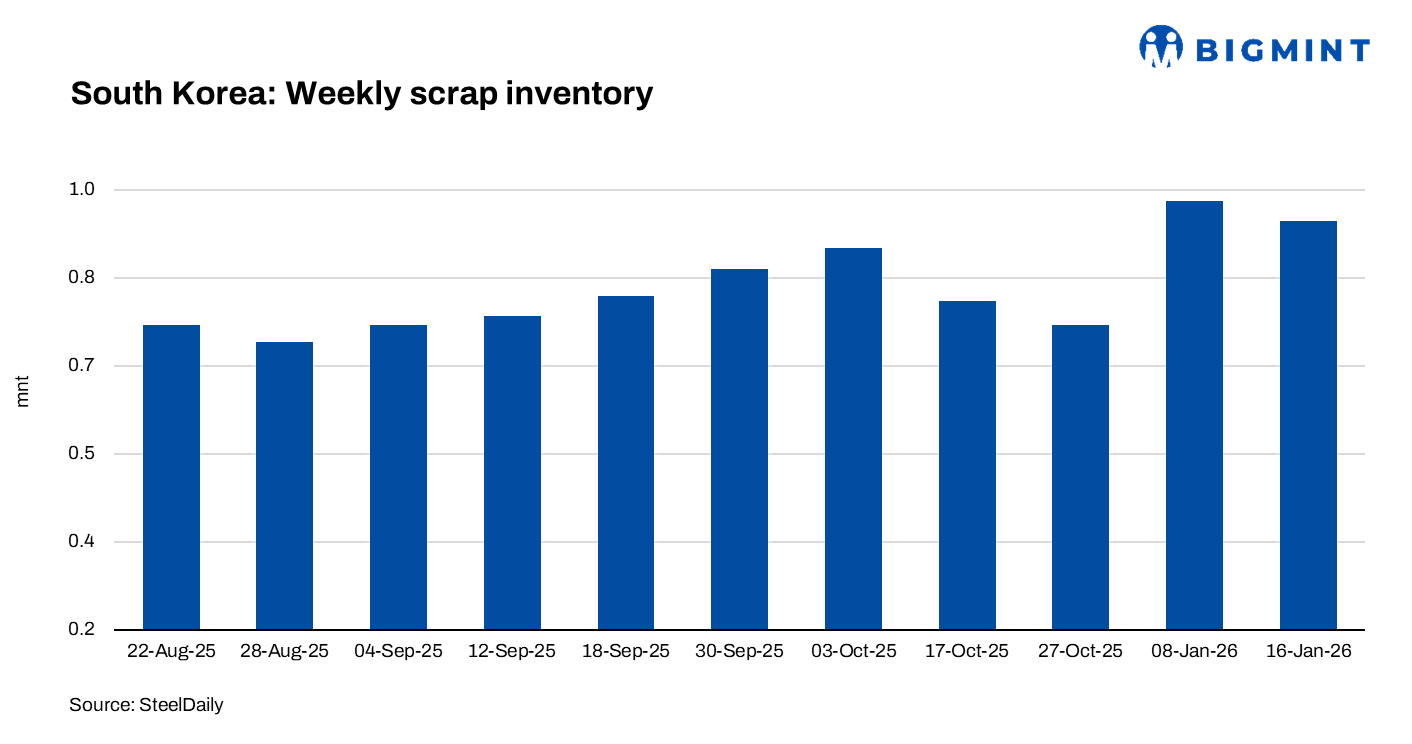

SteelDaily: The cumulative ferrous scrap inventory at eleven major South Korean steelmakers fell for the second time in the new year. Stocks declined by 32,000 tonnes (t) or 3.4% to 897,000 t on 14 January.

Region-wise inventory

Central region: Scrap inventories decreased by 10,000 (3%) in the central region, while Pohang remained relatively stable, posting only a 2,000-t (0.9 %) decline.

Southern region: In the southern region, the sharpest drop was recorded in Busan and South Gyeongsang Province, where inventories declined by 9,000 t, or 7.3%, to 115,000 t. Incheon followed with a 5,000-t (3.6 %) fall to 133,000 t.

By industry, inventories at steel manufacturers fell by 2.8 %, while sheet and special steel producers posted a sharper 4.6 % decline. Both segments shed around 16,000 t of scrap during the week.

Company-wise trends

On a company-wise basis, Hyundai Steel, YK Steel, and Hwanyoung Steel maintained inventory levels similar to the previous week. In contrast, Korea Iron and Steel, Daehan Steel, and Dongkuk Steel recorded relatively sharper declines in scrap stocks.

Comparing the second week of January with a month earlier, production fell by 39,000 t or 4.2%. Daehan Steel’s volumes rose 11.4%, while Hyundai Steel and Hwanyoung Steel increased around 8%. However, many mills saw stock declines of over 10% m-o-m, with some now nearly 30% below mid-December levels.

Daehan Steel, which recorded the largest inventory increase versus December, reportedly pursued an aggressive buying strategy from mid-December, targeting about 50,000 t of scrap. Hyundai Steel also continued maximising procurement despite production cuts and temporary shutdowns.

Market impact

Distributors expect a price uptick as steelmakers’ scrap inventories remain critically low, with several mills operating below optimal levels. Tight supply is intensifying competition, though weak finished steel prices, especially rebar, continue to limit any significant upside in scrap prices.

Steelmakers that increased inventories had started securing scrap from mid-December to prepare for January output. These mills pursued aggressive buying and continued stockpiling despite substantial production cuts, resulting in higher inventory levels compared with December.

Note: This article has been written in accordance with a content exchange agreement between SteelDaily and BigMint.

Leave a Reply