- India remains ~85% import-dependent on scrap

- Imports likely to maintain upward trajectory in Q1CY’26

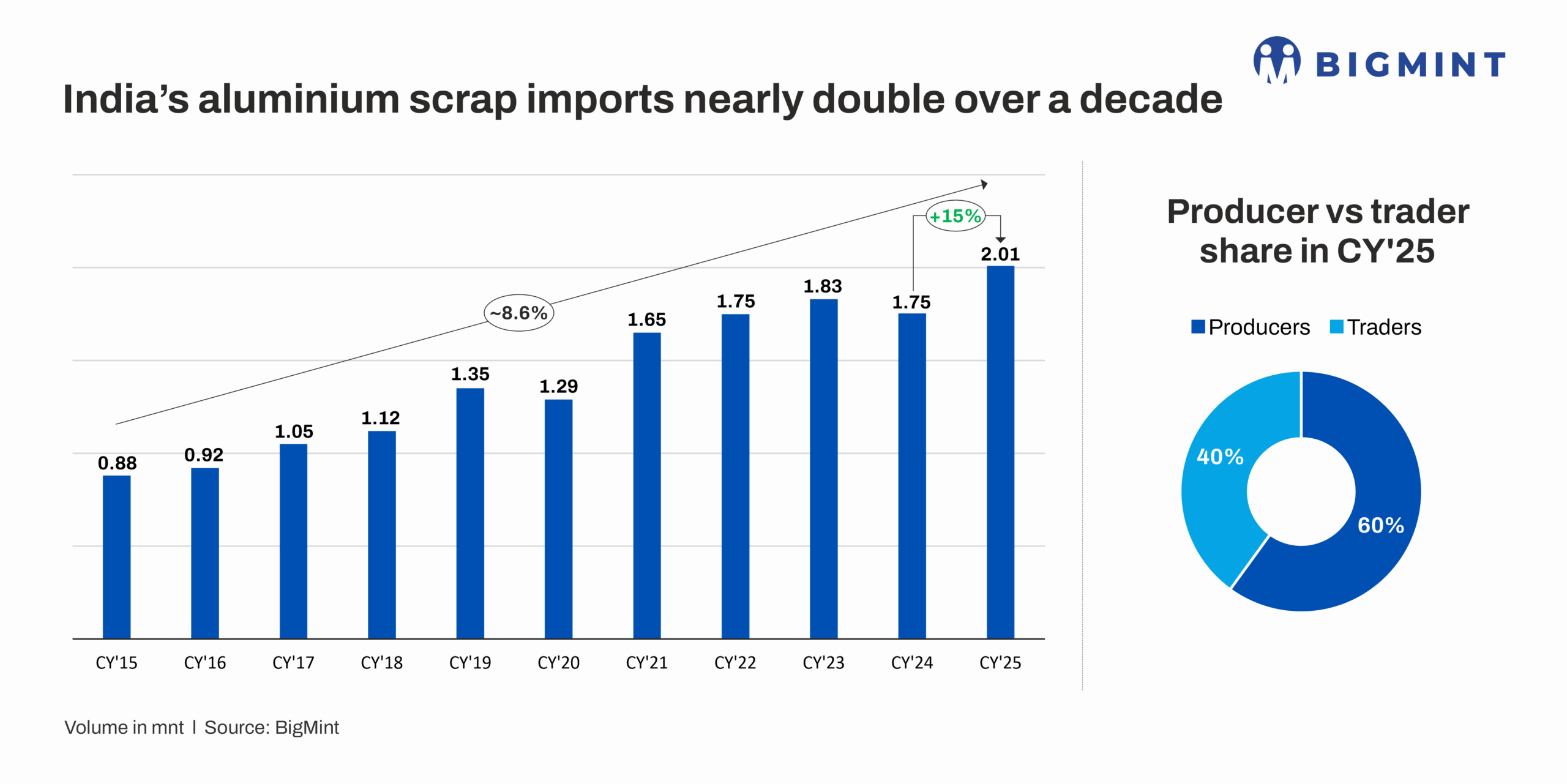

India’s aluminium scrap imports have more than doubled over the past decade, reaching a record level of around 2 mnt in 2025, highlighting the country’s increasing reliance on scrap to support secondary aluminium and alloy production.

Historically, India has lagged other major economies in aluminium consumption, resulting in limited domestic scrap generation. As aluminium use expanded across automotive, infrastructure, and electrical sectors, scrap availability failed to keep pace, driving greater reliance on imports. In 2015, aluminium scrap imports stood at around 0.8 mnt, marking the early stage of this structural shift, which has since accelerated with the growth of secondary aluminium and alloy production.

On a y-o-y basis, aluminium scrap imports are expected to rise by around 15% in CY’25, reaching 2 mnt from 1.75 mnt in the previous year. This growth reflects a combination of market resilience and urgency, driven primarily by global supply realignments and persistent domestic scrap shortages. The increase comes amid heightened volatility in international markets, exacerbated by recent US tariff actions and tightening global scrap availability.

