- Pacific gains offset weakness in Atlantic region

- Soft freights, ample tonnage slow down fixing

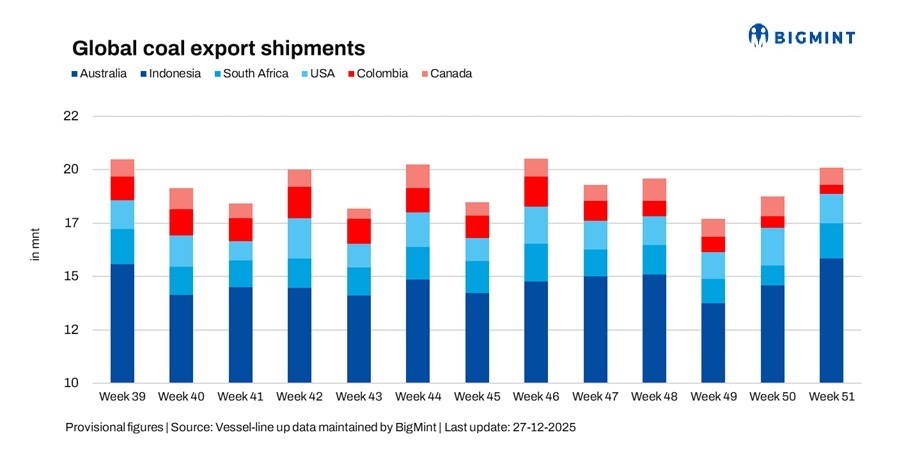

Global seaborne coal exports rose 7.3% w-o-w to 19.70 million tonnes (mnt) in the week ended 19 December (week 51) from 18.36 mnt in the previous week, according to BigMint’s vessel line-up data. The increase was mainly driven by stronger shipments from Australia, Indonesia, and South Africa, which more than offset declines from the US, Colombia, and Canada. Despite the overall rise in volumes, market conditions remained uneven across regions.

The w-o-w improvement reflected better cargo availability from key Pacific and Atlantic suppliers, along with the release of previously deferred stems, particularly from Australia and South Africa. Improved operational flows allowed exporters to lift shipments compared with the prior week, supporting the overall rebound in global volumes.

However, softer freight sentiment, weaker downstream demand, and cautious buying behaviour continued to limit aggressive fixing activity. Falling freights and rising vessel availability reduced charterers’ urgency to secure tonnage, slowing the pace of new fixtures despite higher nominal export volumes.

Country-wise trends

Australian exports extend gains on steady port operations

Australia’s coal exports rose 3.4% w-o-w to 8.11 mnt in week 51 from 7.85 mnt in the previous week, marking a second consecutive w-o-w increase. The improvement was supported by steady loadings across major ports along the eastern coast and smooth operational conditions, enabling exporters to capitalise on available cargoes following earlier volatility. Newcastle led shipments with 3.74 mnt, followed by Gladstone at 1.52 mnt and DBCT at 1.27 mnt.

Glencore emerged as the leading shipper at 1.39 mnt, followed by BHP at 0.74 mnt and Yancoal at 0.33 mnt. Despite the rise in volumes, export momentum remained measured, as Indian and northeast Asian buyers continued to procure selectively amid weak steel margins, elevated inventories, and softer freight markets. Japan and China were the major importers, taking around 2.0 mnt and 1.5 mnt, respectively.

The lack of urgency from buyers limited any sharper upside, indicating that the increase was largely supply-led rather than demand-driven. Separately, Adani Ports and Special Economic Zone (APSEZ) has completed the acquisition of Australia’s North Queensland Export Terminal (NQXT), strengthening its Asia-Pacific presence and long-term global cargo expansion strategy.

Indonesian coal exports rebound on release of delayed stems

Indonesia’s coal exports rebounded by 13.4% w-o-w to 7.50 mnt in week 51 from 6.61 mnt in week 50, recovering after the previous week’s pullback. The increase was supported by the release of delayed cargoes and marginally improved buying interest from India, even as broader Pacific demand remained subdued. Taboneo and Bunati were the major loading ports, handling 1.26 mnt and 1.22 mnt, respectively.

China and India emerged as the leading importers, taking 2.72 mnt and 1.61 mnt of Indonesian coal during the week. However, the rebound did not indicate a meaningful shift in market sentiment. Softer freight markets and cautious chartering behaviour continued to cap fixing activity, leaving Indonesian shipments vulnerable to demand fluctuations despite adequate cargo availability and stable port operations.

Looking ahead, Indonesia’s coal market is expected to remain oversupplied with soft pricing into early 2026, as China and India increasingly rely on domestic production. Producers are responding by focusing on cost efficiency and diversifying beyond thermal coal.

South African exports surge on recovery from prior disruptions

South Africa’s coal exports surged 83.0% w-o-w to 1.59 mnt in week 51 from 0.87 mnt in the previous week. All shipments originated from Richards Bay, with the recovery following a disruption-impacted week 50 and reflecting the resumption of loadings and improved cargo flows after earlier operational constraints.

