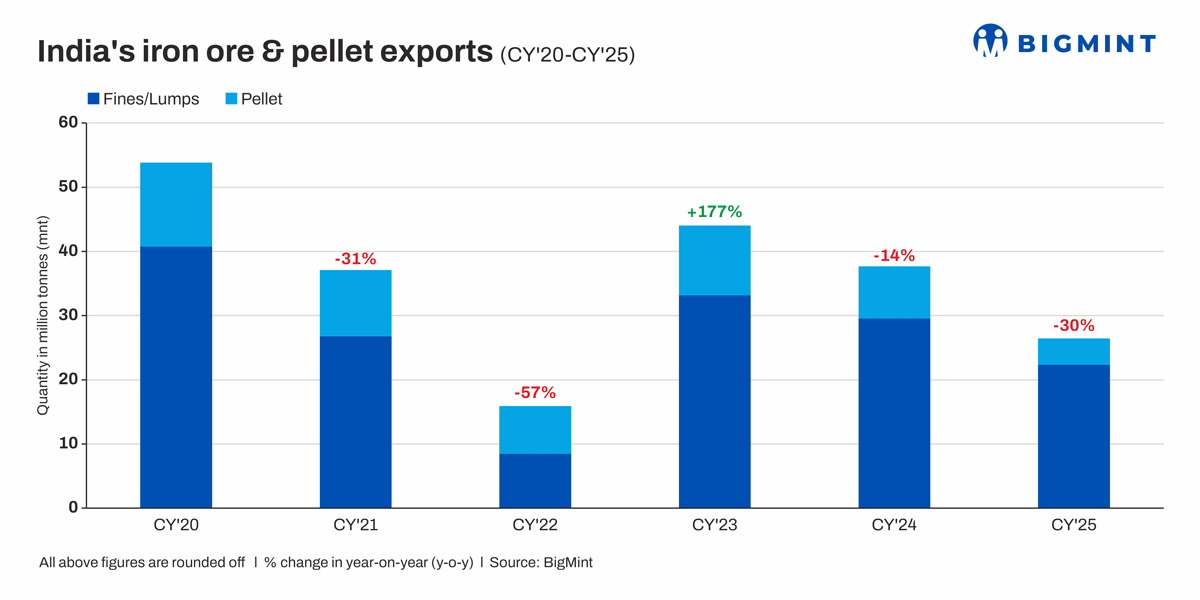

- Shipments drop to around 26 mnt from 38 mnt in CY’24

- Exports to China drop to 20.98 mnt from 34.99 mnt in CY’24

- Govt ‘not in favour’ of export duty on low-grade iron ore

Morning Brief: India’s exports of iron ore and pellets decreased sharply by 30% y-o-y to around 26.4 million tonnes (mnt) in CY’25, as per BigMint data, from nearly 38 mnt in CY’24. Iron ore and pellet exports have been steadily decreasing since 2023’s record of over 44 mnt, which was a direct result of the rescinding of export duty in late-2022.

Data show that iron ore exports fell from 29.5 mnt in CY’24 to 22.33 mnt in CY’25, while pellet exports dipped to 4.11 mnt in CY’25 as against 8.1 mnt in CY’24.

Country-wise exports

Exports to China fell from 34.99 mnt in CY’24 to 20.98 mnt in CY’25. Notably, Malaysia almost doubled its imports from India to around 1.75 mnt in CY’25 against 0.87 mnt in CY’24.

Notably, total exports to China have decreased from a level of over 41 mnt in CY’23 to around 22-23 mnt in CY’25.

Why iron ore exports plunged in CY’25?

Weak China demand: The significant decline in exports to China was the main factor behind decline in exports. China accounts for around 95% of Indian exports. However, crude steel production in China is estimated to have decreased by over 4% in CY’25 to below 1 bnt for the first time in many years. Production controls and weak domestic demand, which declined by over 5% in CY’25, weighed on steel production.

China’s iron ore imports remained high at around 1.26 bnt in CY’25, especially due to high steel exports of over 119 mnt in CY’25 and soft global prices. However, Indian low-grade fines exports dropped even as supplies from mainstream sources increased.

Slow growth in domestic production: BigMint data show that India’s iron ore production rose by just 4% y-o-y in CY’25 to around 295 mnt as against 283 mnt in CY’24. This, notably, is far lower than the pace of crude steel production growth of around 10% y-o-y in CY’25. Therefore, tighter availability in the domestic market kept exports on the lower side.

Price factor: Yearly average export prices for iron ore in CY’25 rose by just $1/t for low-grade fines (Fe 57%), FOB Paradip, to $64.5/t. Stagnant prices were a direct reflection of weakening global iron ore prices. Fe 62% CNF China prices dipped by $7/dmt to $100/t in CY’25 compared to an average of $110/t in CY’24.

On the other hand, domestic iron ore prices firmed up on tightening supplies. For instance, the share of lumps in total iron ore production fell to 27% in CY’25 from 30% in CY’24, indicating limited availability. Rapid growth in CDRI production contributed to a sharp 10% growth in lumps prices. BigMint’s Odisha iron ore index (Fe 62%) average prices increased by approximately INR 200/t y-o-y.

Similarly, our assessment shows that while average domestic pellet prices edged up around INR 200/t y-o-y in CY’25, exports prices fell by around $1/t. Therefore, prices were not propitious enough for exports.

Uncertain policy signals: Tight iron ore availability among steelmakers pushed domestic prices higher, intensifying competition and squeezing margins. This triggered market chatter around a possible policy move to restrict low-grade ore exports. While these remained unconfirmed, the weight of rumour was enough to impact market sentiment.

Outlook

Govt sources have, however, divulged that while an export duty on iron ore was considered some time back in August 2025, it is no longer favoured as a policy option. This will surely go some way in clearing the uncertainty around an export duty on iron ore.

Over the coming month, though, the only positive news is potential Chinese restocking ahead of the Spring Festival in mid-February and recent faint demand stimulus signals. However, softening global prices are a discouragement for Indian suppliers.

Leave a Reply