- Ongoing enquiries offer support, but ample tonnage caps upside

- Panamax rates see selective gains; Supramax stays under pressure

Coal freights across major import routes showed mixed movements, driven by subdued cargo enquiries and abundant vessel availability. While charterers were active and some fixing took place, abundant prompt tonnage and cautious early-year buying by Indian importers kept overall upward momentum muted. Falling bunker prices and softer FFAs further reinforced a cautious sentiment, preventing a meaningful recovery in spot rates.

Across major routes — Australia-India, South Africa-India, and Indonesia-India — shipowners faced sustained competition due to comfortable vessel supply. Although fixtures were concluded, charterers retained strong negotiating leverage, resulting in largely stable to slightly weaker freights. Market participants noted that cargo urgency remained limited, with buyers fixing only nearby requirements rather than advancing cargo programmes.

Panamax routes from Australia and South Africa saw marginal support from selective fixtures, but gains remained modest and route-specific rather than sentiment-driven. In contrast, Supramax freights from Indonesia declined, as muted cargo volumes and an oversupply of open tonnage restricted recovery prospects.

On the cost side, falling bunker prices and weaker forward freight agreements (FFAs) reinforced the bearish sentiment. Lower voyage costs reduced owners’ resistance to rate concessions, while soft paper markets dampened expectations of a near-term rebound.

The market’s subdued tone reflects a combination of low early-year demand, comfortable coal inventories in India, and abundant vessel supply. Falling bunker prices provided limited relief by reducing voyage costs, but softer FFAs reinforced bearish sentiment, leaving owners with little leverage to push rates higher.

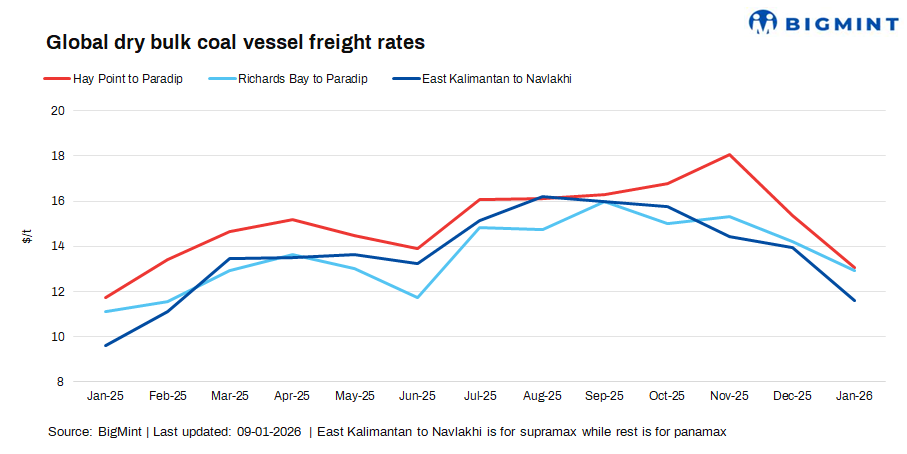

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights edged up by $0.4/dmt w-o-w to $13.25/dmt, driven mainly by isolated fixture activity rather than broad market strength.

- South Africa (Richards Bay)-India (Paradip), Panamax: Rates rose by $0.3/dmt w-o-w to $12.76/dmt, reflecting selective cargoes, though overall market momentum remained weak.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Rates declined by $1.8/dmt w-o-w to $11.01/dmt due to muted cargo enquiries and ample open tonnage, keeping the market under pressure.

Outlook

Coal freight sentiment is expected to remain stable to mildly bearish in the near term, as ample vessel availability continues to offset the presence of cargo enquiries and fixtures. While ongoing fixing activity should prevent a sharp downside, cautious buying behaviour by Indian importers and limited cargo urgency are likely to cap any meaningful rate recovery across both Panamax and Supramax segments.

A sustained improvement in freights will depend on a clearer pick-up in coal imports from the power and steel sectors, alongside tighter vessel supply. Until then, falling bunker costs and soft FFAs are expected to keep owners flexible on pricing, with spot rates likely to remain under pressure in the coming weeks.

Leave a Reply