- Sowing area in India estimated to be down 10% in 2025

- Supply pressure to remain limited in 1st half of season

Global cumin (jeera) sowing for the 2026 harvest season (from mid-February) presents a mixed picture of production trends, with India most likely remaining the leading producer and exporter despite a fall in acreage. However, developments in Turkiye and parts of the Middle East may influence export sentiment in the second half of the season.

It should be noted that given that data is available only for a few origins, directional signals from most competing countries have been analysed rather than confirmed acreage figures.

2026 trends, expectations

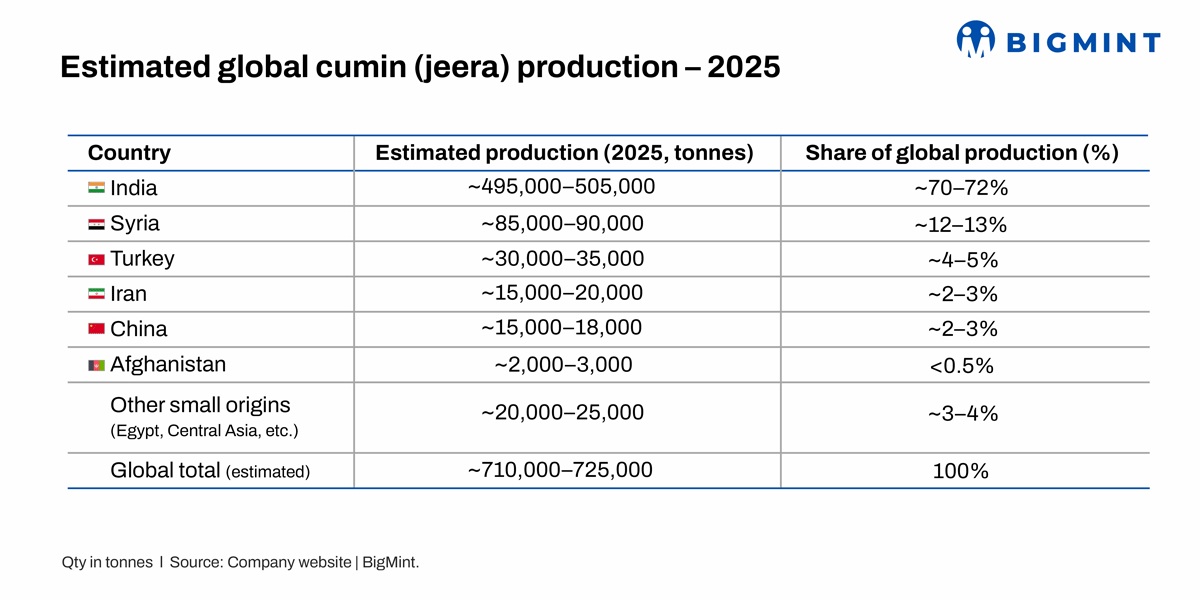

India: India’s total cumin sowing area is estimated to have declined by 10% from about 12.6 lakh hectares in 2024 to around 11.3 lakh hectares in 2025, which is likely to reduce cumin production from about 1.10 crore bags last year to nearly 90-92 lakh bags in 2025, or roughly 15-18% lower y-o-y.

This is mainly due to lower acreage in Gujarat and Rajasthan. In Gujarat, the cumin area is estimated to be 15-16% lower at about 5.6 lakh hectares in 2024 to around 4.7-4.8 lakh hectares in 2025, as farmers shifted to wheat, gram and maize due to weak cumin prices, high carry-forward stocks, and delayed sowing decisions.

In Rajasthan, cumin area is estimated to be 7-8% lower, as delayed sowing and better returns from mustard and gram discouraged cumin planting.

Turkiye: Outside India, Turkiye is the only major cumin-producing country publishing reasonably consistent official crop statistics. Turkish agricultural data for recent seasons indicate that cumin area has remained stable to slightly higher, with an expected yield of 35,000 t, supported by good farm-level returns and lower water requirement compared with cereals.

Turkiye’s sowing typically happens in late winter or early spring, with harvest arriving from May onwards, which means its supply enters the export market after Indian peak arrivals.

Syria, Iran: In contrast, Syria and Iran do not publish clean, nationwide jeera sowing data. Available information from FAO field notes and regional agriculture reports suggests that farmers in these countries have maintained or marginally adjusted area, depending on rainfall and input costs.

Syria continues to grow cumin as a winter crop, but geopolitical disruptions, logistics constraints, and uneven access to inputs mean that output reliability remains uncertain, even if area is unchanged. Iran shows similar patterns, with some provincial expansion plans offset by water stress and cost inflation.

China: China continues to influence global availability through a mix of domestic production and trading activity, but there is no transparent sowing data to confirm whether area has increased meaningfully versus last season.

Afghanistan: In Afghanistan, cumin cultivation remains opportunistic, accounting for a marginal share of global production. The cultivation area tends to expand when prices are attractive, but production and export flows are highly volatile due to infrastructure and security challenges. This makes Afghanistan more of a price disruptor in select nearby markets rather than a consistent global supply source.

Impact on Indian export dynamics

Why this matters is that India enters the global market first, with peak arrivals during February-March. Competing origins mainly arrive from May to July, creating a seasonal gap where Indian jeera dominates export pipelines.

As long as there is no confirmed surge in sowing area from Syria, Iran, or Turkiye, global supply pressure remains limited in the first half of the season. This keeps Indian prices sensitive mainly to domestic arrivals, quality mix, and export demand rather than global oversupply fears.

What may happen next is that the market will closely watch Turkiye’s final production numbers and Middle East weather outcomes during harvest. If Turkiye reports a higher-than-expected crop and Syria/Iran manage smooth exports, Indian jeera prices could face resistance in late Q2.

However, without clear evidence of a sharp global acreage increase, any downside is likely to be gradual, not structural. For traders and exporters, the key risk remains export demand timing, not global sowing expansion.

Leave a Reply