- Offtake increases in 5 Jan auction, but buying stays controlled

- G4 dominates both auctions, with mostly lower-CV grades cleared

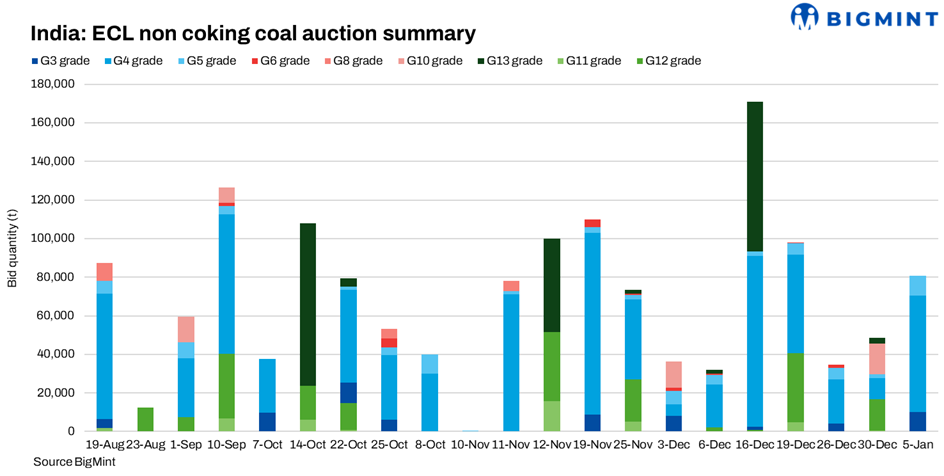

Eastern Coalfields Limited’s auctions on 30 December 2025 and 5 January 2026 signalled cautious, disciplined restocking. On 30 December, ECL sold 65,450 t at an average bid price of INR 3,888/t, reflecting defensive year-end procurement, as mostly lower-CV grades were cleared at reserve prices, with buyers unwilling to pay any premium. Participation was shallow, with buyers spreading bids across grades and avoiding aggressive pricing.

The 5 January auction saw sold volumes increase to 80,850 t, while the average bid price moved higher to INR 5,093/t. The rise in value was driven more by G4-focused restocking at only marginally higher prices, again pointing to selective restocking rather than urgency-led or aggressive buying.

Grade-wise performance

On 30 December, total bid quantity stood at 65,450 t, led by G4 at 21,700 t, followed by G9 and G12. G4 prices averaged INR 4,483/t, while lower-CV grades such as G13 cleared at utility-linked levels near INR 1,713/t.

The 5 January auction saw stronger participation, with the total bid volume rising to 80,850 t. G4 dominated allocations at 60,400 t, with higher average realisations of INR 4,793/t, indicating firmer demand for quality mid-CV coal. G3 also saw notable uptake at improved prices, while G5 volumes increased moderately.

Mine-wise highlights

UG-origin coal continued to command a premium. In the 30 December auction, Jambad UG (G3) achieved a high realisation of INR 7,452/t, while UG mines such as Jhanjra, Khottadih, and Kumardihi A cleared G4 at levels above OC equivalents.

The 5 January auction further underlined UG strength, with Nimcha UG and Narsamuda UG recording elevated G4 prices, while large OC suppliers such as Sonepur Bazari and Khottadih OC cleared significant volumes at stable but lower averages.

Buyer behaviour

Buying on 30 December was fragmented, led by Saroj Commodities, Compact Weighing, Khatu Shyam Steels, and Shree Bahubali Mercantile, with most buyers lifting mid-sized parcels and focusing on G4 and select G12 material.

On 5 January, participation widened, with traders such as Kiran Khan, Mark Trading Company, Khemka Minerals, Khatu Shyam Steels, and Ranisati Coal Carriers actively bidding, primarily for G4 coal. Despite higher volumes, procurement remained targeted rather than aggressive.

Takeaway

The two auctions together pointed to a restocking-driven increase in volumes, not a demand-led rally. While January saw higher quantities and a stronger average realisation, procurement remained measured, reinforcing that the domestic coal market stays well supplied, with buyers firmly in control of market dynamics.

Leave a Reply