- Improved logistics operations support higher trade activity

- Pellet prices fall by up to INR 400/t m-o-m across India in Dec

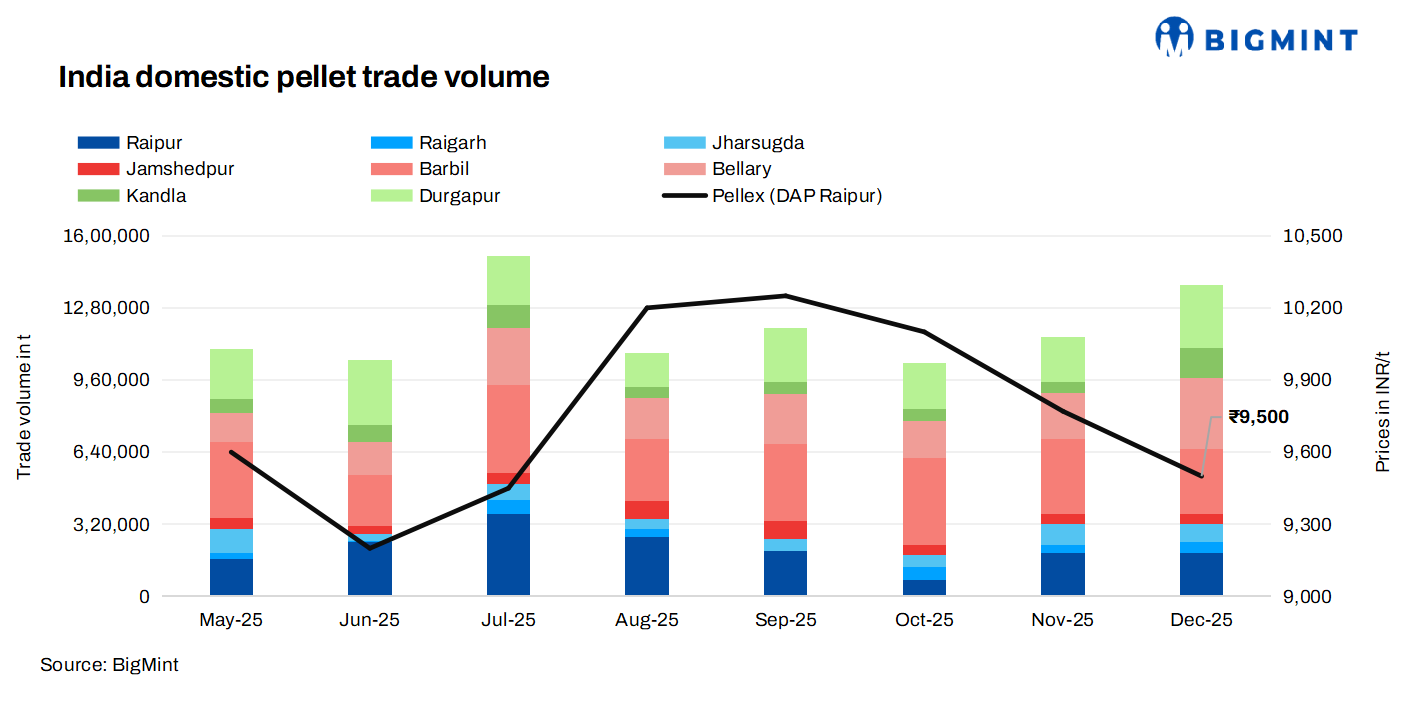

India’s domestic pellet trade surged by around 25% m-o-m in December 2025 to 1.74 million tonnes (mnt) compared to 1.39 mnt in November, supported by improved steel production and better logistics movement.

India’s crude steel production increased by 3.2% m-o-m to 14.147 mnt in December, compared with 13.713 mnt in November. On a y-o-y basis, output rose 5.4% from 13.429 mnt in December 2024.

Meanwhile, BigMint recorded primary trades of approximately 16.33 mnt in the Indian domestic market in CY’25.

Key consuming and trading regions such as Bellary, Durgapur, Jamshedpur, and Kandla registered a notable increase in trade activity due to firm demand from steelmakers. Participants highlighted that steel mills ramped up production in December, leading to higher procurement of raw materials, particularly pellets, to ensure operational continuity.

However, the Barbil and Raipur regions witnessed a marginal decline in trade volumes compared to November. Sources attributed this to cautious buying by some buyers due to price volatility and inventory adjustments at select plants.

Market updates

A pellet producer stated, “The demand scenario was much better in December as steel production picked up momentum, which directly supported pellet offtake.” Improved rake availability and smoother rail movement further facilitated higher trade volumes, easing transportation constraints that were observed in the previous month.

Market participants also noted that firm prices of semi-finished steel products, including sponge iron and billets, provided additional support to pellet trades during the month. Another producer said, “The stability in semi-finished prices encouraged buyers to remain active, while a few long-term bulk contracts also added to the overall traded volume.”

Meanwhile, the commissioning of new pellet capacities also contributed to market activity. New plants in CG Raipur and the RPC Group plant in the Bellary region entered the market with fresh offers, adding liquidity to regional trades.

In Q4CY’25, finished steel production in India reached 39.5 mnt, while domestic consumption was higher at 40.7 mnt, indicating that demand exceeded production during the quarter.

Meanwhile, India’s pellet import volumes increased to around 0.22 mnt in December, compared to 0.07 mnt in November. Kandla and Chennai-based buyers largely booked imports, while most consumers relied on domestic supply due to its competitiveness compared to overseas-origin material.

Factors driving India’s pellet market in Dec’25

- Bids remain firm in OMC’s Dec auction: In OMC’s iron ore fines auction for 2.22 mnt (Fe 51-62%) on 19 Dec’25, around 2.14 mnt (97%) were booked at INR 2,500-6,000/t. The lots received premiums ranging within INR 50-1,100/t, with INR 750/t being the average premium over base prices. Bids (weighted average) remained stable m-o-m.

- PELLEX decreases m-o-m: The monthly average domestic pellet index, PELLEX, dropped INR 275/t m-o-m in December to INR 9,500/t DAP Raipur. Pellet prices were lower m-o-m due to a decline in sponge iron prices in mid-December. In the other regions, pellet prices dropped INR 50-400/t m-o-m in December due to attract sponge iron manufacturers, some of whom have shifted to DRCLO as a raw material.

- Sponge PDRI prices rise m-o-m: The Indian sponge iron market in December witnessed a gradual improvement in sentiment, though overall trade activity remained measured and region-specific. India sponge iron prices increased by INR 900-2,100/t ($10-23/t) m-o-m, supported by a modest revival in buying interest.

- NMDC rake movements rise m-o-m: NMDC dispatched 619 rakes from its Chhattisgarh mines in December, equivalent to 2.38 million tonnes (mnt) of iron ore. This is an uptick of 15% compared to 538 rakes (2.07 mnt) in November, as per BigMint data. On a y-o-y basis, December dispatches rose by 20% compared with 515 rakes in December 2024.

Outlook

Pellet trade volumes are expected to remain at around December’s levels in January. Buyers are likely to adopt a cautious approach amid mixed steel market sentiments, while steady operational demand is expected to prevent any sharp decline in volumes.

Leave a Reply