- Brazil and Asian flows offset declines from Australia, Atlantic exporters

- Soft post-holiday freights keep long-haul shipments under pressure

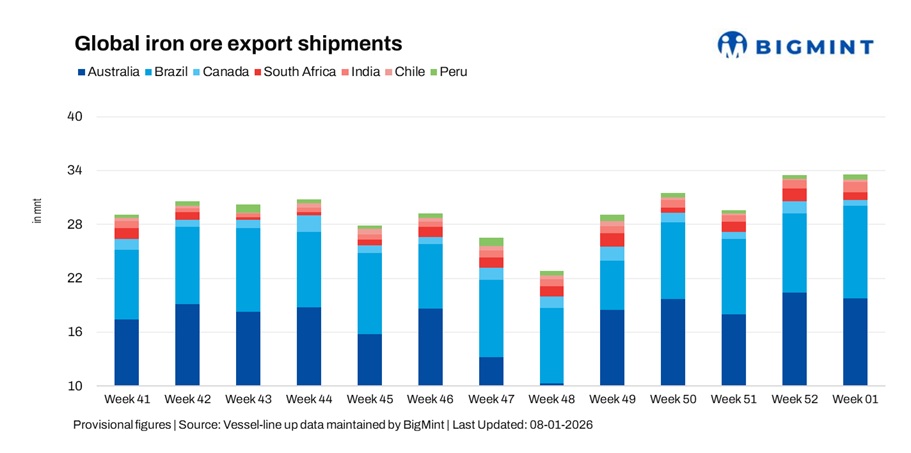

Global seaborne iron ore exports edged up 0.6% w-o-w to 33.7 million tonnes (mnt) in week 1 (27 December-2 January), compared with 33.5 mnt in week 52, according to BigMint’s vessel line-up data. The marginal increase was underpinned by stronger shipments from Brazil, India, Chile, and Peru, which offset lower exports from Australia, Canada, and South Africa, keeping overall volumes broadly stable.

The week’s performance reflected cargo realignment following the holiday period rather than a recovery in freight fundamentals. While underlying trade flows remained steady, the absence of fresh cargo enquiries and cautious chartering behaviour limited fixing activity, resulting in uneven shipment trends across regions. Short-haul and regionally competitive exporters managed to sustain volumes, whereas long-haul Atlantic suppliers faced greater headwinds from softer freight sentiment.

Country-wise trends

Australian exports dip as holiday impact lingers

Australia’s iron ore exports declined 3% w-o-w to 19.8 mnt in week 1, down from 20.4 mnt in week 52, as year-end volumes tapered and holiday-related scheduling disruptions lingered at key Western Australian ports. Port Hedland remained the dominant loading hub with 11.49 mnt, followed by Walcott (4.13 mnt) and Dampier (3.48 mnt), though overall volumes softened as deferred late-December shipments had largely been cleared in the previous week.

On the supply side, Rio Tinto led shipments with 7.61 mnt, followed by BHP (6.04 mnt) and FMG (3.97 mnt), reflecting disciplined export strategies among major miners. China remained the primary destination, importing 15.6 mnt, while South Korea and Japan received 1.79 mnt and 1.31 mnt, respectively.

Despite Australia’s continued structural advantages with respect to Asia, including shorter voyage distances and strong operational reliability, cautious Capesize sentiment and thin post-holiday fixing limited further upside. As a result, exporters maintained controlled shipment flows rather than pushing additional volumes.

Brazil emerges as key swing supplier amid soft freight

Brazil’s iron ore exports rose 16.8% w-o-w to 10.3 mnt in week 1, up from 8.8 mnt in week 52, marking one of the strongest weekly recoveries among major suppliers. The increase was driven by improved vessel positioning and the release of previously deferred cargoes from key load ports, led by Ponta da Madeira (3.03 mnt), followed by Itaguai (2.79 mnt) and Tubarao (2.07 mnt).On the supply side, CSN emerged as the leading shipper with 4.86 mnt, closely followed by Vale (4.07 mnt), reflecting balanced contributions from Brazil’s major producers.

China remained the dominant destination, importing 5.35 mnt, while the Philippines and South Korea each received 0.48 mnt, highlighting selective Asian demand. While long-haul freight sentiment remained soft, Brazilian exporters benefited from selective fixing and stable cargo availability, allowing volumes to recover despite price-sensitive chartering.

The export recovery also aligns with Brazil’s broader export performance, after the country achieved a record annual iron ore shipment in 2025 surpassing 400 mnt for the first time on the back of higher production and resilient demand from China.

South African exports retreat after prior rebound

South Africa’s iron ore exports declined 36.2% w-o-w to 0.9 mnt in week 1, reversing part of the sharp recovery recorded in week 52. The pullback reflected the completion of deferred shipments loaded earlier in December, alongside restrained long-haul fixing interest amid subdued freight sentiment during the holiday period.

Saldanha Bay remained the primary loading port with 0.66 mnt, followed by Richards Bay at 0.27 mnt. Export flows to both Europe and Asia softened as charterers adopted a wait-and-see approach, limiting fresh cargo commitments. China and Japan were the leading destinations, each importing 0.17 mnt during the week.

Despite the week 1 decline, South Africa’s iron ore exports showed resilience in 2025, with volumes holding broadly steady y-o-y and China remaining the largest importer, even as long-standing rail and port infrastructure constraints continue to shape export timing and flow dynamics.

Canadian shipments slide on softer Atlantic demand

Canada’s iron ore shipments declined 56.5% w-o-w to 0.6 mnt in week 1, down from 1.4 mnt last week, as Atlantic demand softened and cargo nominations eased following the late-December rebound. Loadings slowed at Sept-Iles (0.25 mnt) and Port Cartier (0.37 mnt), reflecting cautious chartering behaviour and thinner post-holiday scheduling.

On the supply side, AMNS emerged as the leading shipper with 0.37 mnt, followed by Guinea and Nimba Mines (0.18 mnt). France remained the primary destination importing 0.15 mnt, underscoring continued but selective European demand amid subdued Atlantic market conditions.

Exports remained highly sensitive to long-haul freight economics, with muted fixing activity preventing a sustained recovery in volumes despite stable port operations across Canada’s key export terminals. Looking ahead, developments such as the confirmation of high-grade iron ore potential at Canada’s North Wind project in Labrador and projections for increased national iron ore output in 2026 suggest structural support for Canadian export capacity, even as weekly volumes remain sensitive to Atlantic demand and freight dynamics.

Indian iron ore exports rise on east coast support

India’s iron ore exports increased by 19.6% w-o-w to 1.1 mnt, supported by improved loadings from east coast ports such as Paradip (0.47 mnt), Dhamra (0.23 mnt), and Mormugao (0.21 mnt). Comfortable Supramax availability and relatively competitive regional freight conditions helped sustain shipment flows, even as overall chartering activity remained selective.

China continued to absorb the bulk of Indian exports at 0.29 mnt, reinforcing India’s role as a short-haul supplier during periods of subdued global freight sentiment. Data shows India’s iron ore and pellet exports were down significantly y-o-y in 2025 as rising domestic steel demand absorbed volumes despite a rebound in shipments towards the end of the year, highlighting structural shifts that are likely to shape export flows in early 2026.

Chilean iron ore exports rebound from low base

Chile’s iron ore exports rose 57.9% w-o-w to 0.3 mnt in week 1, driven primarily by the movement of small, previously delayed cargoes. Loadings were concentrated at Caldera (0.17 mnt) and Totoralillo (0.15 mnt), reflecting limited but improved port activity during the week.

Despite the sharp percentage increase, absolute volumes remained modest, constrained by selective fixing and limited cargo availability. China remained the sole major destination, importing 0.32 mnt, underscoring Chile’s continued role as a niche Pacific supplier with shipment flows highly dependent on timing and vessel positioning rather than broader market momentum.

Peruvian iron ore flows improve amid selective fixing

Peru’s iron ore exports increased by 71.4% w-o-w to 0.6 mnt, supported by the release of previously delayed cargoes following subdued activity in late December. San Nicolas dominated loadings with 0.49 mnt, while Matarani contributed 0.12 mnt, highlighting concentrated shipment flows from Peru’s key export terminals.

On the supply side, Shougang Hierro accounted for the bulk of shipments with 0.49 mnt. China remained the primary destination, importing 0.58 mnt, though overall export momentum stayed limited on selective fixing and cautious chartering. As with Chile, Peru’s shipment performance remained highly sensitive to cargo timing and vessel availability rather than a broader improvement in market conditions.

Freight weakness reinforces uneven iron ore shipments

Iron ore freight markets weakened further during the week as year-end and New Year holidays curtailed fixture activity, leaving charterers largely inactive while shipowners competed for a limited pool of cargoes amid ample tonnage availability.

Subdued steel production indicators from China weighed on near-term demand sentiment, reducing cargo urgency and reinforcing a cautious, wait-and-watch approach among market participants.

As a result, a softer freight environment favoured short-haul and opportunistic movements while constraining long-haul shipment economics, contributing to uneven export performance across major iron ore origins during week 1.

Outlook

Global iron ore shipments are expected to remain rangebound in the near term, with volumes stabilising rather than accelerating as markets emerge from the holiday period. A gradual resumption of chartering activity and the return of deferred cargo programmes are likely to support shipment flows, particularly from Australia and Brazil, although ample vessel availability may limit the pace of any recovery. Until freight sentiment improves meaningfully and visibility on Chinese steel demand strengthens, iron ore export momentum is expected to remain uneven across regions in January.

Leave a Reply