The shift in trade flows began early in the year when the US–traditionally India’s largest scrap supplier–significantly curtailed outbound shipments following tariff hikes and stronger domestic demand. This sudden contraction created a supply gap for Indian buyers, prompting a strategic pivot toward alternative sourcing from the UK, UAE, Saudi Arabia, Australia, and several EU countries. Despite this diversification, supply constraints have persisted, pushing Indian manufacturers to maintain aggressive import strategies to secure raw material.

Grade-wise imports

The majority of the aluminium scrap grades are expected to see an increase in arrival in CY’25 despite volatility in prices. This was majorly due to the rise in demand particularly in the backdrop of shortage of scrap and reduced supply from the US in the early months of 2025.

Country-wise imports

The country-wise breakdown of imports highlights a clear rebalancing of sourcing strategies. US scrap shipments declined sharply following the tariff regime introduced by President Trump–initially a 25% duty, later raised to 50% from 4 June 2025–which significantly altered trade flows. With finished aluminium imports falling, US smelters increased domestic scrap absorption and stepped up scrap imports, reducing availability for export markets.

As a result, India redirected its scrap procurement toward alternative sources, including the UK, Saudi Arabia, the UAE, Australia, and several smaller countries. Regionally, Europe–including the UK–is expected to emerge as the largest supplier in CY’25, with combined exports of 0.56 mnt, representing a 13% y-o-y increase and accounting for nearly 30% of India’s total aluminium scrap imports.

Domestic shortages reinforce import reliance

Within India, structural limitations in scrap collection have continued to hinder supply growth. The domestic market struggles with insufficient collection networks, low recycling efficiency and limited inflows of post-consumer scrap. These constraints become particularly evident when demand surges from alloy producers, especially those manufacturing ADC12–a critical grade for the automotive sector.

The shortage of both domestic and imported scrap led to firm prices across regions. Smelters in northern and southern India reported consistent supply tightness, prompting deeper dependence on the overseas markets to meet monthly requirements. The challenge was further aggravated by declining ADC12 imports due to certification hurdles.

Despite strong demand, India is expected to witnessed a 44% drop in ADC12 ingot imports, which fell to 12,539 t in CY’25 from 22,431 t in CY’24. This reduction was not driven by weak consumption but by regulatory barriers. Ongoing BIS certification issues prevented Indian buyers from sourcing material from Malaysia–the country’s largest ADC12 supplier–despite a Free Trade Agreement with that country.

This disruption forced manufacturers to rely even more heavily on raw scrap which further amplified import requirements of available grades.

Strong demand

One of the biggest drivers of the surge in imports was the sustained rise in consumption by secondary smelters, rolling mills and die-casting units. Expansion in automotive, foundry, electrical, and packaging sectors kept demand stable throughout the year. With producers operating at higher utilisation rates, imported scrap remained essential to ensuring consistent raw material availability.

Additionally, India’s secondary aluminium industry continued to scale up, pushing manufacturers to secure larger volumes of raw materials.

Price trends

Aluminium prices on the LME increased by $178/t y-o-y in CY’25 reaching $ 2,635/t from $2,457/t. Meanwhile, stocks on LME saw a 37% drop in CY’25 settling at 0.48 mnt as against 0.76 mnt.

Aligning with the rise in LME aluminium prices, imported as well as domestic scrap prices witnessed an increase y-o-y in CY’25. As per BigMint’s assessment, major grades like US tense (6-7%) stood at $1,960/t CFR West Coast India, reflecting a 5% increase y-o-y from $1,865/t in CY’24.

Domestic tense scrap prices rose 10% climbing to INR 191,044/t from INR 174,252/t ex-Delhi. Chennai mirrored this uptrend, posting an 7% increase. Despite the rise in domestic prices, buyers continued to favour imported scrap as landed cost remained more competitive–lower by INR 4,000-5,000/t. This price advantage supported higher arrivals of imported material during CY’25.

What lies ahead for India?

India’s aluminium scrap imports are expected to maintain an upward trajectory over the upcoming few months die to domestic scrap shortages. However, the outlook beyond 2025 introduces new challenges that could reshape supply chains.

The EU-27 is preparing to implement scrap export restrictions by spring 2026 to address leakage–an action that could significantly reduce availability for global buyers. Several Middle Eastern countries are also evaluating similar restrictions. Notably, India’s second largest supplier after the US is the EU-27, which accounted for nearly 30% of India’s imports in CY’25.

Policies for ramping up India’s demand & domestic scrap generation

India remains around 85% import-dependent for aluminium scrap and faces increasing obligations under the new EPR norms for non-ferrous metals. Without accelerated reforms in domestic scrap collection and the formalisation of recycling infrastructure, the country risks greater exposure to the uncertainties of global markets. Additionally, aluminium scrap imports are currently subject to a 2.5% basic customs duty (BCD), while the previous budget reduced duties on other non-ferrous metal scrap to zero. The domestic recycling industry has been advocating for a similar removal of the duty on aluminium scrap to support local recycling and reduce import reliance.

Leave a Reply