- Tight supply conditions supported market sentiment

- Regional inventories signaled tightening physical markets

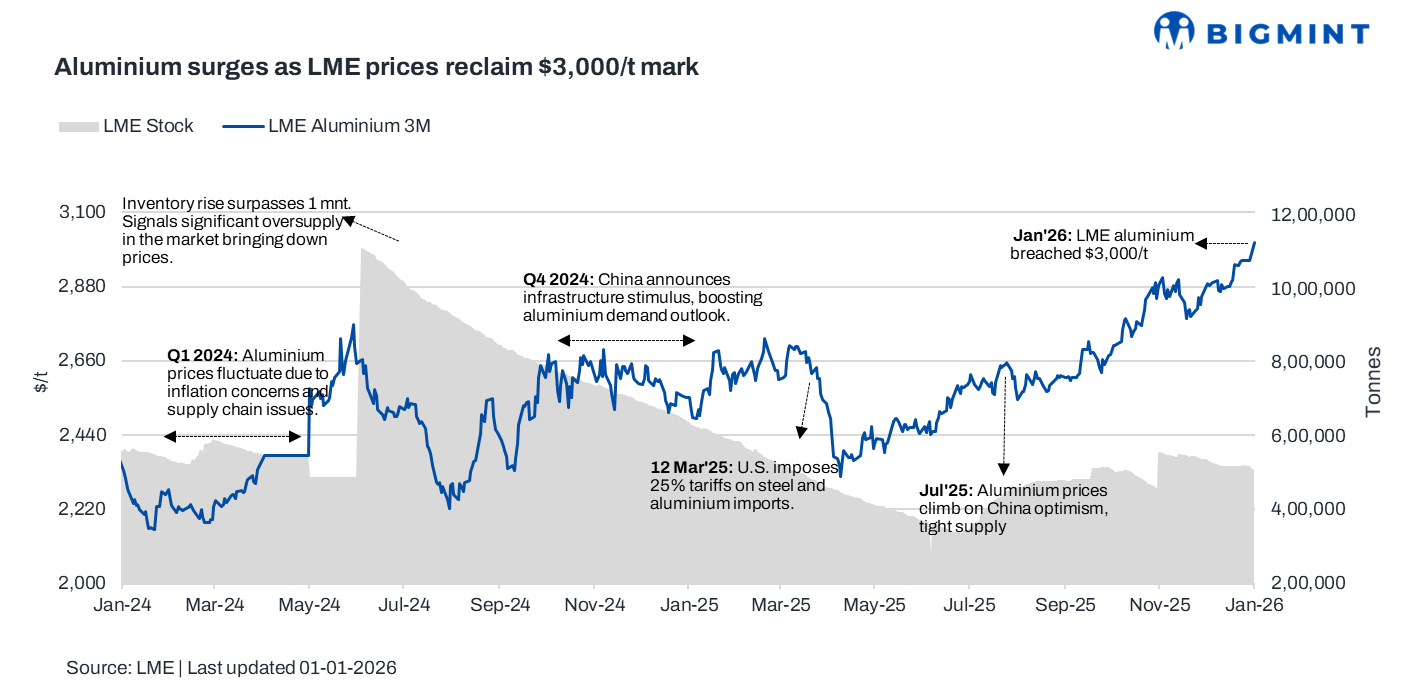

Benchmark aluminium prices on the London Metal Exchange (LME) edged higher during the week ended 01 January 2026, supported by tightening global supply expectations. LME aluminium prices rallied to touch $3,000/t, driven by tightening supply conditions, China’s capacity constraints, falling exports, and signs of regional inventory tightness, reinforcing expectations of a structurally firmer aluminium market.

Pricing, inventory trends

LME aluminium prices averaged $2,980/t in the week ended 01 January, up $30/t or 1% w-o-w. Prices opened the week at around $2,959/t and strengthened mid-week reaching $2,990/t and closed the week at $3,010/t.

Meanwhile, LME aluminium inventories witnessed a drop settling at 515,110 t w-o-w from 519,600 t in week 52.

Factors impacting prices

LME aluminium prices rose as market sentiment strengthened on a tightening supply outlook and expectations of resilient long-term demand. Prices were supported by China’s continued enforcement of its 45-million-tonne smelting capacity cap, which is limiting incremental supply just as domestic demand improves.

As a result, Chinese producers redirected more output to the local market, contributing to a 9.2% y-o-y decline in aluminium exports in November. Supply concerns were further reinforced by delays to overseas expansion projects by Chinese smelters, particularly in Indonesia, due to higher energy costs and regulatory risks.

Regional tightness was evident in falling inventories at major Japanese ports, which declined 5.2% m-o-m, offsetting a modest rise in SHFE stocks. Together with only marginal growth in global primary aluminium output, these factors tightened physical market conditions and pushed LME aluminium prices higher.

Outlook

LME aluminium prices are expected to remain firm in the near term, supported by constrained supply growth, China’s capacity limits, and declining export availability. While modest inventory rebuilds may cap upside, structurally tight regional markets and steady demand prospects should continue to underpin prices, keeping volatility skewed to the upside.

Leave a Reply