- Coal and coke prices mixed amid cautious demand, adequate inventories

- Freight markets weak, sponge iron supports South African coal

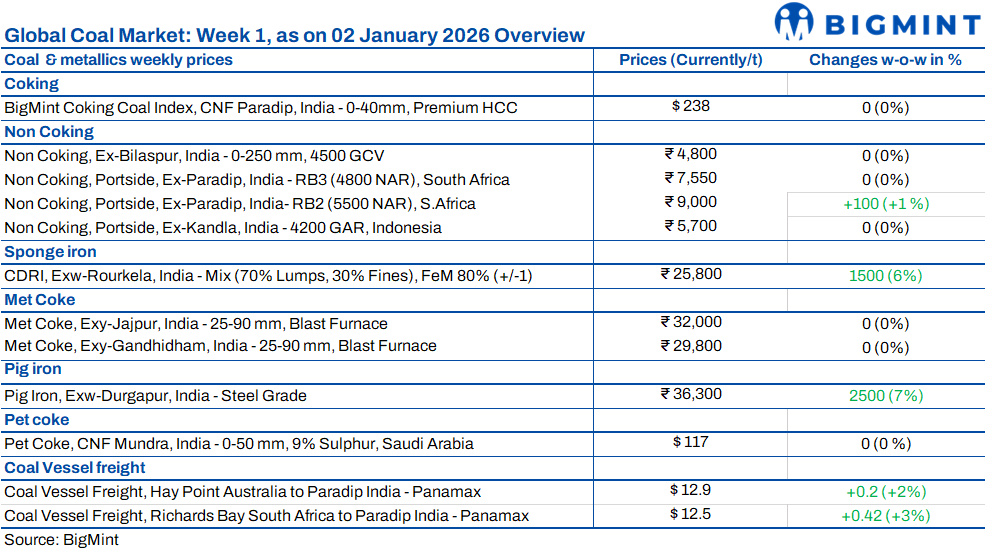

India’s coal and coke markets commenced CY’26 with mixed trends, shaped by subdued demand, adequate inventories, and cautious trade sentiment. While Indonesian coal remained stable and South African coal gained support from rising sponge iron prices, coking coal indices softened, metallurgical coke prices stayed steady, and freight markets weakened. These dynamics reflect a measured start to the year, with near-term activity expected to remain range-bound.

Indonesian non-coking coal remains stable despite HBA price hike

Indian portside prices for Indonesian thermal coal were largely stable week-on-week until 2 January 2026, supported by muted spot buying and sufficient portside inventories. High-grade 5,000 GAR remained unchanged, while lower CV grades experienced minor softening. Declining freight rates cushioned landed costs despite weaker global benchmarks. Portside coal inventories declined slightly by 3% w-o-w to 12.91 million tonnes, while power plant stocks remained comfortable.

Additionally, Indonesian benchmark prices were revised upward, reflecting steady export trends. Indonesia’s Ministry of Energy and Mineral Resources (ESDM) has revised its thermal coal benchmark prices (HBA) for the first half of January 2026, indicating a firm upward trend across all calorific value segments. The 6,322 kcal/kg GAR benchmark increased by 2.5%, the 5,300 kcal/kg GAR (HBA-I) index rose 3.3% and lower-grade coal benchmarks extended their upward momentum. HBA-II (4,100 kcal/kg GAR) surged 3.5% from the second half of December

South African thermal coal gains on sponge iron support

Portside South African thermal coal prices in India increased INR 100-300/t w-o-w by 2 January 2026, primarily driven by higher sponge iron prices and tightening inventories. RB2 (5,500 NAR) rose to INR 9,000–9,200/t ex-Paradip/Vizag/Gangavaram, whereas RB3 (4,800 NAR) remained stable at INR 7,500–7,550/t. Traders observed limited deal closures despite firm offers, citing sufficient domestic coal availability. Simultaneously, portside inventories fell 3% w-o-w due to faster evacuation and slower arrivals, supporting price stability.

Domestic coal prices range-bound amid CIL’s e-auction initiative

Domestic coal prices remained steady, with 5,000 GCV at INR 5,750/t and 4,500 GCV at INR 4,800/t w-o-w, underpinned by adequate regional supply and need-based procurement. Moderate downstream demand helped maintain market equilibrium. In a significant development, Coal India Limited (CIL) allowed foreign buyers to participate in e-auctions under the revised Modified CIL E-Auction Scheme 2022, effective 1 January 2026. Foreign participants can register using international tax identification numbers, enabling them to bid alongside domestic buyers, thereby enhancing India’s coal trade presence globally while ensuring compliance with trade regulations.

Coking coal index softens on limited trade activity

BigMint’s premium hard coking coal (PHCC) index eased to $236/t CNF Paradip on 2 January 2026, down $2/t from 26 December 2025, reflecting muted trading during the New Year holidays. Global activity remained limited, though a western India-based steel mill booked around 30,000t (+/-10,000t) of Australian PHCC at $238/t CFR India for mid-January loading. BigMint has revised its PHCC CFR India index to include multiple origins, aligning with India’s gradual diversification from Australian supplies.

Metallurgical coke prices stable amid cautious trading

The Indian metallurgical coke market remained largely unchanged w-o-w until 31 December 2025, reflecting balanced but cautious sentiment. BF-grade coke prices were steady at INR 32,000/t ex-Jajpur in the east and INR 29,800/t ex-works Gandhidham in the west, while foundry-grade coke remained at INR 35,200/t ex-Rajkot. The government’s provisional anti-dumping duty on low-ash met coke imports supported domestic producers. Concurrently, Australian PHCC remained stable at $218/t FOB, providing cost stability despite rising domestic availability.

Freight markets open weak amid thin activity

Dry bulk coal freight markets into India opened CY’26 on a weak note, weighed down by thin fixing activity, cautious chartering, and ample prompt tonnage. Panamax and Supramax rates remained under pressure across Australia-India, South Africa-India, and Indonesia-India routes, with minimal fresh fixtures. Falling bunker prices and softer FFA levels reinforced the bearish sentiment. Route-wise, Australia-India Panamax edged up to $12.9/dmt, South Africa-India to $12.5/dmt, while Indonesia-India Supramax softened to $12.8/dmt.

Leave a Reply