- Sharp increase in production outpaces demand growth

- Q4 outlook hinges on demand revival amid market surplus

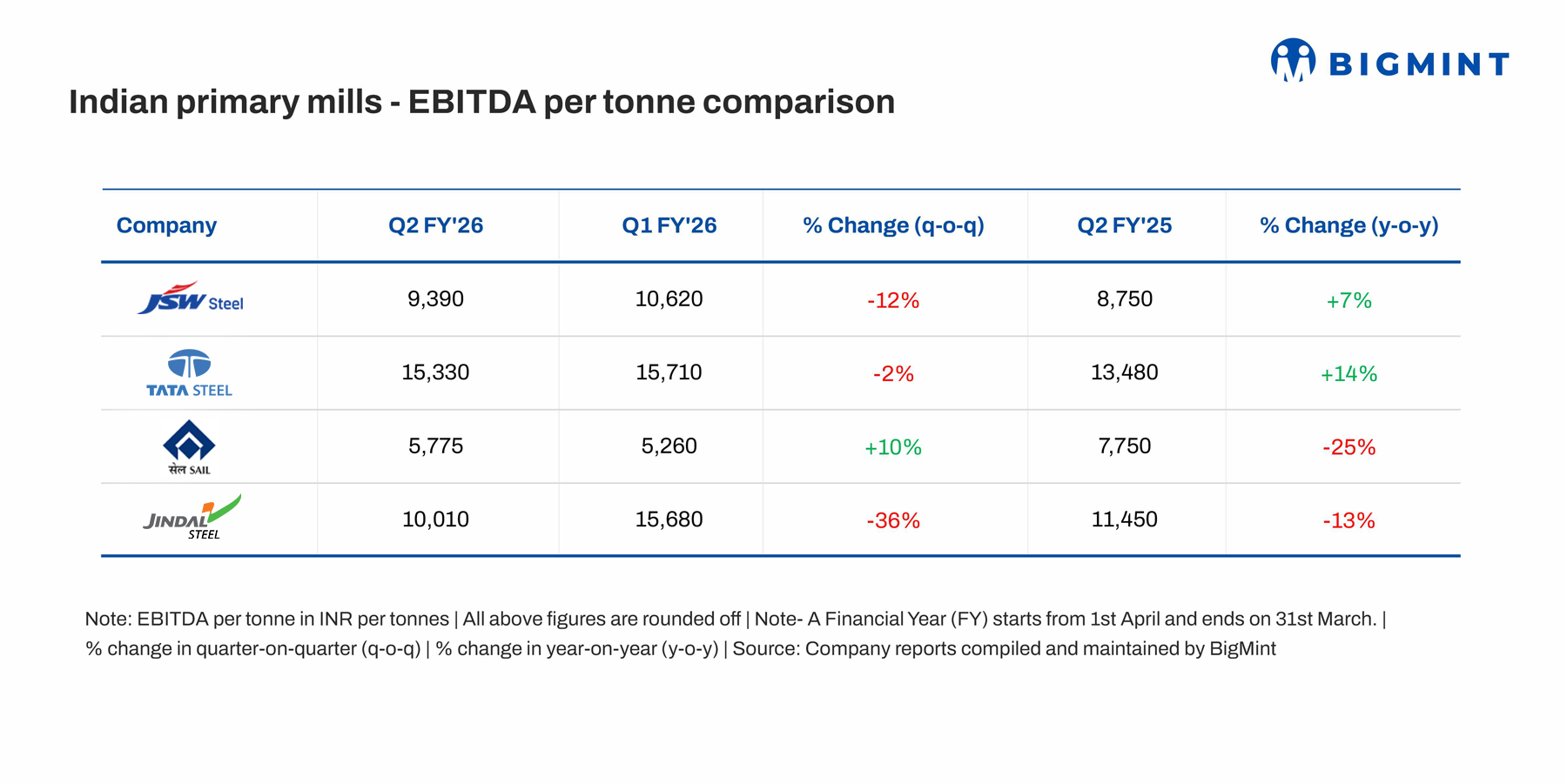

Indian steel mills are projected to report lower profit margins for the December quarter (Q3FY26), belying expectations of a pick-up after the monsoon. Aggregate EBITDA per tonne for the top four mills is projected to range about INR 9,253- 9,675, corresponding to a sequential decline of 7-11%. On y-o-y basis, the decline is less severe at 0-4%. The performance is quite similar to Q2FY26, when aggregate EBITDA per tonne fell by 10% on sequential basis, although it rose by 13% y-o-y, primarily led by higher volumes.

The performance is impacted by a sharp increase in production and muted demand growth, leading to pressure on prices. As per Joint Plant Committee (JPC) report, production growth in the first two months of Q3FY26 (October-November) stood at 10.5%, against growth of only 5.2% in consumption.

As a result, prices of hot rolled coils (HRC) declined by 5% on sequential basis, to INR 47,212/t, whereas rebar (ex-Mumbai, BF route) prices fell by 2% to INR 47,250/t. While y-o-y decline for HRC was only marginal at 1%, finding some support from the interim safeguard duty, rebar fell more sharply by 12%.

Besides, mills also faced cost pressure with coking coal (0-40mm, Premium HCC) prices rising sharply by 9% sequentially, to INR 19,432/t. Prices have risen because of lower production in China, impacted by harsh weather conditions, compounded by the rupee depreciation. Iron ore (0-10 mm, Odisha, Fe 62%) also faced pressure with a 3% increase, both sequentially and y-o-y basis, to INR 5,496/t. However, a price cut taken by NMDC in October kept prices benign.

Company-wise performance

In terms of individual performance, JSW Steel and Tata Steel are projected to see large sequential declines of 7-14% and 8-11%, respectively, impacted by higher decline in HRC prices. Their performance is similar to Q2FY26, when their EBITDA per tonne had fallen by 12% and 2%. Notably, both had seen a seven-quarter high EBITDA per tonne in Q1. While the imposition of the safeguard duty for three years should help improve the realisation in Q4, price trends would need to be closely monitored considering the market surplus in flat products.

