- Textile body flags rising cotton costs, margin stress for spinning millers

- Export competitiveness risk grows amid global tariff, demand pressure

India’s textile industry has renewed its demand for the permanent removal of the 11% import duty on raw cotton in the Union Budget 2026, citing measurable cost stress across the cotton–yarn–textile value chain. The request, led by the Confederation of Indian Textile Industry (CITI), follows the reinstatement of the duty from 1 January 2026 after the expiry of the temporary exemption.

High import costs hinder spinning millers’ operations

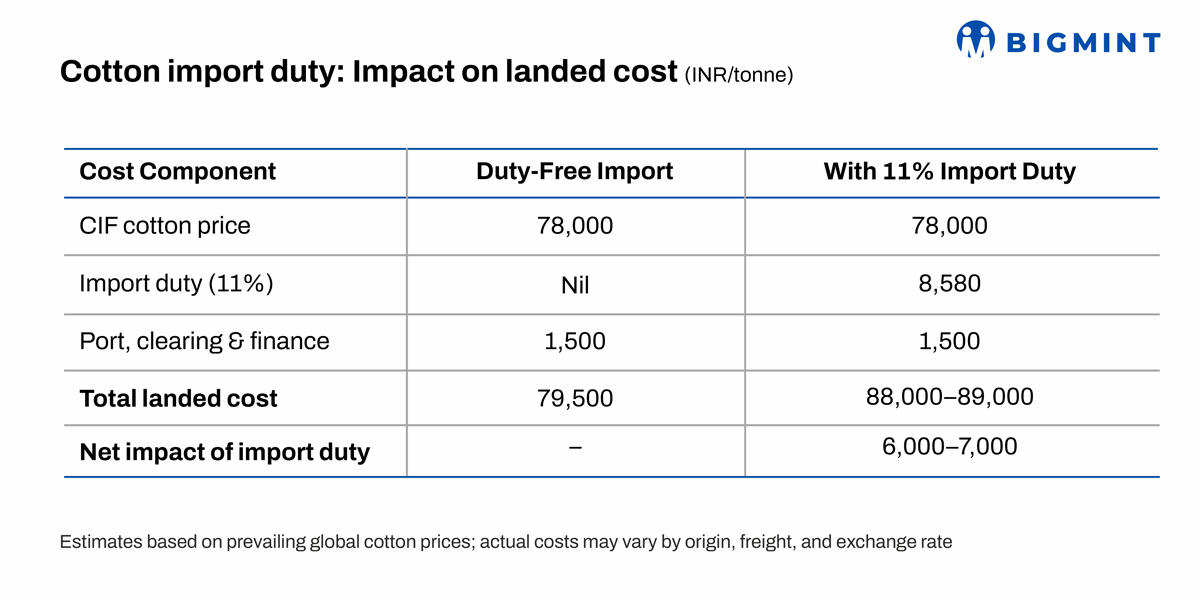

At prevailing international prices, the duty raises the landed cost of imported cotton by around INR 6,000-7,000/tonne (t), materially impacting spinning millers who depend on imports for consistent quality and finer counts.

During the duty-free window between August and December 2025, imported cotton acted as an effective price benchmark for the domestic market. Domestic spot prices largely tracked international parity, limiting sharp upside during tight arrival phases and improving raw material availability. Spinning millers benefited from better cost visibility, while brokers saw steadier trade flows as imports capped volatility.

With the duty back in place, imported cotton has turned largely unviable, reducing inflows and removing this external price discipline. As a result, domestic prices have become more sensitive to arrivals, quality variations, and holding by trade.

Duty removal to help bridge quality gaps, ease raw material costs

If the import duty is permanently removed in Budget 2026, cotton imports from origins such as Brazil, Australia, and the US are likely to resume. This would help bridge quality gaps in the domestic crop and keep Indian cotton prices aligned with global benchmarks. For spinning millers, raw material costs could ease by 4-6%, directly supporting yarn margins at a time when yarn realisations remain under pressure. Export competitiveness would also improve, as Indian yarn and textiles would price more closely against suppliers from Bangladesh and Vietnam, where cotton imports are largely duty-free.

If the duty continues, domestic cotton prices may remain structurally firm, but downstream demand risks weakening. Higher cotton costs are difficult to pass on fully in yarn and fabric prices, raising the risk of margin compression and lower spindle utilisation. In such a scenario, indirect pressure could build on the Cotton Corporation of India (CCI). With private trade demand potentially slowing at higher price levels, a larger share of arrivals may gravitate towards MSP-linked procurement, increasing CCI’s buying volumes, inventory carrying costs, and policy management burden for the government.

Conclusion

Overall, the Budget 2026 decision on cotton import duty will influence not only prices and trade flows but also institutional market dynamics. Duty removal would prioritise competitiveness, exports, and smoother price discovery, while duty retention could support domestic prices at the cost of downstream demand and higher procurement pressure. For ginners, spinning millers, and brokers, policy clarity on cotton imports will remain a key driver of price direction and risk management in the 2026-27 season.

Leave a Reply