- Kanto tender supports prices; spot demand weak

- US scrap exports subdued; shredded supply tightens

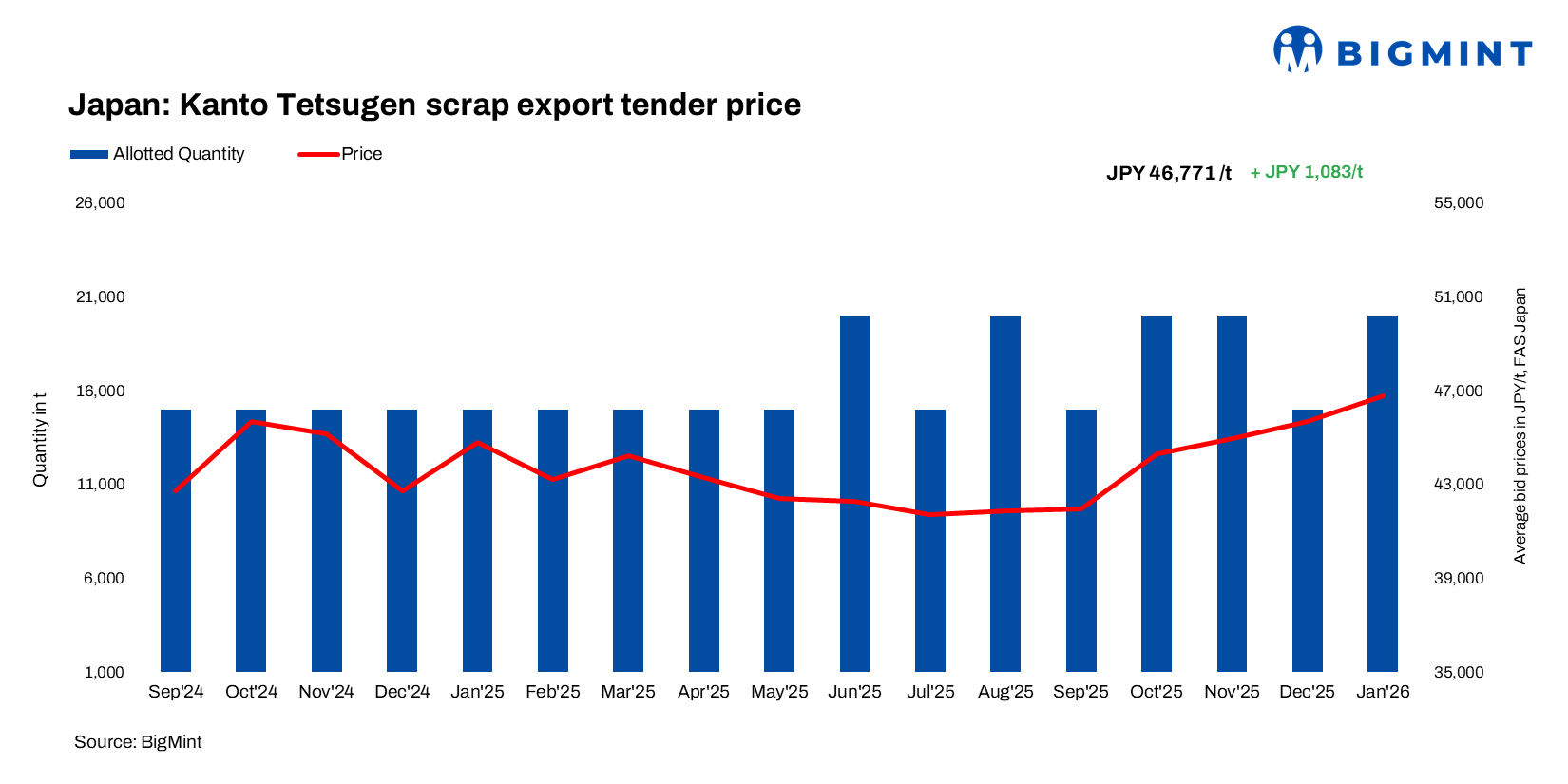

Japan’s Kanto scrap tender hits a 17-month year-high in Jan 2026–the sixth consecutive monthly rise (up by JPY 1,083/t)–marking the strongest prices since the Aug 2024 peak (JPY 47,956/t).

A 20,000 tonnes (t) H2 cargo was awarded to a Chattogram-based mill at JPY 46,771/t FAS, translating to around $305/t FOB Japan and approximately $345-350/t CFR. Compared with the previous month, the increase in dollar terms was limited to about $6/t, as a weaker Japanese JPY (slipping from around 156.7/$ in December to 157.2/$ in early January) supported higher export offer levels despite modest underlying price gains.

Commenting on the outcome, Chairman Minami Koji said the final price exceeded expectations, citing a weaker yen, lower freight costs, and improving buying interest from Southeast and South Asia as key factors.

All 15 trading companies participated, submitting a total of 125,900 t in bids, up 20,000 t m-o-m and marking the 13th consecutive month with bids exceeding 100,000 t.

Scrap prices in the Kanto region remained stable for the second consecutive month, as softer demand from export markets continued to cap upward momentum.

Tokyo Steel revised scrap purchase prices on 8 January, its first update of the year, keeping prices unchanged across most plants, lowering Kansai to JPY 43,500/t, and continuing to suspend revisions at Takamatsu, which remains at JPY 39,500/t.

Japan scrap export market

BigMint assessed Japan’s H2 scrap at JPY 43,550/t ($279/t) FOB Tokyo Bay, down by JPY 750/t w-o-w, due to competitive offers and weak buying interest.

H2 scrap offers to Vietnam slipped to $325-330/t CFR, with tradable levels around $318-320/t CFR, as mills remained well stocked and waited for the Kanto tender outcome. Deep-sea scrap markets saw thin liquidity due to a wide bid-offer gap, limiting spot activity despite slightly firmer assessments.

Muted US scrap exports

The US ferrous scrap export market saw muted activity in the first full week after the year-end holidays, with limited transactions reported. A couple of cargo sales from US to Turkiye emerged at around $371-372/t CFR, while trading remained largely quiet. Tightened shredded scrap availability narrowed the price gap with HMS. Meanwhile, easing freight rates contrasted with currency pressures and flat Turkish finished steel markets, keeping overall sentiment cautious.

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $347/t, up by $3/t w-o-w.

- Shredded – $367/t, up by $3/t w-o-w.

US-origin HMS 80:20, bulk – CFR assessments

- Turkiye – up by $1/t w-o-w at $371/t.

- Vietnam – stable w-o-w at $345/t.

- Bangladesh – up by $1/t w-o-w at $362/t

Outlook

Looking ahead, the association is scheduled to complete shipments for the December contract (15,000 t) between 13-23 January, while the next export tender for February delivery is planned for 10 February. Japanese H2 scrap prices may remain under pressure as buyers, especially Vietnamese mills, delay restocking due to high inventories. While US scrap exports remain muted, tight shredded supply and currency factors offer limited price support.

Leave a Reply