- Ample supply, weak steel production to weigh on iron ore prices

- Traders hold on to iron ore stocks, avoid selling at lower prices

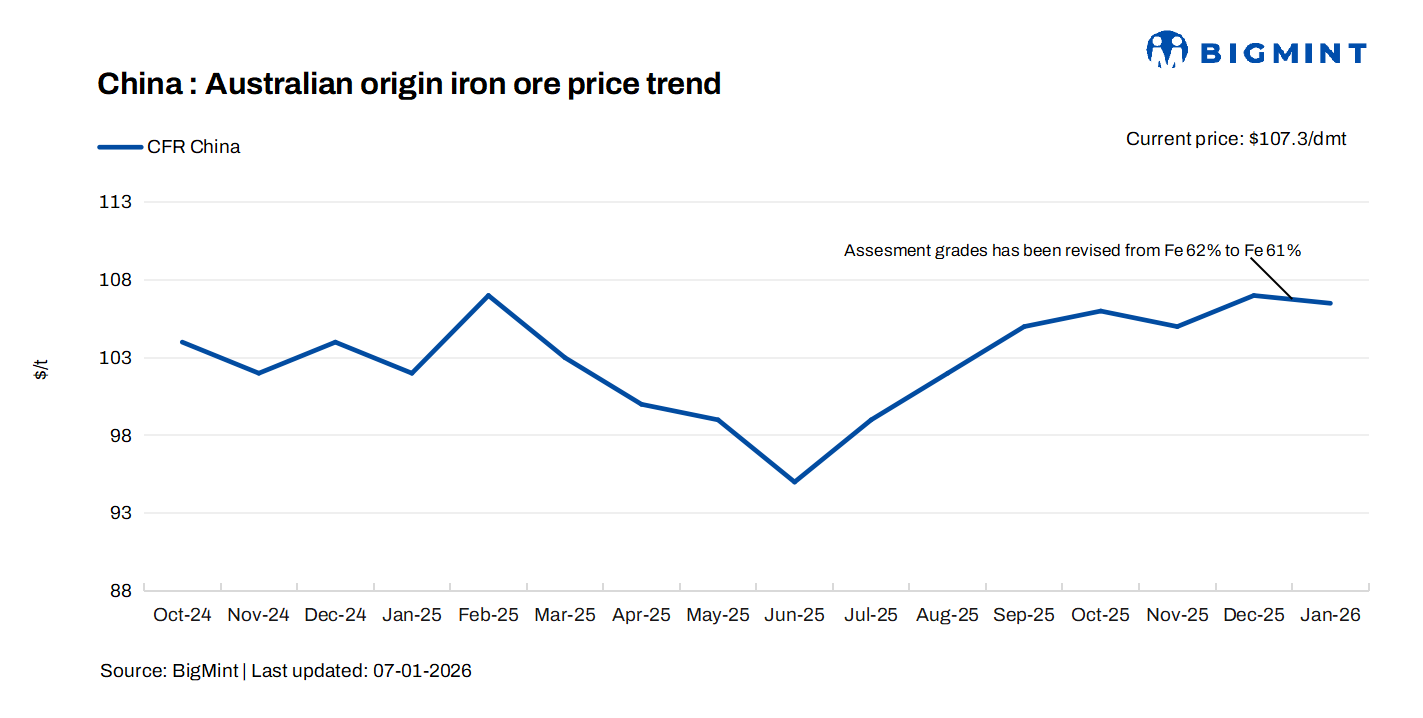

Mysteel: Prices of imported iron ore in China defied weakening fundamentals last month to edge higher, and this resilience is likely to persist into the new year, with prices expected to trade in a wider range in January, according to Mysteel’s latest monthly report on the commodity. Restocking activity ahead of the New Year holidays may support iron ore prices despite elevated port stocks and robust arrivals at Chinese ports.

In December, Mysteel’s SEADEX 62% Australian Fines index fluctuated within a narrow range of $103.7-106.95 CFR Qingdao, averaging $105.47/dmt, an increase of $1.71/dmt from November.

The slight uptick appeared counterintuitive, as iron ore’s market fundamentals actually softened last month, Mysteel Global notes. Port inventories continued to accumulate, signalling looser supply, while demand weakened as Chinese steel mills curtailed hot metal output during the winter lull.

Nevertheless, the strength of iron ore prices is justified. Besides the widespread market optimism about a demand recovery (as reported), traders patiently held onto their stocks instead of selling into declines.

Meanwhile, mills also increased forward purchasing in late December to secure sufficient iron ore ahead of the Chinese New Year holiday in February, the report noted. This provided further support that offset weaker fundamentals.

Looking ahead, iron ore prices are expected to remain under pressure this month, primarily due to abundant supply. While seaborne shipments from global miners may see a seasonal decline, arrivals of ore cargoes at Chinese ports will continue rising as a result of robust shipments in December.

Global iron ore shipments last month reached a record high of 156.2 million tonnes (mnt), according to Mysteel’s tracking data.

Consequently, China’s port stocks are anticipated to climb further this month. By 31 December, the stockpiles at the 45 major ports under Mysteel’s tracking had risen by 4.4% m-o-m or 7.4% y-o-y to 159.7 mnt, nearing a four-year high.

On the demand side, domestic blast-furnace (BF) steelmakers lack strong incentives to lift their production significantly. Many mills have halted their furnaces for year-end maintenance, and some may only resume operations after the Chinese New Year holiday (15-23 February), given the tepid steel demand amid cold weather-related construction slowdowns and the still-poor steel margins, the report suggested.

Consequently, any recovery in hot metal output is likely to be limited, which will also constrain the rebound in iron ore demand.

Throughout December, the combined hot metal production of the 247 Chinese BF steelmakers under Mysteel’s tracking averaged 2.29 mnt/day, down by 3% m-o-m. The daily average output in January will remain below 2.3 mnt/d, the report predicted.

Despite the subdued demand overall, ore prices are expected to find support from more pre-holiday restocking activities among steelmakers, it added.

“Steelmakers usually increase spot purchases of iron ore to build up their in-plant stocks around one month before the Chinese New Year holiday, so the pre-holiday replenishment should begin from the second half of this month,” an iron ore analyst based in Shanghai explained. “This should lend strong support to iron ore prices,” he suggested.

In summary, this month import iron ore prices in China are likely to experience a dip before rising later, the report forecast, projecting that the Mysteel SEADEX 62% Australian Fines index will trade between $102/dmt and $108/dmt, a wider band than during December.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply