- HRC prices rise on safeguard duty support, mills’ list price hikes

- IF rebar prices slide as buyers show resistance at higher levels

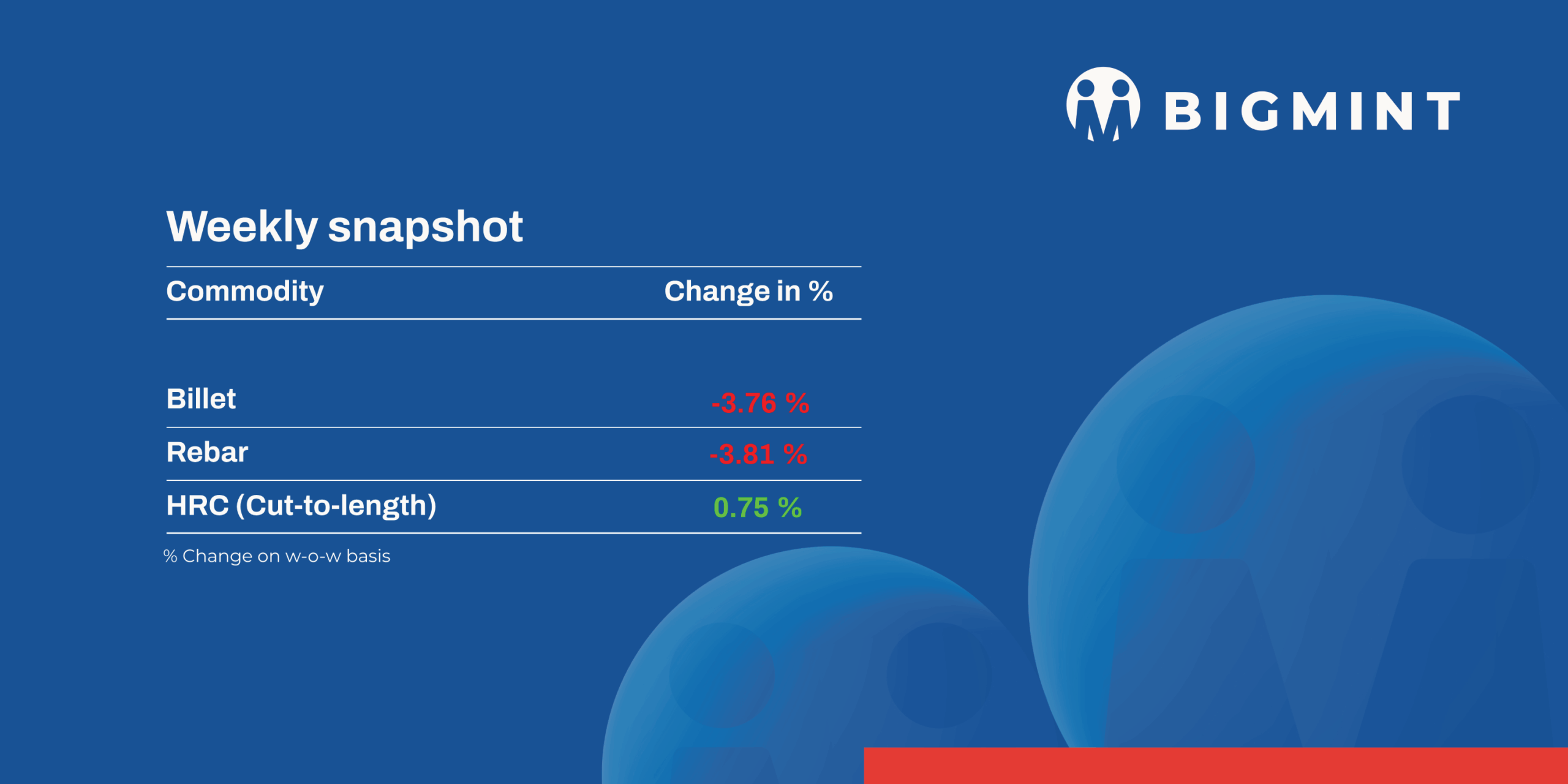

The Indian steel market saw contrasting trends during week 2 of CY’26 (5-9 January). Semi-finished steel prices dropped in the range of INR 700-2,200/tonne (t), with flat steel and BF rebar prices climbed up. Demand remained uneven across segments, with trading momentum slowing across the IF segment, evidenced by price drops across sponge iron, billet, and IF rebar. List price hikes by primary mills, however, supported flat steel and BF rebar prices.

Iron ore, pellet

- NMDC announced its list prices of iron ore CLO (calibrated lump ore) and fines on 9 January, BigMint learnt from sources. The miner has fixed prices of DR CLO (10-40 mm, Fe 67%) at INR 5,150/t ($57/t) and of iron ore fines (-10 mm, Fe 64%) at INR 3,900/t ($43/t). Prices are on FOR basis from the miner’s Bacheli complex and exclude royalty, DMF, and NMEDT. However, official confirmation from NMDC is still awaited. NMDC has shifted its pricing structure from a tax-inclusive model to one that excludes royalty, DMF, and NMEDT charges.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices increased by $3/t w-o-w to $69/t FOB east coast on Thursday, tracking the slight rebound in global iron ore prices. Meanwhile, the index stood at $79/t CFR China. The uptick comes despite muted demand, particularly from China, where high portside inventories continue to cap buying interest. However, prices remained under pressure, with some sources stating that the export discount for Fe 57% fines widened to around 22-23%, while Fe 54-55% material saw discounts increase to nearly 30% against the global fines index.

- BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index remained largely stable w-o-w at $107.5/t FOB east coast on Wednesday. Additionally, a producer offered around 50,000 t of Fe 64.5% pellets on 7 January, sold at a higher price level ($119-120/t FOB India) due to lower alumina content.

Coal

- Indian portside South African thermal coal prices inched up w-o-w in early January 2026, although trading activity remained limited. RB2 (5,500 NAR) increased by INR 50/t to INR 9,050/t exw Paradip, while Vizag prices rose to INR 8,950/t. RB3 (4,800 NAR) firmed up to INR 7,600/t at Paradip and INR 7,550/t at Vizag. Higher offers of INR 9,000-9,300/t were quoted across Mangalore, Ennore, Paradip and Gangavaram, supported by seasonal tightness at RBCT during the winter and New Year holidays, though no trades were heard.

- Domestic coal prices remained flat w-o-w, with 5,000 GCV at INR 5,750/t and 4,500 GCV at INR 4,800/t, as per BigMint’s assessment. In South Eastern Coalfields Limited’s bulk auction on 7 January 2026, around 70-80% of the 3.4 mnt offered was booked, largely near floor prices, reflecting comfortable supply and cautious, need-based buying.

- India’s BF-grade metallurgical coke prices strengthened w-o-w in the week ended 7 January 2026, supported by improved steel demand and reduced import viability following anti-dumping duties. In eastern India, BF-grade met coke (25-90 mm) rose by INR 200/t to INR 32,200/t ex-Jajpur, while western India prices increased by INR 300/t to INR 30,100/t ex-Gandhidham. A few deals at INR 33,000/t ex-Jajpur lifted offers to INR 34,000/t. Import bookings remained absent as landed costs stayed unattractive, although selling pressure persisted in western India.

- BigMint’s premium hard coking coal (PHCC) index was assessed at $238/t CNF Paradip on 9 January 2026, up $2/t w-o-w, with trade activity remaining thin.

Ferrous scrap

- India: India’s imported scrap market remained quiet, as better steel demand failed to trigger demand amid largely unworkable offers. EU/UK shredded stayed near $355/t CFR, while HMS 80:20 held at $330-335/t CFR.

- German busheling was quoted at $365-375/t CFR, with limited confirmations around $370/t. Despite lower Australian offers, buyers stayed cautious and price-sensitive, restricting trade activity.

- About 3,000-3,500 t of imported scrap arrivals were recorded, including around 1,000-1,500 t of HMS 80:20, along with additional LMS and NTP.

Metallics

- The sponge iron market witnessed a pronounced correction. Prices across key producing regions fell by INR 700-1,400/t ($7-15/t) w-o-w, as procurement activity slowed across all regions. Buyers remained cautious, refraining from fresh purchases amid persistently weak downstream steel demand, despite the price corrections.

- SAIL’s Rourkela Steel Plant (RSP) conducted an auction on 5 January for 3,500 t of steel-grade pig iron, in which the entire quantity was booked at an average price of INR 38,100/t exw. This marks a rise of INR 4,350/t compared to the previous auction on 18 December, in which the entire quantity of 1,100 t was sold at INR 33,750/t exw.

- On the export front, Indian DRI offers edged lower by $3-5/t w-o-w, with prices assessed at $312/t CPT Raxaul for Nepal and $320/t CPT Benapole for Bangladesh. Despite the downward price adjustment, export demand from both destinations remained limited.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices inched up by INR 975/t ($11/t) w-o-w to INR 70,800-71,400/t ($784-791/t) across Durgapur, Raipur, Vizag, and Raigarh. The increase was supported by better acceptance of higher offers, firm smelter pricing, rising manganese ore costs, limited supply, and a modest recovery in steel demand.

