- Safeguard duty on flat steel imports boosts market sentiment

- Domestic scrap demand stays strong on price hike expectations

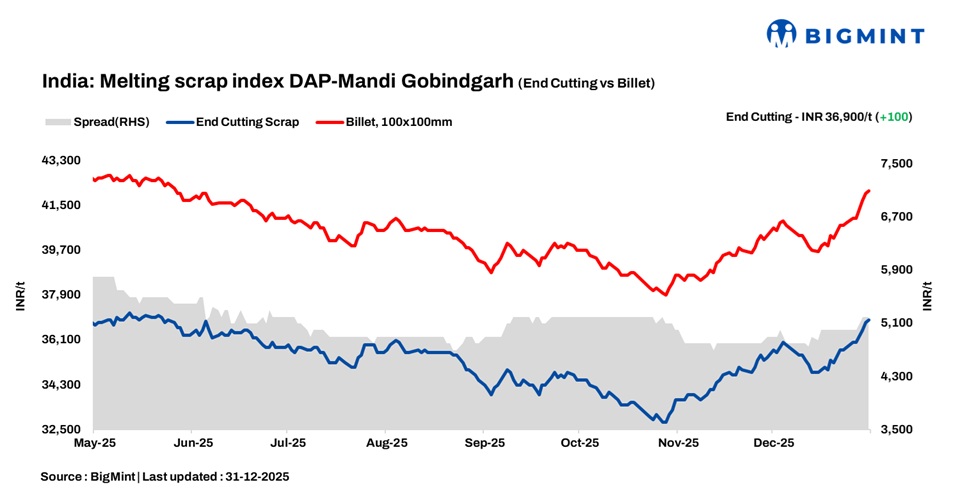

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, inched up by INR 100/tonne (t) d-o-d to INR 36,900/t DAP on 31 December 2025.

India’s secondary steel markets remained upbeat in today’s trading session, with a moderately strong improvement in demand taking place across the raw materials to finished steel segments. This was primarily fuelled by positive sentiment from the government’s new safeguard duty on key flat steel products, including HR coils/plates, CR coils, metallic-coated, and colour-coated steel.

In Mandi Gobindgarh, bookings for domestic ferrous scrap remained robust, with mills actively procuring amid expectations of an upcoming price hike. Imported scrap bookings remained on hold due to weakened price viability, as cheaper domestic material was readily available in the region.

The Mandi market received the following offers for imported scrap: US-origin HMS (80:20) was quoted at around $325-327/t CFR west coast India, while HMS 1 from the same origin was heard at $335-336/t CFR. Bahrain-origin HMS 1 material was assessed higher at $340/t CFR west coast India.

Alternative raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh edged up by INR 100/t d-o-d to INR 29,400/t DAP. Steel grade pig iron prices in Ludhiana remained flat d-o-d at INR 37,500/t DAP.

Steel market trend

In Mandi Gobindgarh, semi-finished steel prices rose INR 100/t d-o-d to INR 42,100/t DAP during the reporting and normalisation period. Across major steel hubs, prices gained INR 100-150/t, signalling a broadly positive trend.

Similarly, in the rebar (Fe500) segment, Mandi prices remained stable d-o-d at INR 46,800/t exw, supported by moderate demand.

Overview of Alang market

On 31 December 2025, Alang’s ship-breaking melting scrap (HMS 80:20) prices declined by INR 400/t d-o-d to INR 32,300/t ex-yard, driven by subdued semi-finished and finished steel activity in the previous day’s afternoon session and mills pushing back against higher scrap quotes.

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 5,000-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $325-326/t, approximately INR 31,500/t (inclusive of freight). HMS (80:20) in Mumbai remained stable d-o-d at INR 31,300/t DAP. Indicative prices of shredded from Europe stood at $350-$354/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 15,250/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

Leave a Reply