- LME cash prices rise 3% y-o-y

- Global zinc demand up 1-2% in 2025

The global zinc market in 2025 showed paper surpluses but physical tightness. Rising supply met weak demand, while collapsing inventories and concentrate constraints supported prices. In 2026, analysts expect clearer surpluses, inventory recovery, and flat-to-lower prices.

Prices, inventories

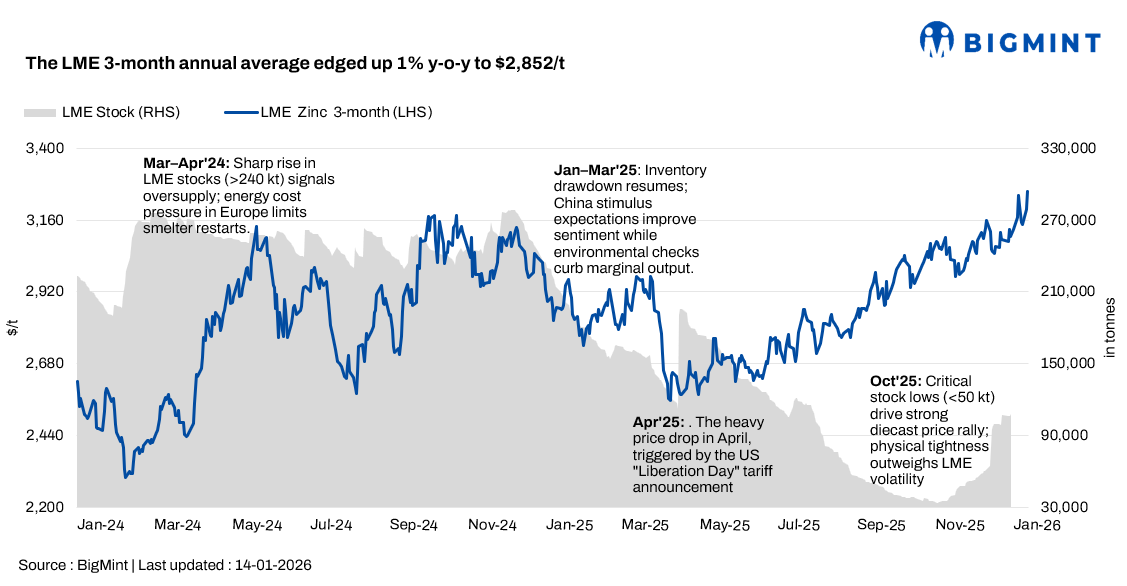

Despite weak demand, zinc prices proved resilient in 2025. LME 3-month zinc averaged $2,852/t, up around 1% y-o-y, while average cash prices rose 3% to $2,867/t. The key support came from a sharp contraction in visible inventories, which fell 54% y-o-y to around 113,700 t. LME on-warrant stocks collapsed from roughly 230,000 tonnes in January to below 34,000 tonnes by November, an 85% drawdown, driving pronounced backwardation of around $130/t.

In China, SHFE zinc prices consistently traded at premiums to LME, with an average SHFE–LME ratio of 8.1. Quarterly averages rose steadily from CNY 21,500/t in Q1 to CNY 23,000/t in Q4, supported by inventory tightness and construction demand. Chinese refined zinc output increased over 6% y-o-y to nearly 6.8 mnt.

Strong mine growth, constrained refined supply

Global zinc mine production rose sharply in 2025 as new projects and expansions came online. Key additions included Ivanhoe Mines’ Kipushi project in the DRC (278,000 mnt/year), expansions in Bosnia and Portugal, and the ramp-up of Boliden’s Odda smelter in Sweden. Macquarie estimates global mine output increased by around 5.8% y-o-y, more than double the International Lead and Zinc Study Group’s (ILZSG) initial forecast.

However, supply growth was uneven. Production disruptions at McArthur River (Australia), shutdowns at Tara (Ireland), and intermittent closures at Aljustrel (Portugal) constrained availability, keeping the market tight through early 2025. While these disruptions contributed to deficits in 2024, the ILZSG ultimately forecast a modest surplus of approximately 148,000 t in 2025 as new supply outweighed losses.