- Ferro manganese: Indian high-carbon ferro manganese (70%) prices edged up by INR 200/t ($2/t) w-o-w to INR 71,700/t in Durgapur and INR 72,000/t in Raipur. The rise was supported by steady steel demand and limited spot availability, encouraging sellers to raise offers across key producing regions.

- Ferro silicon: Indian ferro silicon (Si 70%) prices fell by INR 2,000/t ($22/t) w-o-w to INR 94,000/t ($1,042/t) exw Guwahati, while Bhutan prices eased by INR 1,300/t ($14/t) to INR 94,000/t ($1,042/t). The decline followed Bhutan’s announcement of its January 2026 offers, which weighed on market sentiment.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices edged down by INR 700/t ($8/t) to INR 105,600/t ($1,170/t) exw Jajpur. Although buyers expected prices to soften further, sellers held firm on offers, limiting any significant downside in the market.

Semi-finished steel

- India’s semi-finished steel market weakened sharply this week, as per BigMint’s assessment. Domestic billet prices across major markets recorded a steep decline of INR 800-2,200/t ($9-24/t) on a w-o-w basis, driven by softening buying interest in the semi-finished steel segment. Continued weakness in finished steel offtake further intensified the downtrend, leading to a loss of price momentum across markets.

Finished long steel

- IF-rebar: India’s induction furnace (IF) route rebar prices declined by INR 500-1,800/t across regions during the week. Market sentiment remained cautious due to a lack of clarity, as traders booked material at varied prices and showed limited interest in purchasing at higher rates. In response, mills and manufacturers increased trade discounts, leading to price softening. Although prices were on the upward side at the beginning of the week, they later corrected downward. Mills did not face inventory pressure and currently hold forward bookings of around 8-10 days, depending on location. In the near term, market sentiment is expected to remain stable.

- On a weekly basis, rebar prices decreased by INR 500-1,800/t across regions, as per BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size were assessed at INR 42,600-43,200/t exw Raipur and INR 48,700-49,300/t exw Jalna.

- Trade reference prices of heavy structural steel for base size 150mm channel stood at INR 44,800-45,200/t exw Raipur.

- Trade reference prices of wire rod stood at INR 43,200-43,700/t ex Raipur.

- BF-rebar: Trade-level BF rebar prices rose w-o-w across major Indian markets, supported by recent price hikes announced by primary mills, improved trading activity, and tight material availability in the distribution channel. Primary producers raised rebar list prices by up to INR 1,000/t ($11/t) during the week, taking landed prices to around INR 52,000-53,000/t ($577-588/t). As a result, trade-level BF rebar prices increased by INR 600/t ($7/t) w-o-w to approximately INR 52,500/t ($583/t) exy-Mumbai, excluding 18% GST.

- Strong offtake in the trade segment and reduced supplies led to shortages in select sizes, pushing offers higher. In the projects segment, prices were assessed at INR 51,500-52,500/t ($571-582/t) on a FOR basis. Healthy order bookings and rising backlogs at mills continued to support market sentiment. Meanwhile, offers were also heard at around INR 53,000/t ($588/t) at the end of the week.

Flat steel

-

- Trade-level prices of hot-rolled coils (HRCs) in India increased w-o-w to INR 49,000-51,600/t ($543-572/t) across regions. Additionally, cold-rolled coil (CRC) prices rose w-o-w, ranging between INR 53,500-58,700 ($593-651/t).

- Domestic HRC prices have stayed high after two price hikes in December and another increase in early January 2026. Steelmakers are raising prices following the safeguard duty announcement, supported by policy, restocking activity, and positive market expectations, even though demand is moderate.

- India’s bulk imports of HRCs touched 380,944 t as of 31 December, based on vessel line-up data. Around 125,188 t of additional cargoes are expected by mid-January.

- India’s bulk exports of HRCs touched 430,090 t as of 31 December.

- BigMint’s Indian HRC (S275) export index for the European Union (EU) remained unchanged w-o-w at $520/t FOB main port, as trading activity in the region remained limited due to the year-end holiday slowdown.

- Indian HRC (SAE 1006) export index for the Middle East also remained stable w-o-w at around $465/t. A BigMint source indicated that market activity is expected to pick up after the New Year break and with the start of the new fiscal year in the region.

Leave a Reply