- India reduces Indonesian imports by 16% y-o-y; Polish exports dip 1%

- Govt imposes anti-dumping duty after quantitative restrictions expire

- Indonesian prices still at par with domestic ones despite $83/t duty

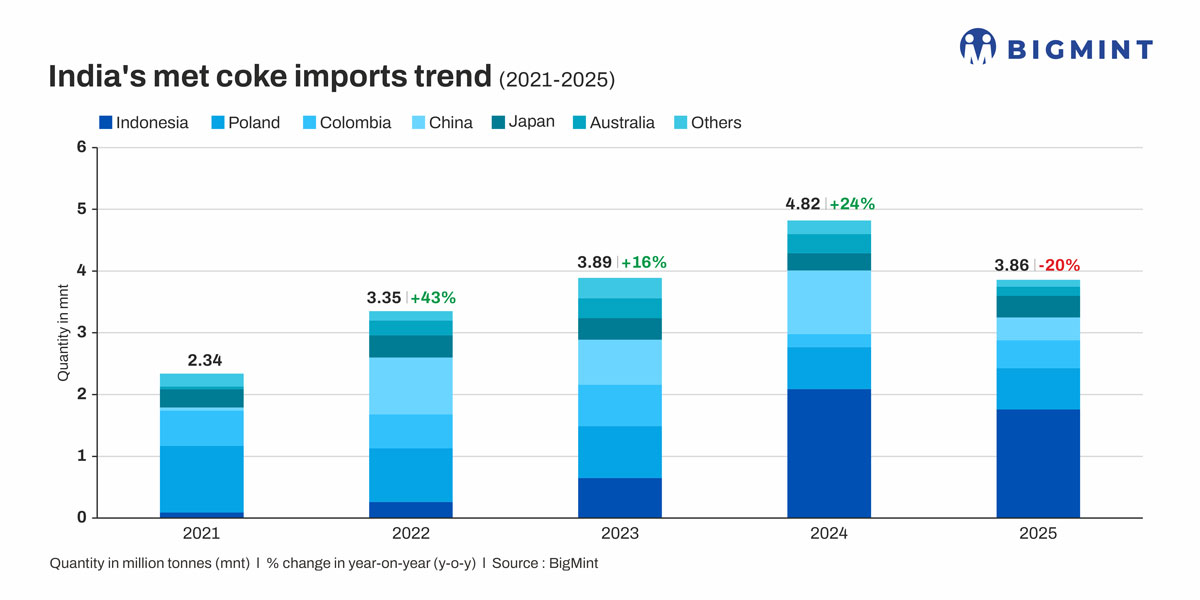

Morning Brief: India’s metallurgical (met) coke imports fell 20% y-o-y to 3.9 million tonnes (mnt) in CY’25, according to provisional data. Quantitative restrictions on the imports of low-ash met (LAM) coke were the primary factor contributing to the sharp drop in volumes.

Country-wise import sources

Mixed trends emerged in terms of country-wise imports rather than across-the-board decline.

Indonesia was the largest supplier in CY’25 at 1.76 mnt, with a fall of 16% y-o-y. Similarly, imports from Poland declined by 1% to 0.67 mnt. Conversely, shipments from Colombia more than doubled to 0.45 mnt against 0.21 mnt, while imports from Japan increased by 25% 0.35 mnt.

Imports from “Others”, that is, miscellaneous smaller suppliers, fell by 60% y-o-y to 0.63 mnt.

Leading importers

AM/NS India was the largest importer at 1.08 mnt, with intake declining 21% y-o-y. Tata Steel reduced its imports by 52% to 0.31 mnt and JSW Steel by 34% to 0.25 mnt.

Factors influencing India’s met coke imports in CY’25

Govt imposes import restrictions on LAM coke: In December 2024, the Indian government imposed quantitative restrictions on imported met coke with ash content less than 18%. Domestic met coke manufacturers had alleged that LAM coke imports, especially from Indonesia, had eroded their profits and forced them to reduce capacity utilisation rates due to the wide price gap with domestic material.

To illustrate, in FY’25, India’s merchant met coke industry had an installed capacity of about 8 mnt, while actual production was much lower at around 4 mnt. Moreover, considering prices recorded on 8 January 2026, Indonesian met coke stood at $235/tonne (t) CFR India compared to domestic blast furnace-grade material at INR 32,200/t ($358/t) exy-Jajpur.

While these import curbs were initially for six months till the end of June, they were later extended till 31 December. Quarterly allocations stood at 713,583 t, with the full-year volume at 2.85 mnt.

Following the expiry of these restrictions, the Indian government imposed a provisional anti-dumping duty on LAM coke imports for six months, aimed at protecting domestic producers from low-priced overseas supplies.

The duty will range between $60.87/t and $130.6/t, depending on the country of origin, and will apply to imports from China, Indonesia, Colombia, Japan, and Russia.

At the same time, the Indian government withdrew import restrictions on low-ash metallurgical coke, making imports freely permissible with immediate effect.

Met coke production rises, coking coal imports rise: India’s met coke production increased by 8% y-o-y to 51 mnt, as per provisional data maintained with BigMint. India also increased its imports of coking coal by 10% to 62.6 mnt. This suggests that met coke producers ramped up operations to capture increased demand due to limited imports. Parallelly, rising procurement of coking coal also comes in response to expanding coke-making capacities of steelmakers.

Outlook

Met coke imports are expected to decline following the imposition of the anti-dumping duty, with smaller players likely to shift to sourcing domestic material rather than imports.

However, a major decrease may not occur, and a potential increase cannot be completely ruled out. The landed cost of Indonesian met coke, taking into account the anti-dumping duty of $82.75/t, comes to INR 30,250/t CFR India excluding freight charges. In comparison, domestic met coke is at INR 32,200/t exy-Jajpur and INR 30,100/t exy-Gandhidham.

Therefore, Indonesian imports may continue given their price viability, with larger mills turning to these. Met coke from other countries, however, will turn uncompetitive due to higher prices.

If imports slow down, the capacity utilisation of domestic met coke producers is expected to increase. Coking coal imports will rise in conjunction, although high prices may curtail demand and may shift focus to imported met coke again.

Notably, Synergy Capital has taken over Saurashtra Fuels and has started met coke production for the merchant market in western India. The restart of coke production at Synergy Saurashtra may contribute to reducing India’s import dependence.

Domestic met coke prices are expected to continue increasing in the first half of January, supported by higher pig iron and coking coal prices. Prices will also gain support from the recovery in steel demand in India that is generally seen in Q1. However, if imports pick up, prices may slide.

Leave a Reply