- Rebar prices rise INR 1,800-6,000/t m-o-m across regions

- Higher billet and sponge iron prices anchor rebar offers

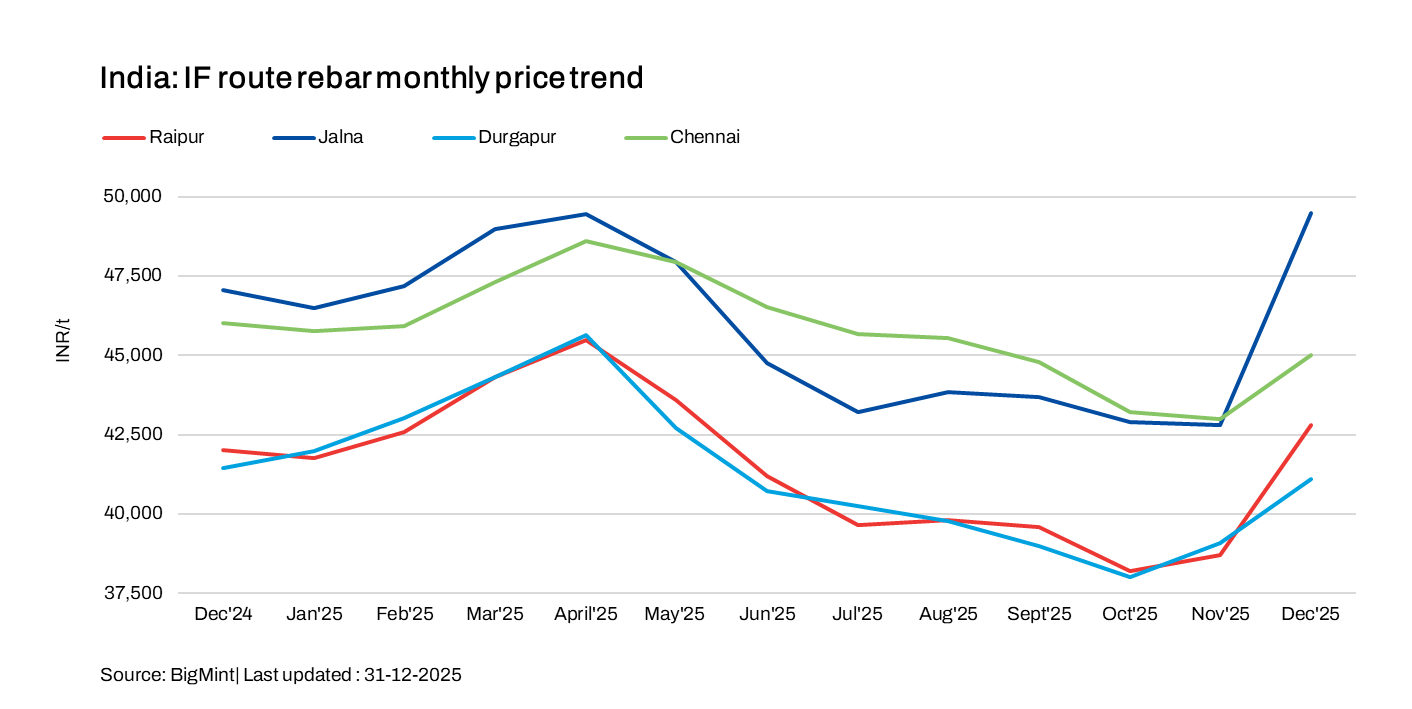

IF-route rebar prices witnessed a strong upward thrust in December 2025, rising by INR 1,800-6,000/t m-o-m across regions, according to BigMint’s assessment. Rebar prices climbed to a 7-8 month high after hitting a four-year low in October. The uptrend was mainly observed in the last week of the month, primarily driven by improved market sentiment and steady enquiries, which translated into higher order bookings.

Firm sponge iron and billet prices reinforced rebar offers, keeping sellers confident in maintaining prevailing rates. Strengthened activity was also supported by procurement for the project segment and improved demand from the retail sector, reflecting a sustained positive momentum across markets.

Mills in most regions are operating at near-full capacity to meet prevailing demand. Mills have reported advance bookings of around 15-20 days, reflecting sustained buying interest. Meanwhile, inventory levels at mills are comfortable and range between six-eight days, varying by region, indicating balanced supply conditions.

As per Joint Plant Committee (JPC) data, India’s rebar production through the IF and BF routes stood at 34.2 million tonnes (mnt) in April-November of FY’26, marking a significant 9% rise from around 31.3 mnt in the same period of FY’25.

Region-wise price movements

Factors impacting market

Raw material prices support uptrend: The continued upward movement in finished steel prices was strongly supported by firm raw material costs, particularly the sharp rise in steel billet prices, along with higher sponge iron values-both key inputs in IF-route production. The notable increase in billet prices played a major role in pushing overall costs higher. Steady buying interest and improved trade activity across several markets encouraged manufacturers to maintain or further raise prices, reinforcing bullish market sentiment.

Considering Raipur as the benchmark, billet prices rose by INR 3,950/t m-o-m to INR 40,450/t ex-works, while sponge iron (PDRI FeM 80% ±1) increased by INR 650/t m-o-m to INR 24,550/t ex-works. These firm raw material prices underpinned the upward movement in IF rebar offers.

Production & inventory levels

Mills across regions are operating at near-full capacity to meet prevailing demand conditions. Market activity remains positive, backed by healthy enquiry levels and smooth dispatches. Mills have reported advance bookings of around 15-20 days, reflecting sustained buying interest. Meanwhile, inventory levels at mills are comfortable and range between six-eight days, varying by region, indicating balanced supply conditions.

Improved demand: Market activity remains positive, backed by adequate enquiries, smooth dispatches, and a gradual reduction in inventories at secondary mills. Seasonal improvement in construction activity, strong momentum from project orders, and support from firm raw material prices are expected to keep rebar prices on a firm trajectory over the next three months. Mills continue to operate at full capacity to meet demand.

BF-route rebar sentiment

Trade-level BF rebar prices strengthened in December, rising by INR 800/t m-o-m to an average of INR 47,800/t exy-Mumbai, supported by improving domestic demand. Buying momentum accelerated in the second half of the month, particularly from the projects segment, prompting mills to announce multiple price hikes. During the last week of December, Tier-I mills raised list prices by up to INR 2,000/t.

In the first week of January 2026, trade-level BF rebar prices surged, climbing INR 2,900/t w-o-w to around INR 51,900/t exy-Mumbai, as per BigMint’s assessment on 2 January. Project segment prices were assessed at INR 51,000-52,000/t on a FOR Mumbai basis.

Outlook

Prices are expected to remain firm through January, supported by stable raw material costs, improved project execution, and healthy dispatch activity. Strong infrastructure-led demand is likely to keep prices near seasonal highs across key markets. Disciplined order booking by mills, with backlogs of 15-20 days, continues to provide pricing support. Additionally, controlled supply from primary producers is expected to limit downside risks.

Leave a Reply