- Imported coal demand stays weak despite selective price corrections

- Imported pet coke market remains quiet amid wide bid-offer disparities

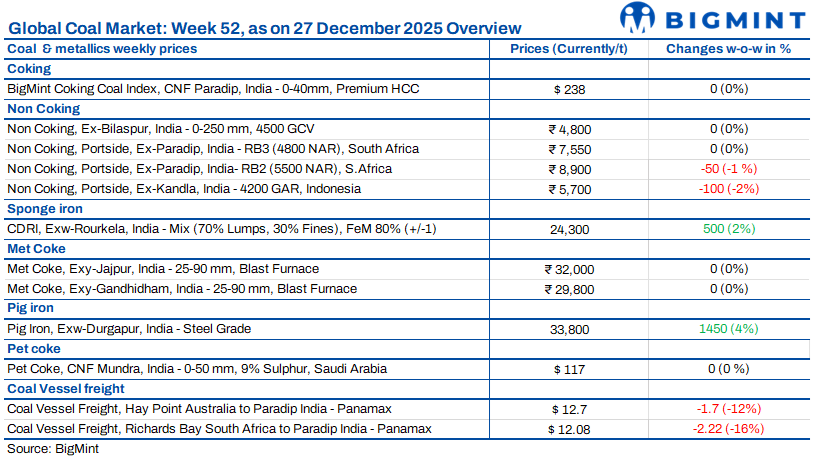

Indian coal market sentiment remained subdued during the week ending 27 December 2025, shaped by holiday-led inactivity and cautious buying behaviour. Imported coal offers softened selectively, but higher replacement costs and uneven availability limited trade interest. Domestic supply was comfortable, keeping procurement largely need-based. Portside stocks remained balanced overall, though distribution varied across locations. Market participants largely stayed on the sidelines, awaiting clearer downstream signals and post-holiday normalisation before committing to fresh volumes.

Portside Indonesian coal prices steady amid subdued spot buying

Indian portside Indonesian thermal coal prices remained largely stable in the week ended 26 December, as subdued spot buying limited price movement. According to BigMint’s assessment, 5,000 GAR was unchanged w-o-w at INR 7,200/t at Kandla and INR 7,100/t at Vizag. Prices of 4,200 GAR softened marginally by INR 100/t to INR 5,700/t at Kandla and INR 5,600/t at Vizag, while 3,400 GAR held steady at INR 4,500/t at Navlakhi. Power sector coal stocks eased to 54.67 mnt from 55.16 mnt, offering around 18 days of cover. In the seaborne market, Indonesian prices softened, with 4,200 GAR down $0.44/t and 3,400 GAR down $0.55/t. Overall sentiment remained cautious amid ample supply and weak demand.

Portside South African coal prices ease amid lull

Portside South African thermal coal prices eased in the week ended 26 December amid weak year-end buying. RB2 (5,500 NAR) ex-Paradip, Vizag and Gangavaram declined to INR 8,850-8,900/t, while RB3 (4,800 NAR) slipped to INR 7,500/t ex-Vizag and stayed INR 7,550/t at Paradip and Gangavaram. The correction followed a fall in freights to about $12/dmt from $14/dmt. International trade activity remained muted due to the Christmas and New Year holidays. Meanwhile, sponge iron prices strengthened, with CDRI ex-Rourkela rising INR 500/t w-o-w to INR 24,300/t and prices in other markets gaining INR 50-300/t. Portside thermal coal stocks rose 1.8% w-o-w to 13.31 mnt, though uneven port-wise distribution continued to influence local price movements.

Domestic coal prices remain flat on ample supply

According to BigMint’s assessment, 5,000 GCV coal stayed flat w-o-w at INR 5,750/t, while 4,500 GCV was stable at INR 4,800/t. Coal availability remained adequate across major consuming regions, limiting any urgency in procurement. Buying activity was largely need-based, even as downstream sentiment showed marginal improvement. The balance between steady supply and cautious demand kept price movements limited to a narrow range.

Coking coal index holds firm

BigMint’s premium hard coking coal (PHCC) index stayed unchanged w-o-w at $238/t CNF Paradip on 26 December, as market activity remained muted during the Christmas holiday period. Trading interest stayed limited, with no fresh deals heard. Market participants noted that global inactivity kept prices stable, although supply-side risks provided support, as heavy rains in Australia’s Moranbah region disrupted mining operations and logistics.

Met coke prices stay steady

India’s metallurgical coke market remained largely stable in the week ended 24 December, as cost pressures were balanced by muted demand. BF-grade met coke stayed unchanged at INR 32,000/t ex-Jajpur in eastern India and INR 29,800/t ex-Gandhidham in the west. Foundry-grade prices softened, falling INR 600/t w-o-w to INR 35,200/t ex-Rajkot due to weak offtake. Producers continued to face margin pressure as Australian premium hard coking coal prices rose to $218/t FOB, up $1/t w-o-w. In pig iron, prices firmed, with exw-Durgapur assessed at INR 33,100/t, supported by bids in SAIL Rourkela’s auction, which averaged INR 33,750/t. Overall sentiment stayed cautious.

Imported pet coke trade stalls for 4th straight week

India’s imported pet coke market remained inactive for a fourth consecutive week, with no confirmed spot trades heard. Offers stayed firm at $120-121/t CFR India, while bids remained capped at $114-115/t, leaving a persistent $5-7/t gap that prevented deal execution. Buying interest stayed weak as consumers continued to favour cheaper thermal coal alternatives from the US, South Africa and Mozambique, available at a $5-10/t cost advantage. Comfortable inventories further reduced procurement urgency, with end-users reporting no immediate requirement for fresh cargoes. Market participants maintained a wait-and-watch approach, expecting activity to revive only if prices corrected meaningfully or coal economics shifted.

Freights weaken due to holidays

Dry bulk coal freight rates to India stayed under pressure in the week ended 26 December as year-end holidays reduced activity and cargo volumes remained thin. Panamax freights from Australia to India fell $1.7/dmt w-o-w to $12.70/dmt, while South Africa-India rates dropped sharply by $2.22/dmt to $12.08/dmt. Indonesia-India Supramax freights declined $0.85/dmt to $12.91/dmt. Ample vessel availability and limited enquiries kept owners competitive. The Baltic Panamax index slipped 122 points to 1,267, while the Supramax index fell 114 points to 1,144. Lower bunker prices offered little support, as weak demand and high tonnage continued to weigh on the market.

Leave a Reply