- Fe64%, low-alumina iron ore suitable for BF trials

- Move assumes significance ahead of impending lease expiries in CY’30

Tata Steel has brought a trial shipment of iron ore from its Canadian arm, Tata Steel Minerals Canada (TSMC), to India as part of its long-term raw material planning. The shipment includes iron ore lumps Fe 64% with 10-40 mm size range lumps, material typically suitable for blast furnace operations, according to market sources reported to BigMint.

The exercise is not about replacing domestic ore today, but about understanding how imported material behaves in Tata Steel’s system and how it can be blended with captive supply to optimise quality and value-in-use. It reflects early preparations for a future in which domestic sourcing may no longer fully cover internal requirements.

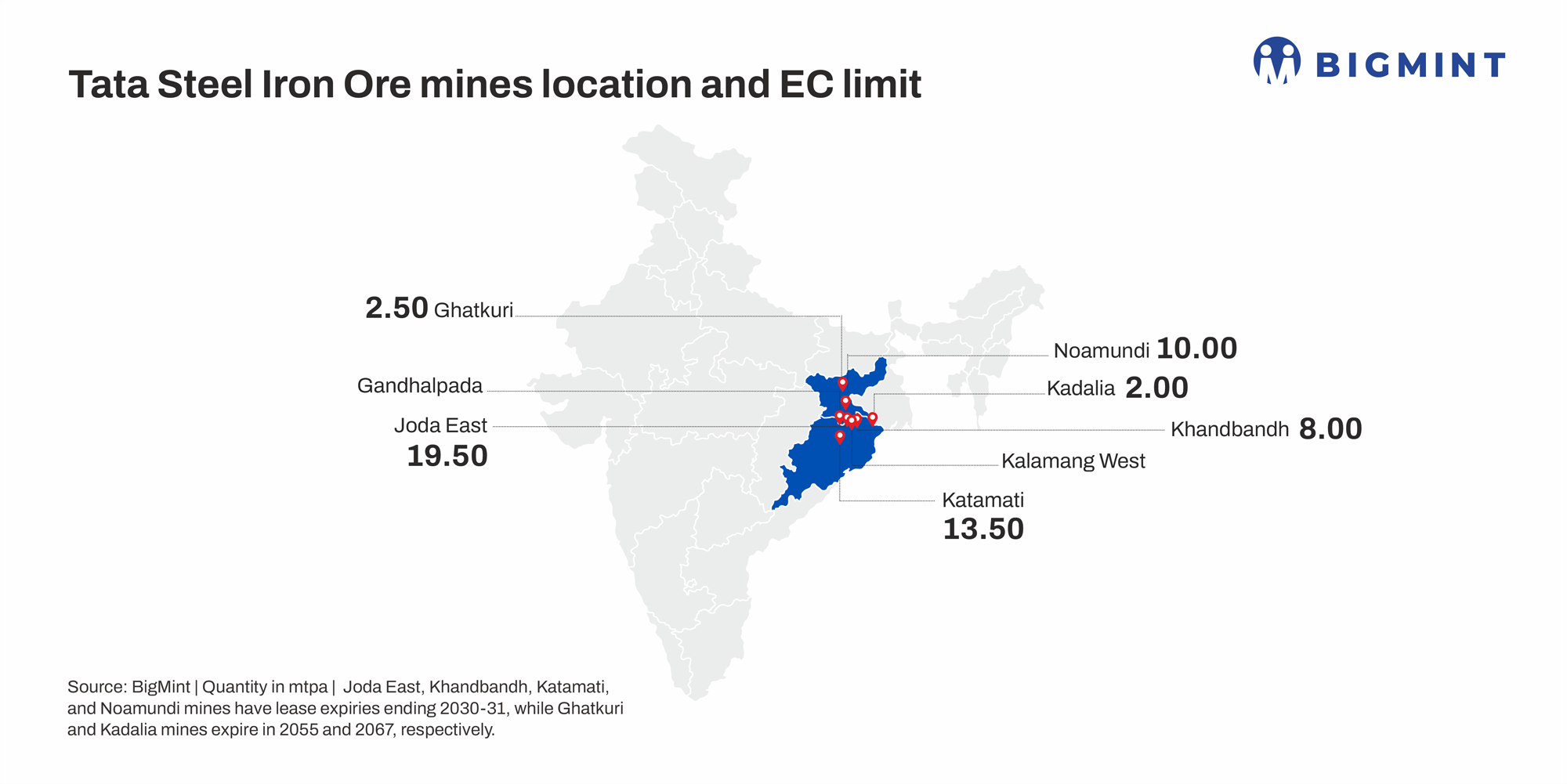

Currently, Tata Steel meets 100% of its iron ore requirement in India through six captive mines in Jharkhand and Odisha – Noamundi, Katamati, Joda East, Khandbandh, Vijaya II, and Koidahas. The company’s iron ore production stood at 19 mnt in H1CY’25.

As per mine-level approvals, Joda East has an EC capacity of 19.5 mnt/year, Khandbandh 8 mnt/year, Katamati 13.5 mnt/year and Noamundi 10 mnt/year, forming the bulk of Tata Steel’s captive supply base. However, the leases for Joda East, Khandbandh, Katamati and Noamundi expire in 2030-31, meaning a combined ~51 mnt/year of approved capacity faces renewal risk within the next five years.

In contrast, longer-dated assets such as Ghatkuri (Vijaya II) and Kadalia, with lease validity till 2055 and 2067 respectively, account for only ~4-5 mnt/year, insufficient to offset the scale of expiring capacity. Although Tata Steel has secured new auctioned blocks such as Kalamang West and Gandhalpada, these are yet to commence production.

From a market perspective, the move reflects more than just a one-off cargo. It signals how large integrated steelmakers are beginning to reassess raw-material security as a significant portion of captive capacity approaches expiry, especially when current production of ~22 mnt/year is concentrated in leases nearing their end of term.

From a market standpoint, the move underscores three emerging themes:

- Proactive risk management ahead of captive mine expiries affecting 50+ mnt/year of approved capacity.

- Rising emphasis on ore quality, particularly low-alumina, high-Fe material to sustain blast furnace productivity and operational efficiency.

- Gradual shift toward blended sourcing (domestic plus imports) among large integrated producers to manage volume risk and quality consistency.

Looking ahead, if peers follow similar strategies, India’s iron ore market could shift structurally. Higher reliance on premium seaborne lumps and fines would increase competition for high-grade material, tighten availability in export channels, and potentially support price differentials for quality.

Tata Steel’s trial does not imply near-term disruption, but it clearly signals how procurement strategies may evolve as post-2030 supply risks and cost pressures become more prominent.

Leave a Reply