- HKC enforcement strengthens India’s competitiveness

- Political uncertainty weakens Chattogram market sentiment

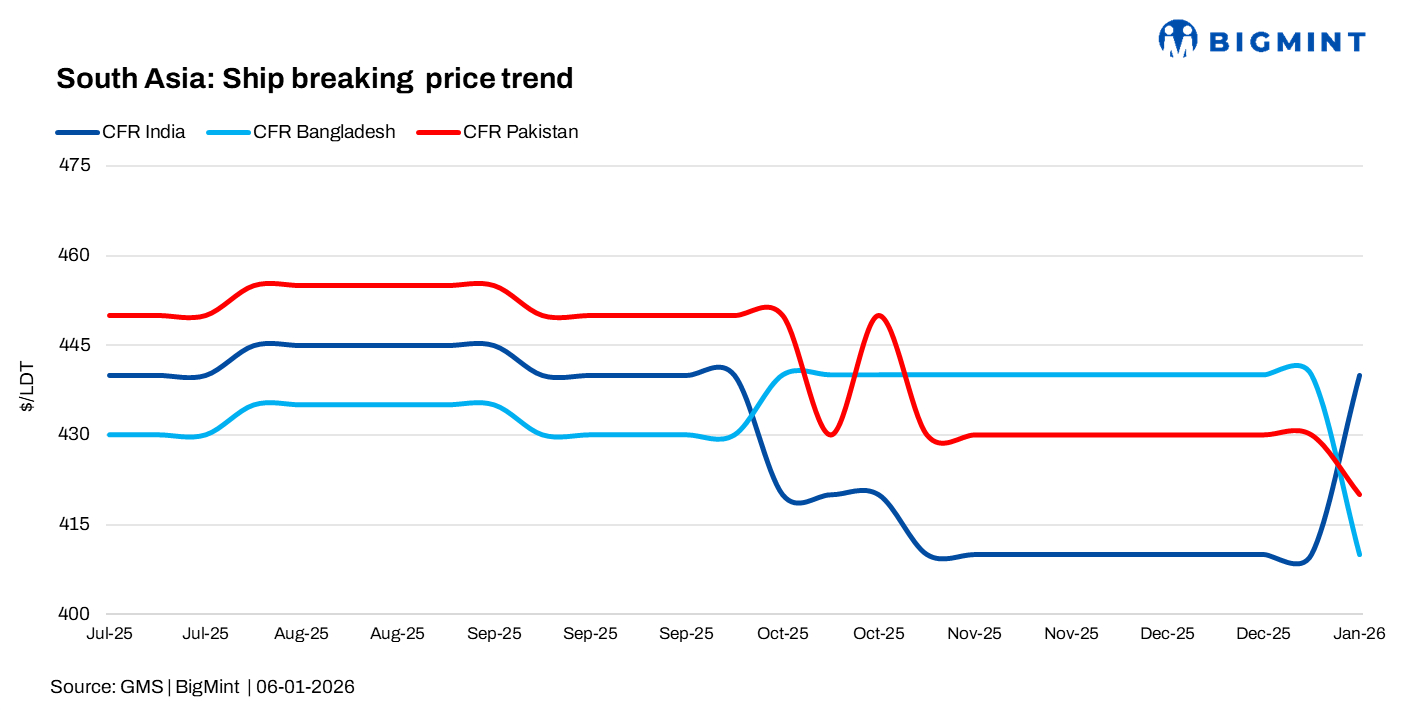

In the beginning of 2026, the South Asian ship-breaking markets are showing a mixed picture. The Alang market in India has been strengthening due to a rebound in domestic steel market sentiments, while Bangladesh and Pakistan struggle with political uncertainty, limited HKC capacity and weak demand, shifting regional tonnage flow toward India.

Alang reclaims spotlight as 2026 begins

The Indian ship recycling market rebounded strongly, with prices rising nearly $30/LDT and lifting Alang to the top of global rankings for the first time in over three months, marking a positive start to 2026. Demand improved despite a weaker rupee crossing INR 90/$, boosting recycler optimism after a difficult 2025. Although Alang anchorage appeared unusually quiet, several vessels are waiting offshore, suggesting activity will pick up soon.

India remains the best-positioned destination for incoming tonnage, with the Hong Kong Convention now fully in force. In contrast, Bangladesh faces limited HKC-compliant yard capacity and political uncertainty, keeping shipowners cautious and shifting market focus toward Alang.

Bangladesh market under pressure

Since the tonnage glut in November 2025, Bangladesh’s ship recycling market has weakened sharply, with prices falling around $50/LDT from Q4 highs. Recyclers in Chattogram have become largely uncompetitive, dampening demand and sentiment. Political uncertainty ahead of the February elections, coupled with recent violent incidents, has further weighed on market confidence.

Despite reporting the subcontinent’s only arrivals this week, fundamentals remain fragile. Volatile steel plate prices, a weaker taka at BDT 122.30/$, and limited buyer appetite suggest a challenging outlook, raising the likelihood of tonnage diverting to alternative destinations.

Gadani lacks momentum despite opportunities

With Bangladesh slowing, Pakistan has a potential opening to attract tonnage, but Gadani recyclers remain hesitant. Local price indications continue below $400/LDT, and activity through December and early January has been largely muted, following a brief strong phase last year when Gadani topped regional price charts.

Anchorage levels have once again fallen quiet, highlighting subdued demand. While yards are upgrading to meet HKC standards, limited compliant capacity remains a key constraint. Stable steel plate prices, a slightly weaker rupee at PKR 280.62/$, and easing inflation offer some support, but India is likely to absorb most near-term tonnage.

Leave a Reply