Steel Authority of India Ltd (SAIL) is projected to see a sequential decline of 5-8% in its EBITDA per tonne, after recording an improvement of 10% in Q2. This would still be higher than the 10-quarter-low figure of INR 5,260, hit in Q1. SAIL has the lowest EBITDA margin of about 7%, because of high other operating expenditure.

The outlier is Jindal Steel (earlier, Jindal Steel & Power), which had seen a sharp decline of 36% in its sequential EBITDA per tonne in Q2, after hitting a 10-quarter high of INR 15,680 in Q1. The company is projected to see an improvement of 6-8% in its margin on sequential basis.

Outlook

While the outlook for the steel mills looks promising, much would depend on how domestic demand shapes up in the seasonally strong fourth quarter and whether the GST rate cut leads to any demand pick up for steel mills. As per JPC report, during July-November (Q2) and first two months of Q3, consumption growth stood at 7.4%, lower than 7.9% in Q1. On the other hand, production growth rose sharply to 12.2%, against 7.6% in Q1, creating a significant demand supply imbalance.

With new facilities expected to see a ramp up, the market may continue to see a surplus in Q4. A sustained growth in exports, with India turning a net exporter in October-November, could be another important factor for the steel mills.

Disclaimer: The data, projections, and opinions contained herein are based on sources considered reliable at the time of publication but are not guaranteed for accuracy or completeness. This content does not constitute investment, trading, or financial advice, nor does it recommend or endorse any specific securities or companies. Bigmint does not assume any liability for decisions made based on this information. Readers and stakeholders are encouraged to conduct their own due diligence and consult qualified advisors for investment decisions.

Leave a Reply