India emerged as the leading importer, taking 0.37 mnt during the week. However, demand conditions remained fragile, with Indian buying interest staying selective amid weak downstream fundamentals. As a result, the rise in exports was driven largely by pent-up supply and logistical normalisation rather than a material improvement in end-user demand, leaving the sustainability of higher shipment levels uncertain.

Meanwhile, South Africa increased coal exports to Israel following Colombia’s ban on shipments, with its share of Israel’s seaborne coal market rising in 2025, offering some diversification support amid softer demand across traditional Atlantic markets.

US coal shipments decline on softer follow-through demand

US coal exports declined 20.8% w-o-w to 1.32 mnt in week 51 from 1.7 mnt in week 50, following a strong, seasonally driven performance in the prior week. The pullback reflected softer follow-through demand and reduced urgency from European and Indian buyers after earlier winter-related stocking.

Mobile led loadings with 0.39 mnt, followed by Norfolk at 0.38 mnt and Baltimore at 0.25 mnt. India emerged as the leading importer of US coal during the week, taking 0.30 mnt. While overall cargo flows remained steady, competitive pressure from alternative suppliers and weaker freight economics limited fresh fixing interest, preventing US shipments from sustaining the elevated levels seen in the previous week.

Looking ahead, US thermal coal markets are ending 2025 on a firmer footing, with producers cautiously optimistic for 2026 as domestic demand and prices remain supportive. Softer seaborne pricing is prompting some producers to prioritise domestic sales, pointing to a stable start to 2026.

Colombian exports weaken further on persistent Atlantic softness

Colombia’s coal exports declined 14.0% w-o-w to 0.40 mnt in week 51 from 0.46 mnt in week 50, extending the downward trend. The fall was driven by continued weakness in European demand, cautious inventory management by buyers, and limited flexibility to redirect cargoes to alternative markets.

Puerto Nuevo led loadings with 0.20 mnt, followed by Puerto Bolivar at 0.16 mnt, while only minor volumes were shipped from Santa Marta at 0.04 mnt. The Netherlands and Turkiye were the leading importers, taking around 0.17 mnt and 0.16 mnt, respectively. Prodeco Group and Cerrejon Mines emerged as the main shippers, exporting 0.17 mnt and 0.16 mnt, respectively.

The sustained softness underscores Colombia’s exposure to Atlantic basin demand conditions, with shipment volumes remaining constrained amid limited near-term upside catalysts. Export sentiment has remained weak in 2025 following Colombia’s ban on coal sales to Israel, a previously key buyer, further increasing reliance on subdued Atlantic demand and limiting recovery prospects.

Canadian shipments slip amid cautious Asian buying

Canada’s coal exports declined 13.5% w-o-w to 0.8 mnt in week 51 from 0.91 mnt in the previous week. The pullback was driven by softer buying interest from northeast Asia and continued caution among importers amid ample global supply and volatile coal prices.

Vancouver led loadings with 0.35 mnt, followed by Roberts Bank at 0.27 mnt and Prince Rupert at 0.17 mnt. Elk Valley Resources emerged as the main shipper, exporting 0.35 mnt during the week.

South Korea was the leading importer of Canadian coal, taking 0.41 mnt. Despite stable port operations, Canadian exporters faced muted demand signals, keeping weekly volumes below recent averages and reinforcing the broader trend of selective procurement across Asian markets.

Coal freights soften across key routes

Global dry bulk coal freight markets softened during the week, with rates across key Pacific and Atlantic routes coming under pressure amid falling cargo volumes, abundant vessel availability, and cautious buying sentiment. The overall freight environment weakened as demand for tonnage slowed across both basins.

Rising vessel availability shifted bargaining power back towards charterers, slowing fixing activity and encouraging a wait-and-watch approach despite lower bunker costs. Charterers showed little urgency to secure tonnage, reflecting weak downstream visibility and muted cargo requirements.

The softer freight backdrop reduced shipment momentum from Indonesia and South Africa and limited the upside impact of stronger Australian exports. Overall, subdued freight sentiment reinforced cautious trade behaviour, preventing higher export volumes from translating into more aggressive fixing activity.

Outlook

Global coal exports are expected to remain mixed in the near term, with Australia likely to sustain relatively higher shipments if operational stability continues. Indonesian and South African volumes may fluctuate depending on demand visibility and prevailing freight dynamics, while Atlantic suppliers are expected to stay under pressure amid subdued European buying interest.

Overall, trade flows will continue to be influenced by freight sentiment, vessel availability, and short-term shifts in regional demand. With downstream consumption remaining soft and buyers cautious, shipment volatility is likely to persist, keeping exports sensitive to both logistical factors and market confidence through the remainder of December.

Leave a Reply