- Weak Asian demand drove a 7.8% y-o-y drop in exports

- Uneven supply caused mixed port and regional shipment trends

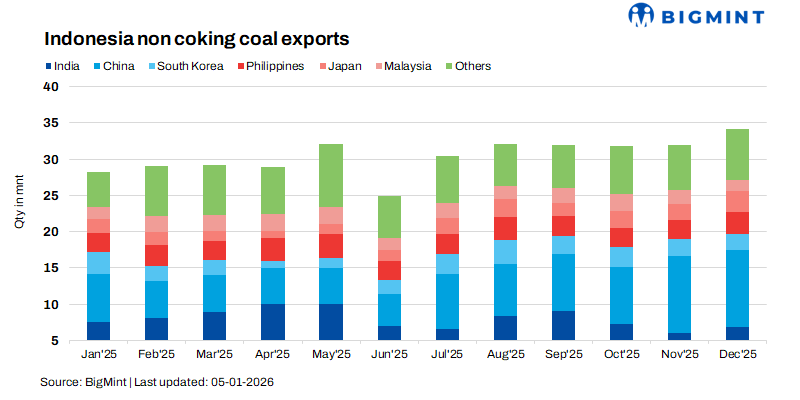

Indonesia’s total non-coking coal exports in CY’25 (Jan-Dec) stood at 364.6 mnt, down 7.8% year-on-year (y-o-y) from 395.5 mnt in CY’24, reflecting weaker regional demand conditions for most of the year. Non-coking coal exports increased on a month-on-month basis in December 2025, with shipments rising 6.7% to 34.1 million tonnes (mnt) from 31.9 mnt in November. The increase was largely driven by scheduled year-end loadings and improved port operations. However, on an annual basis, exports declined.

Asian demand softens amid high inventories

Most Asian importing countries reduced coal procurement in 2025 due to elevated stock levels, slower industrial activity, and cautious restocking strategies. India, Indonesia’s largest buyer, cut imports by 7% y-o-y to 95.4 mnt as power generators relied more heavily on domestic coal availability. Though prolonged monsoon last year in India significantly lifted hydropower and overall renewable energy generation, resulting in reduced coal-based power generation and softer electricity demand.

Malaysia was an exception, increasing imports by 1.7% y-o-y to 24.4 mnt, while the Philippines saw imports decline by 3.4% y-o-y to 34 mnt.

Northeast Asia shows limited buying interest

Demand from Northeast Asia remained subdued. Japan’s import declined 1.8% y-o-y to 22.7 mnt, reflecting lower thermal coal consumption. South Korea recorded only marginal growth of 0.8% y-o-y, with imports reaching 27.4 mnt. China posted the sharpest decline, with imports falling 21% y-o-y to 83.1 mnt from 105 mnt in CY’24, supported by strong domestic coal output and moderated power demand growth.

Regional supply trends remain mixed

Indonesia’s coal-producing regions showed varied performance in 2025, influenced by logistics constraints and demand for specific coal grades. East Kalimantan, the largest producing region, recorded a 13% y-o-y decline in shipments to 171.9 mnt, mainly due to vessel shortages and logistical challenges. Sumatra maintained stable volumes at 53.9 mnt. North Kalimantan exports declined 7.1% y-o-y to 15.1 mnt, while South Kalimantan shipments slipped 2.6% y-o-y to 123.7 mnt.

Port-wise shipments highlight uneven export flow

Port data mirrored the regional supply imbalance. Taboneo posted a 7.7% y-o-y increase in CY’25 shipments to 70.6 mnt, supported by steady contractual loadings. In contrast, Samarinda shipments fell 7.5% y-o-y to 50.6 mnt, while Muara Pantai volumes dropped sharply by 27% to 24.1 mnt. Balikpapan saw a 13% y-o-y decline to 27.2 mnt, whereas Bunati recorded a strong 27% y-o-y rise to 43.8 mnt.

Benchmark prices firm entering 2026

Indonesia’s Ministry of Energy and Mineral Resources (ESDM) revised thermal coal benchmark prices upward for the first half of Jan’26, indicating improving price sentiment. The 6,322 kcal/kg GAR benchmark increased 2.5% to $103.3/t, supported by firmer regional demand and controlled supply. The 5,300 kcal/kg GAR index rose 3.3% to $72.23/t, while lower-grade coal prices also strengthened, with the 4,100 kcal/kg GAR benchmark reaching a six-month high of $47.05/t. The 3,400 kcal/kg GAR index edged up slightly to $35.13/t, reflecting steady demand from cost-sensitive buyers.

Export duty policy adds uncertainty

Indonesia has yet to finalise its coal export duty framework for 2026. While the levy was initially proposed at 1-5% and expected to take effect from January, resistance from miners has delayed implementation. Revised proposals now suggest a tiered structure of 5-11% linked to global coal prices, though these remain under review. The lack of clarity has increased uncertainty around export competitiveness and production planning.

Outlook

Going forward, Indonesia’s non-coking coal exports are expected to remain stable in the near term, supported by firmer benchmark prices and selective demand recovery in Asia. However, high inventories in key markets, weak buying interest from China, and unresolved export duty policies are likely to cap any sharp rebound. Overall, the market is expected to move into 2026 with a balanced but cautious outlook.

Leave a Reply