- G4 coal dominates buyer interest in both auctions

- Buyers resort to selective procurement strategy

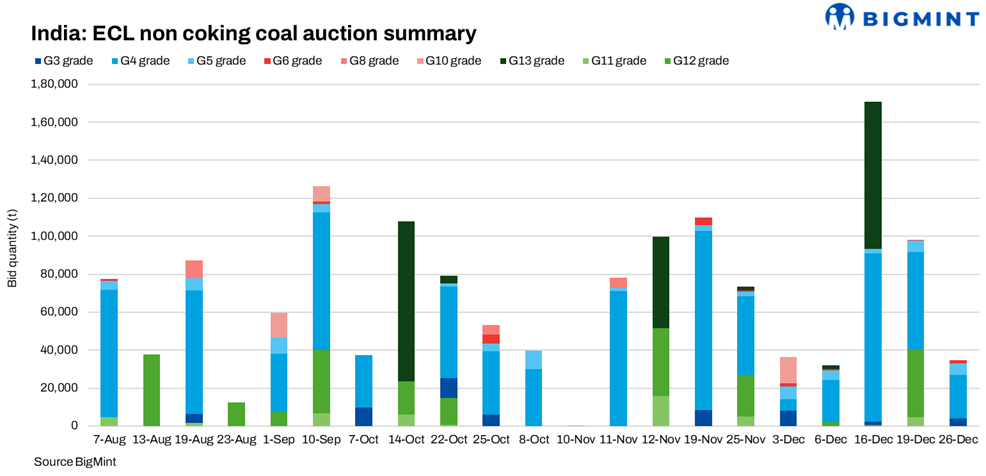

Coal India (CIL) subsidiary Eastern Coalfields Limited (ECL) concluded two non-coking coal auctions on 19 December and 26 December 2025. The auctions reflected buyer preference for mid-calorific value (CV) coal grades and saw underground (UG) coal fetching sustained premiums despite limited volumes sold.

In the two auctions ECL offered a combined 1.18 million tonnes (mnt) of coal, while the total bid quantity stood at 173,350 t, underscoring weak procurement behaviour. Buyers remained focused on G4 grade coal, with allocations concentrated among traders and industrial consumers, while the lower-CV grades saw restrained participation and price-sensitive clearing.

Grade-wise performance

G4 dominated allocations in both auctions, accounting for nearly two-thirds of total volumes. On 19 December, G4 alone accounted for 88,800 t, supported by aggressive bidding for select UG parcels, while G12 and G11 volumes cleared largely at utility-linked price levels. The 26 December auction saw smaller overall volumes, but firmer average G4 prices, reflecting tighter availability and continued demand for quality mid-CV material. G3 and G5 saw moderate interest, while G6 remained marginal across both auctions.

Mine-wise highlights

UG coal continued to command clear premiums over opencast (OC) material. On 19 December, UG mines such as Jhanjra, Pandaveswar, Central Kajora, and Kumardihi A recorded materially higher realisations compared to large OC mines like Sonepur Bazari and Khottadih. Jhanjra UG emerged as a key contributor within G4, reinforcing buyer preference for cleaner, consistent coal.

The 26 December auction further highlighted UG strength, with Kunustoria UG achieving the highest G4 realisation of INR 6,867/t, followed by JK Nagar and Belbaid UG, while OC supplies from Sonepur Bazari and Amkola were cleared at comparatively lower but stable levels.

Buyer behaviour

Buying remained concentrated among a limited set of traders and industrial consumers. On 19 December, Saroj Commodities, Maharaja Udyog, SS Enterprises, Khatu Shyam Steels, and Laxmi Narayan Enterprises were active primarily in the G4 segment, lifting mid-sized parcels with consistent pricing. Participation was fragmented, but bidding for UG-linked G4 parcels was visibly aggressive.

On 26 December, buyers such as Shakambhari Ispat and Power, Iconic Coal Company, Khemka Minerals, and Laxmi Narayan Enterprises continued to anchor demand. Although parcel sizes were smaller, bids for UG G4 and select G3 material remained firm, indicating targeted procurement rather than volume-driven buying.

Takeaway

The twin auctions reaffirmed a segmented domestic coal market. While overall volumes stayed limited, buyers continued to prioritise quality over quantity, particularly within G4 UG coal. Lower-CV grades cleared mainly on price discipline, while UG-origin mid-CV coal retained scarcity value. The widening price dispersion across grades and mines suggests that demand is not uniformly weak, but increasingly selective and application-driven.

Leave a Reply