A key bottleneck remained zinc concentrate availability. Nexa Resources highlighted that tightness in 2025 stemmed from limited concentrate supply and cautious operating policies at Chinese smelters. Although higher concentrate stocks (such as Ozernoye in Russia) and restarts like Bunker Hill in the US eased pressure mid-year, global refined zinc output rose only about 3-3.6% y-o-y to 13.8 mnt, narrowly exceeding demand growth.

Demand: galvanizing weakness caps growth

Zinc demand in 2025 remained dominated by galvanized steel, which accounts for nearly half of global consumption. Weakness in housing, construction, automotive and infrastructure sectors sharply limited growth.

In China, persistent real estate stress weighed on steel production and zinc consumption, offsetting modest infrastructure support. In the US and Europe, high interest rates curtailed housing affordability and vehicle output. By late 2025, U.S. housing starts had stalled, unsold inventories surged, and European automakers such as Volkswagen and Stellantis announced factory shutdowns. Reflecting this slowdown, galvanized steel prices fell by around 17% in Europe.

Overall, global zinc demand grew only 1–2% in 2025. ILZSG data showed refined zinc demand rising about 2.5% in January-October 2025 to 11.44 mnt, compared with 11.19 mnt in the same period of 2024. Supply growth nonetheless outpaced consumption, reinforcing surplus conditions.

Macroeconomic scenario

The macroeconomic environment remained challenging throughout 2025. Elevated inflation and restrictive monetary policy kept real interest rates high, dampening industrial activity. Manufacturing PMIs in major economies stayed below 50 for much of the year.

Market sentiment deteriorated sharply in Q2 2025 following the US “Liberation Day” tariff announcements, which raised fears of weaker housing and manufacturing demand and a stronger US dollar. Although tariff-related concerns eased later in the year, subdued housing and automotive activity continued to cap zinc demand. Expectations of Federal Reserve easing by mid-2026 and gradual fiscal stimulus provided longer-term support but had limited impact during 2025.

Energy costs remained a structural constraint. In Europe, electricity and gas prices stayed elevated despite easing from crisis highs, forcing producers such as Nyrstar and Glencore to curtail output. And it was noted that subdued European premiums amid high power costs. In contrast, lower power prices in China allowed smelters to operate at higher rates. Analysts broadly agreed that elevated energy costs prevented refined output from reaching full capacity.

Policy environment

Policy developments also influenced the market. In China, regulators moved to curb non-ferrous overcapacity, proposing strict caps on new zinc smelting capacity from 2026 and reducing metals output growth targets to around 1.5% per year. In the US, zinc’s designation as a critical mineral supported project development, including FAST-41 approval for South32’s Hermosa zinc-lead mine.

India: prices strengthen

In India, zinc prices strengthened on a year-on-year basis in 2025, supported by firm domestic demand, higher input costs and supportive global cues. BigMint-assessed zinc ingot (Zn 99.995%) prices in north India (Ex-Delhi) rose from around INR 263,500/t in CY’24 to INR 283,300/t in CY’25, marking an 8% y-o-y increase. In western India, prices increased 7% y-o-y, from approximately INR 260,100/t to INR 278,100/t, driven by steady offtake from galvanising and alloying segments.

MCX zinc prices largely tracked LME movements but reflected additional volatility from INR currency fluctuations and local market premiums. Quarterly averages show MCX zinc at INR 262,000/t in Q1, falling to INR 238,000/t in Q2 during the tariff-led sell-off, before rebounding sharply to INR 292,000/t in Q3 and INR 316,000/t in Q4 as inventory tightness and seasonal construction demand supported prices.

Hindustan Zinc Limited (HZL) played a pivotal role, producing a record 827,000 tonnes in CY2025, up 1% y-o-y. While higher output reduced import dependence, global concentrate constraints and strong domestic consumption helped maintain price stability in the second half of the year.

Outlook for 2026

Most analysts expect zinc to move into a clearer surplus in 2026. The ILZSG forecasts mine output rising to 12.8 million tonnes and refined production to 14.13 million tonnes, while demand grows only 1% to 13.86 million tonnes, resulting in a surplus of around 271,000 tonnes. Price forecasts cluster lower, with Morgan Stanley at $2,900/t and Macquarie, the World Bank and Fitch at $2,450-2,500/t.

Overall, while inventory tightness supported zinc prices in 2025, rising supply and modest demand growth suggest range-bound to slightly lower prices in 2026, with market direction increasingly driven by inventory movements, Chinese supply policy and macroeconomic conditions.

Leave a Reply