- India: Containerised scrap demand soft, offers higher than expected

- Bangladesh: Bulk HMS bids lag offers, buyer interest remains weak

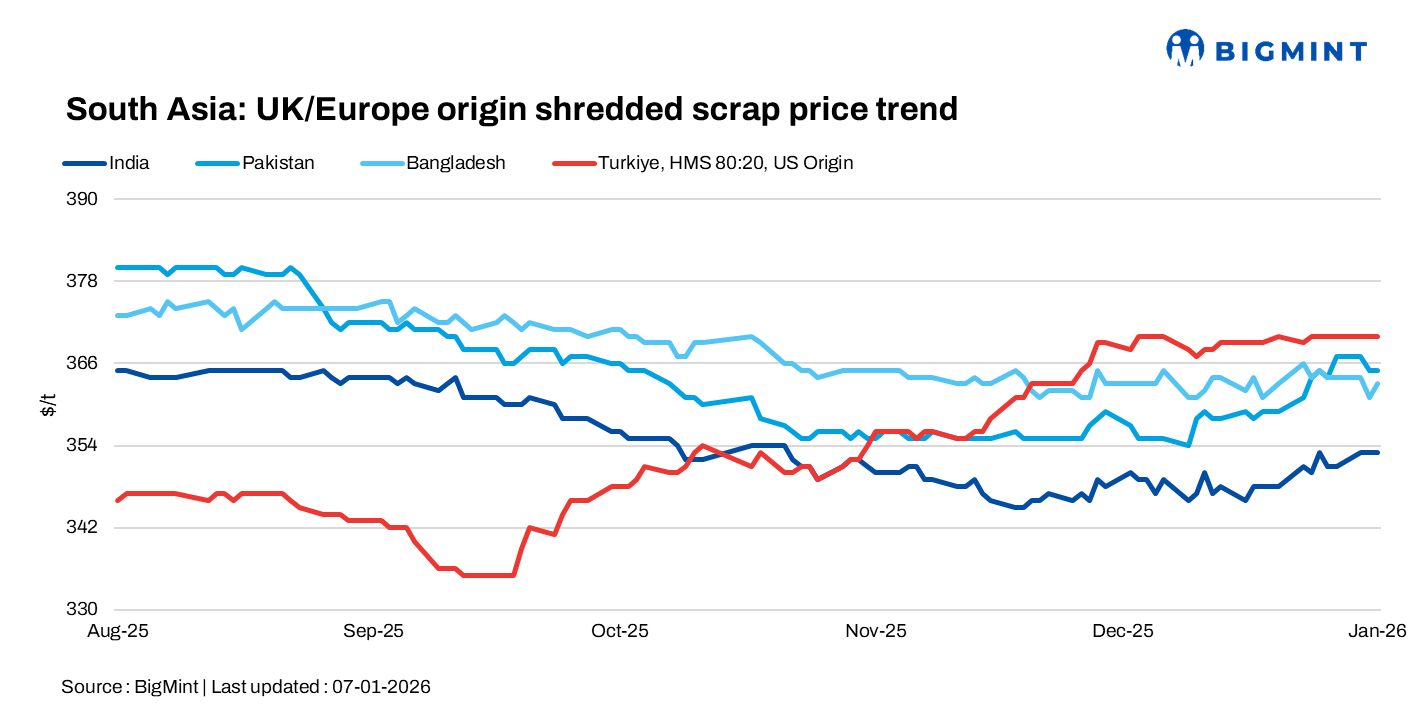

Imported scrap markets across South Asia remained largely subdued, with cautious buying, unworkable offers, and selective procurement prevailing. Weak demand in India, Pakistan, and Bangladesh contrasted with firm domestic steel prices, limiting fresh import activity.

India: India’s imported containerised scrap market remained quiet, as improving steel demand failed to translate into buying interest due to largely unworkable offer levels. A distressed lot of around 1,000 t HMS 60:40 from Costa Rica, affected by vessel damage, was offered at $310/t CFR after an $8/t discount for February delivery, but overall trade activity stayed limited.

Indicative offers into Mundra and Nhava Sheva included West African scrap at $345-348/t CFR, Dubai auto HMS at $325-330/t CFR, good-quality pure LMS at $310-315/t CFR, EU HMS 80:20 at $335-340/t CFR, and UK-origin shredded around $355/t CFR, with buyers remaining cautious and highly price-sensitive.

Pakistan: The imported scrap market remained muted, with buyers showing limited appetite for fresh purchases and focusing only on workable levels of around $362-364/t. Weak import interest contrasted with elevated domestic prices, as local scrap was indicated at around PKR 130,000/t, while billet and rebar prices hovered around PKR 184,000-185,000/t, keeping mills cautious as regards raw material bookings despite firm finished steel values.

Bangladesh: The scrap import market remained weak, with buyers showing limited appetite and highly selective procurement. A bulk cargo of 10,000 t HMS 80:20 from Singapore was offered at $355/t CFR Chattogram, while buyers attempted to close deals at around $351/t. Australian cargo indications of HMS 80:20 at $325-330/t, HMS 1 at $335-340/t, shredded at $358-360/t, and PNS at $362-365/t failed to generate buying interest.

Turkiye: Deep-sea imported scrap prices remained stable despite muted buying interest linked to weak rebar demand which, however, was balanced out by limited scrap availability and fewer seller offers. Tight margins on both sides kept activity subdued, but prices held stable, with US-origin HMS 80:20 indicated at around $370-372/t CFR.

Leave a Reply