- BF-grade met coke prices increased w-o-w on improved steel demand

- Market upside capped by AD duty uncertainty and weak foundry offtake

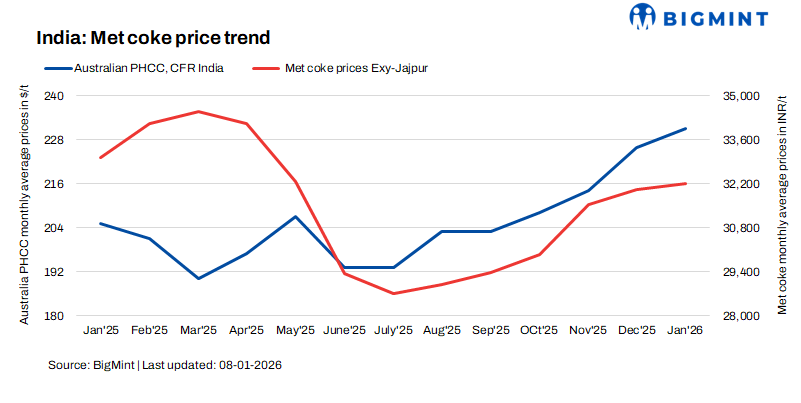

The Indian BF-grade metallurgical coke market recorded a week-on-week increase during the week ended 07 January 2026, supported by improved demand sentiment in key steelmaking regions.

BF-grade met coke (25-90 mm) prices in eastern India rose by INR 200/t to INR 32,200/t ex-Jajpur, while western India prices increased by INR 300/t to INR 30,100/t ex-Gandhidham. A few deals were also reported at INR 33,000/t exw Jajpur, following which offers have risen to INR 34,000/t exw Jajpur. Absence of import bookings, following landed cost of imports turning less viable, domestic offers have found support.

However, in western India sales pressure seems to have impacted prices.

Market sentiment remains cautious due to the anti-dumping (AD) duty on met coke imports. Participants noted slower market activity and limited spot transactions, with expectations that import bookings may resume in the second half of January 2026 once clarity improves.

Cost and global market signals mixed

On the cost front, Australian premium hard coking coal (PHCC) prices remained stable at $ 218/t FOB. Meanwhile, China’s domestic coke market continued to trade weak and steady, as steel mills maintained conservative procurement amid soft downstream demand. Although coking enterprises are operating under margin pressure and adjusting production flexibly, supply reductions continue to lag demand slowdown.

Pig iron prices in India surge on strong auction results

The pig iron market provided notable support, with steel-grade pig iron prices ex-Durgapur rising INR 1,900/t w-o-w to INR 36,500/t. The uptrend was reinforced by SAIL’s Rourkela Steel Plant auction on 05 January 2026, where 3,500 t of steel-grade pig iron was fully booked at an average of INR 38,100/t ex-works – up sharply by INR 4,350/t from the previous auction held on 18 December 2025.

Market outlook

We expect BF-grade met coke prices to increase marginally in the near term, supported by higher pig iron prices and selective steel demand. However, policy uncertainty, weak spot activity, and subdued foundry demand may limit further gains until import clarity and steel production improve later in January 2026.

Leave a Reply