- Around 1.04 mnt of new capacity slated for commissioning

- Reduction in steel production to cap demand pull for ferro silicon

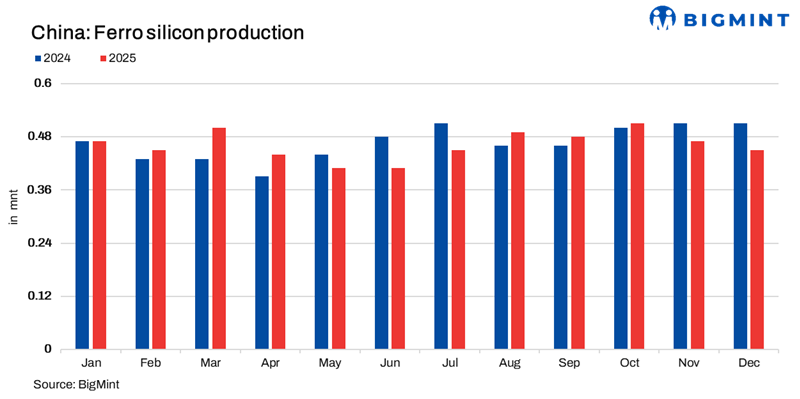

Mysteel Global: China’s ferro silicon market is expected to face challenges in 2026 with the rush of new capacity coming on stream amidst a structural slowdown in steel production, the ferroalloy’s core consuming sector, Mysteel’s annual report on the commodity observed.

Major supply pressure will materialize gradually in the second half of 2026, according to the report. Approximately 1.04 million tonnes (mnt) of new ferro silicon capacity is slated for commissioning during this year’s July-December half, primarily from four large-scale projects.

Meanwhile, projects with a higher probability of commissioning in 2026 include delayed 2025 projects in Gansu, a medium-carbon ferro manganese-supporting project in Inner Mongolia, and a capacity replacement project in Shaanxi involving a combined 252,000 tonnes/year of annual capacity, according to Mysteel data.

Industry analysts also warn of the potential seismic impact of a major integrated ‘source-grid-load-storage’ (SGLS) project in Inner Mongolia once this becomes fully operational. SGLS projects integrate the power resources of the source, network, load, and energy storage sides for more efficient use and storage of electricity, Mysteel Global notes.

Meanwhile, over the past two years the government of the Xinjiang Uygur Autonomous Region in northwest China has approved several new projects in the “semi-coke – ferro silicon- magnesium metal” chain which seem set to introduce substantial long-term supply into the market beginning from this year.

On the demand side, the outlook for ferro silicon is equally challenging, the report points out. Steel, which consumes the bulk of ferro silicon, is undergoing a structural phase of “volume reduction and stock optimization,” which will cap its demand pull for ferro silicon. Growth in other key sectors, such as stainless steel and magnesium, is seen as being too modest to absorb the massive burgeoning of new ferro silicon supply.

In stainless steel, only the 2.51 million t/y being actioned by the Hangzhou Iron & Steel-Zhenshi Holding Group joint venture, and Guangdong Guangqing Technology’s 400,000 t/y project, are on track for commissioning in 2026. Most other planned capacity increases face likely delays amid thin margins and intense competition, Mysteel surveys indicate.

The magnesium sector offers little relief too, with sluggish conditions and weak downstream demand likely to suppress new capacity additions in 2026. Total capacity is projected to grow by a mere 5.9% on year to 1.44 million t/y, according to Mysteel survey results.

Compounding the demand shortfall, ferro silicon exports are forecast to contract to 380,000 tonnes this year under sustained pressure from the international market.

However, the silver lining is that costs will provide support for the ferrosilicon market. The price of the crucial ferro silicon raw material, semi-coke, is expected to rise moderately in 2026, which will help underpin ferro silicon prices.

More significantly, Shaanxi province will impose a surcharge on electricity prices for the ferroalloy sector starting from July 1 2026. Although many smelting plants have captive power, those relying on grid electricity will face an additional charge of Yuan 0.1/kWh (cents/kWh), directly increasing the industry’s production cost curve.

During 2026, ferro silicon prices will be squeezed between rising costs and crushing overcapacity, Mysteel’s report grimly concluded. Profitability will hinge less on market prices and more on access to low-cost power, stable raw materials, and avoiding punitive power tariffs. This marks a decisive industry shift from scale competition to cost-structure competition, it remarked.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply