- Seasonal tightness lifted offers but trades stayed limited

- Ample domestic supply capped upside across coal markets

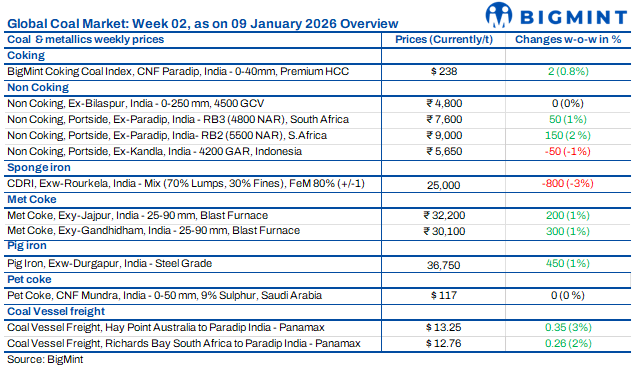

Coal market sentiment this week remained broadly cautious across domestic and seaborne segments. Seasonal tightness in select export origins lent some support to offers, but ample domestic availability and comfortable inventories limited deal conversions. Buying stayed largely need-based, with participants adopting a wait-and-watch approach amid mixed downstream signals. Freight softness and logistical constraints influenced flows, while demand from steel and power sectors showed uneven recovery. Overall, sentiment stayed balanced, with stability prevailing over directional moves.

Indonesian coal prices steady

Indian portside prices of Indonesian non-coking coal remained largely stable w-o-w in the week ended 9 January 2026, as weak demand and sufficient inventories limited price movement. Prices of 5,000 GAR stayed unchanged at INR 7,200/t at Kandla and INR 7,100/t at Vizag, while 4,200 GAR eased by INR 50/t to INR 5,650/t and INR 5,550/t, respectively. Lower-grade 3,400 GAR remained steady at INR 4,450/t at Navlakhi. Power plant coal stocks declined by 1% w-o-w to 52.92 mnt, offering around 17 days of cover, though 16 plants remained under critical levels due to logistical issues. Indonesian benchmark prices edged up by $0.27-0.79/t, but this had limited impact on Indian prices amid cautious buying sentiment.

Seasonal tightness lifts South African coal offers

Indian portside South African thermal coal prices edged up marginally w-o-w in early January 2026, though trade activity remained thin. Exw Paradip, RB2 (5,500 NAR) rose by INR 50/t to INR 9,050/t, while at Vizag it increased to INR 8,950/t. RB3 (4,800 NAR) also firmed to INR 7,600/t at Paradip and INR 7,550/t at Vizag. Offers were quoted higher at INR 9,000-9,300/t across Mangalore, Ennore, Paradip and Gangavaram, supported by seasonal tightness at RBCT during winter and New Year holidays, but no deals were concluded. FOB RBCT RB2 hovered at $78-79/t against bids of $73-74/t, while RB3 offers stood at $68-69/t versus bids near $61/t. Portside stocks stayed broadly stable at 12.95 mnt. Meanwhile, sponge iron prices fell by INR 200-500/t, with CDRI exw-Rourkela down INR 300/t to INR 25,000/t, limiting upside acceptance.

India: Domestic coal prices hold steady as SECL auction sees moderate uptake

Domestic coal prices remained unchanged w-o-w, with 5,000 GCV assessed at INR 5,750/t and 4,500 GCV at INR 4,800/t, according to BigMint’s assessment. In the recent bulk auction conducted by South Eastern Coalfields Limited on 7 Jan’26, around 70-80% of the 3.4 mnt offered was booked. Most volumes cleared close to floor prices, indicating comfortable supply conditions and cautious, need-based buying by participants.

BigMint’s coking coal index inches up w-o-w

BigMint’s premium hard coking coal (PHCC) index was assessed at $238/tonne (t) CNF Paradip, India, on 9 January 2026, up by $2/t against the previous assessment on 2 January last. Although trade activities remained limited, offers remained on higher side as trader sources expect prices should go up due to weather related disruptions in Australia.

Met coke domestic prices in India strengthen

India’s BF-grade metallurgical coke prices strengthened w-o-w in the week ended 7 January 2026, supported by improved steel demand and reduced import viability after anti-dumping duties. In eastern India, BF-grade met coke (25-90 mm) rose by INR 200/t to INR 32,200/t ex-Jajpur, while western India prices increased by INR 300/t to INR 30,100/t ex-Gandhidham. A few deals were reported at INR 33,000/t ex-Jajpur, pushing offers to INR 34,000/t. Import bookings remained absent as landed costs turned unattractive, supporting domestic prices, though sales pressure persisted in western India. Australian PHCC stayed steady at $218/t FOB, while China’s coke market remained weak. Pig iron prices surged, with steel-grade pig iron ex-Durgapur up INR 1,900/t to INR 36,500/t, lending further support. However, AD duty uncertainty and weak foundry demand kept sentiment cautious.

US petcoke prices firm

Petroleum coke prices showed a mixed but generally firm trend from December 2025 into early January 2026. U.S. export prices strengthened, supported by lower freight costs and steady overseas interest. FOB USGC prices for 4.5% sulphur material rose to $79-80/t, while 6.5% sulphur reached $72-74/t. On the USWC, low-sulphur coke jumped to $140-158/t, a nine-month high. In import markets, Turkey prices stayed near $103-108/t CFR, while India eased slightly to $111-117/t. China showed diverging trends, with low-sulphur grades rising by $10/t or more. Strong pre-holiday Chinese demand, falling freight rates and geopolitical tensions involving Venezuela supported sentiment, though competition from thermal coal capped gains in price-sensitive markets.

Coal freights mixed w-o-w

Dry bulk coal freight rates showed mixed trends w-o-w across key India-bound routes, as ongoing enquiries offered limited support but ample vessel availability capped gains. Market sentiment remained subdued amid cautious early-year buying by Indian importers, comfortable coal inventories and abundant prompt tonnage. Falling bunker prices and softer FFAs reduced voyage costs and weakened owners’ resistance to rate concessions.

On the Panamax segment, Australia (Hay Point)-India (Paradip) rates edged up by $0.4/dmt to $13.25/dmt, while South Africa (Richards Bay)-India (Paradip) increased by $0.3/dmt to $12.76/dmt, driven by selective fixtures rather than broad strength. In contrast, Indonesia (East Kalimantan)-India (Navlakhi) Supramax rates declined by $1.8/dmt to $11.01/dmt due to muted cargo volumes. Overall, limited cargo urgency and oversupplied tonnage kept freights under pressure.

Leave a Reply