- Rising geopolitical uncertainty raises risk appetite

- Optimistic demand outlook supports bullish sentiment

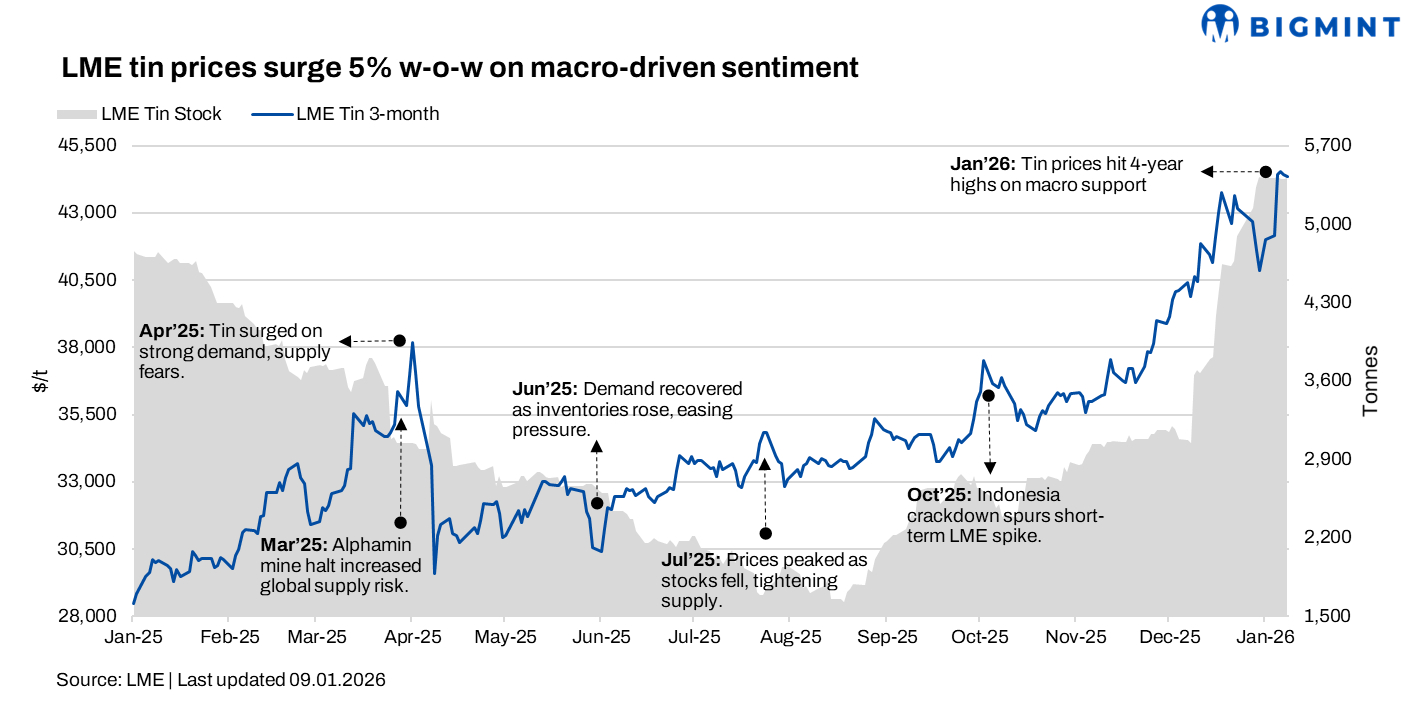

Tin prices on the London Metal Exchange (LME) surged in the week ended 09 January 2026 (week 2), driven by macro factors, geopolitical uncertainty, and strong futures participation, while a positive demand outlook supported sentiment despite spot market resistance and cautious downstream procurement limiting fundamental backing.

Pricing, inventory trends

LME tin prices averaged $43,985/tonne (t) in the week ended 09 January, marking an $2,198/t or 5.3% rise w-o-w from the previous week. The week began with prices at $42,150/t, which inched up to around $44,525/t mid-week and then closed at $44,350/t.

Meanwhile, tin inventories at LME-registered warehouses rose 2% to 5,412 t from 5,328 t in the previous week.

What impacted prices?

LME tin prices rose w-o-w, supported primarily by strong macro-driven sentiment rather than fundamentals. Rising geopolitical uncertainty boosted risk appetite across the metals complex, while synchronised gains in SHFE prices and increasing futures positions signalled strong speculative participation.

Positive global demand cues, including optimism around semiconductor demand and improving Chinese auto consumption indicators, further lifted sentiment. However, the rally was largely futures-led, as spot market resistance and cautious downstream procurement limited fundamental backing at elevated price levels.

Outlook

LME tin prices may consolidate at elevated levels in the near term as macro and geopolitical factors continue to support sentiment. However, rising inventories, cautious spot demand, and limited fundamental support could cap further upside and increase the risk of near-term price corrections.

Leave a Reply